A. Facts of the Case

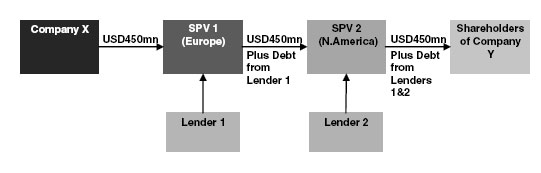

1. Company X (“X”), an Indian Company acquired an overseas

Company Y (“Y”) in Canada. The acquisition was to be funded by

contribution by Company X by way of an equity contribution of

USD 450 mn to a Special Purpose Vehicle – Netherlands

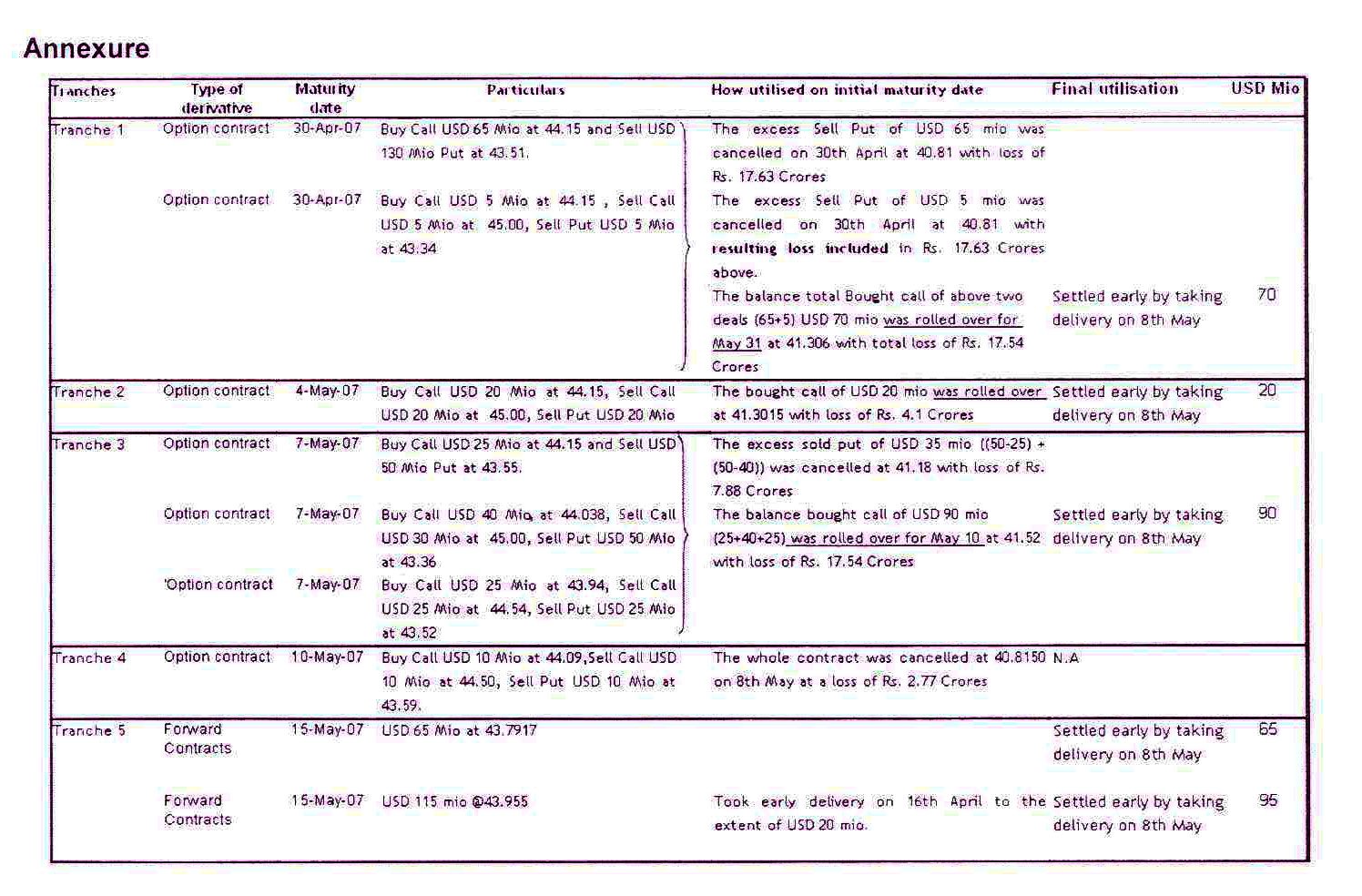

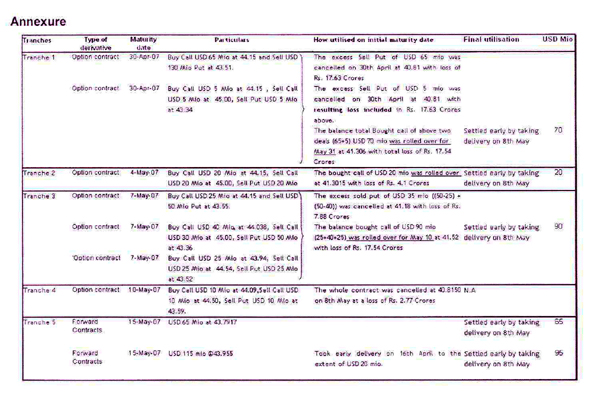

incorporated company (“SPV 1”) and the balance money was by

loans drawn by this SPV and others specifically created for this

purpose. The payment structure was as follows:

2. SPV 1 issued equity shares denominated in Euro to X. SPV 2

issued equity denominated in USD to SPV 1.

3. X had put in the bid for company Y during last week of

January ’07 and Y communicated to X on 20th February, ’07 that

they have been chosen as the preferred bidder. The transaction

had to be paid for and consummated by 15th May, ’07. To protect

against currency fluctuations, X entered into some forward contracts

and option contracts during last week of March ’07 and early April

’07 for USD 380 mn out of the total USD 450 mn exposure. Since

the exact payment dates were not known at that stage but the

expectation was that the deal would be closed not later than 31st

May and ideally around 15th May. Hence, X entered into derivatives

maturing around the expected payment date ranging from end

April to May 15th.

4. Significant portion of the derivative contracts was in the form

of Zero Cost Collar options, i.e., these derivatives provide the

holder a right to buy Dollars. However, instead of paying premium

the holder writes a compensating sell option. In the present case,

X has entered into leveraged options, i.e., where the pay off on

the written sell option is higher than the bought call option. X has

also entered into other variants of options.

5. The details of the derivative instruments and the activity therein

are as set out in the Annexure.

6. The actual payments were made as follows:

16-Apr-07 USD 70 mn USD 50 mn purchased from market

USD 20 mn from early delivery from

Tranche 5

8-May-07 USD 380 mn USD 340 mn was used by taking

delivery

against the derivative

contracts on 8th May

as set out in

table given in the Annexure.

USD 40 mn was purchased from

market

7. X has accounted for the losses incurred on various dates on

cancellation of the leveraged portion of the options and roll-forward

of the option contracts amounting to approximately Rs. 67 crore

as expense in the profit and loss account of the relevant period.

8. The net impact of settlement of the forward contracts on May

8, 2007 was not material.

B. Query

9. The querist has sought the opinion of the Expert Advisory

Committee on the following issues arising from the above:

(i) Whether the losses incurred (refer paragraph 7 above)

on the derivatives contracted for hedging the cash

outflow for equity investments can be considered as a

direct cost of acquisition and accordingly, added to the

cost of investments or would the losses have to be

taken to the profit and loss account.

(ii) Whether the combination of call and put options can be

considered as a forward exchange or another financial

instrument that is in substance a forward exchange

contract as in paragraph 36 of Accounting Standard

(AS) 11, ‘The Effects of Changes in Foreign Exchange

Rates’, and thus, be accounted for as forward contracts.

In the absence of any specific guidance for accounting

for option contracts what would be the primary source

of technical guidance for its accounting/disclosures

including the option contracts entered for hedging the

forecast transaction.

(iii) If it is agreed that these transactions are not covered by

existing Indian Accounting Standards, then whether

reference can be made to International Accounting

Standard (IAS) 39, ‘Financial Instruments: Recognition

and Measurement’, only for these transactions, i.e., not

adopt IAS 39 in its entirety, including potential for

claiming hedge accounting under IAS 39.

C. Points considered by the Committee

10. The Committee notes that the company in question had

entered into certain options and forward contracts to cover the

foreign currency risk to purchase an investment in future. In other

words, the aforesaid derivative contracts were entered into in

expectation of purchase of an investment in future.

11. The Committee notes that paragraph 36 of AS 11 provides as

below:

“36. An enterprise may enter into a forward exchange

contract or another financial instrument that is in

substance a forward exchange contract, which is not

intended for trading or speculation purposes, to establish

the amount of the reporting currency required or available

at the settlement date of a transaction. The premium or

discount arising at the inception of such a forward

exchange contract should be amortised as expense or

income over the life of the contract. Exchange differences

on such a contract should be recognised in the statement

of profit and loss in the reporting period in which the

exchange rates change. Any profit or loss arising on

cancellation or renewal of such a forward exchange

contract should be recognised as income or as expense

for the period.”

12. The Committee also notes that the above paragraph of AS 11

does not apply to forward exchange contracts to cover a future

transaction. In this context, the Committee notes that the Institute

of Chartered Accountants of India had issued, in January 2006, an

Announcement titled as ‘Accounting for exchange differences

arising on a forward exchange contract entered into to hedge the

foreign currency risk of a firm commitment2 or a highly probable

forecast transaction3’. The said Announcement is reproduced below:

“1. The Institute of Chartered Accountants of India (ICAI)

issued an Announcement, on ‘Applicability of Accounting

Standard (AS) 11 (revised 2003), The Effects of Changes in

Foreign Exchange Rates, in respect of exchange differences

arising on a forward exchange contract entered into to hedge

the foreign currency risk of a firm commitment or a highly

probable forecast transaction (see ‘The Chartered Accountant’,

July 2004 (pp. 110)). As per the Announcement, AS 11 (revised

2003) is not applicable to the exchange differences arising on

forward exchange contracts entered into to hedge the foreign

currency risks of a firm commitment or a highly probable

forecast transaction. It is stated in the Announcement that the

hedge accounting, in its entirety, including hedge of a firm

commitment or a highly probable forecast transaction, is

proposed to be dealt with in the Accounting Standard on

‘Financial Instruments: Recognition and Measurement’, which

is under formulation.

2. It may be noted that as per the above Announcement,

AS 11 (revised 2003) is not applicable to the exchange

differences arising on the forward exchange contracts entered

into to hedge the foreign currency risks of a firm commitment

or a highly probable forecast transaction. Accordingly, the

premium or discount in respect of such contracts continues to

be governed by AS 11 (revised 2003), The Effects of Changes

in Foreign Exchange Rates.

3. It has been noted that in the absence of any authoritative

pronouncement of the Institute on the subject, different

enterprises are accounting for exchange differences arising

on such contracts in different ways which is affecting the

comparability of financial statements. Keeping this in view,

the matter has been reconsidered and the Institute is of the

view that pending the issuance of the proposed Accounting

Standard on ‘Financial Instruments: Recognition and

Measurement’, which is under formulation, exchange

differences arising on the forward exchange contracts entered

into to hedge the foreign currency risks of a firm commitment

or a highly probable forecast transaction should be recognised

in the statement of profit and loss in the reporting period in

which the exchange rate changes. Any profit or loss arising

on renewal or cancellation of such contracts should be

recognised as income or expense for the period.”

13. The Committee notes that the above Announcement had been

deferred by subsequent Announcements made by the ICAI in

February 2006, June 2006 and July 2007.

14. With regard to whether the losses on derivatives should have

been added to the cost of investments, the Committee also notes

paragraph 28 of Accounting Standard (AS) 13, ‘Accounting for

Investments’, which requires as follows:

“28. The cost of an investment should include acquisition

charges such as brokerage, fees and duties.”

15. The Committee is of the view that the requirement of the

above paragraph of AS 13 covers charges on acquisition and,

accordingly, it does not include losses on derivative contracts as a

part of cost of investments.

16. The Committee is of the view that the nature of options

contracts or the combination thereof as per the facts of the case is

different from the forward contacts or their combination and

accordingly, the options contracts or their combination cannot be

considered as a forward exchange contract or another financial

instrument that is in substance a forward exchange contract for

the purposes of paragraph 36 of AS 11 and the Announcements

mentioned in paragraphs 12 and 13 above. The Committee is,

therefore, of the view that insofar as option contracts are concerned,

since there was no pronouncement of the ICAI, the company

could have adopted any rational treatment. Thus, recognising losses

on the options contracts was in order, keeping in view the principle

of prudence. Insofar as forward contracts were concerned, although

the Announcement reproduced in paragraph 12 above had been

deferred, the said Announcement formed the only authoritative

source of accounting for a forward transaction of a highly probable

forecast transaction. Thus, in case the concerned transaction met

the definition of the highly probable forecast transaction, recognition

of the loss thereon in the profit and loss account was in order.

17. It may be noted that the Institute of Chartered Accountants of

India has issued Accounting Standard (AS) 30, ‘Financial

Instruments: Recognition and Measurement’, corresponding to IAS

39. AS 30 becomes recommendatory in respect of accounting

periods beginning 1st April, 2009 and mandatory from 1st April,

2011. In view of the fact that options contracts are not forward

exchange contracts or another financial instrument that is in

substance a forward exchange contract as envisaged in paragraph

36 of AS 11, the company can follow AS 30 with regard to hedge

accounting provisions in case the combination(s) of options taken

by the company constitute(s) a hedging instrument(s), after having

satisfied all the requirements related to hedge accounting, e.g.,

those related to hedge effectiveness, documentation, etc.

D. Opinion

18. On the basis of the above, the opinion of the Committee on

the issues raised by the querist in paragraph 9 are as below:

(i) Losses incurred on the derivative contracts for hedging

the cash outflow for equity investments cannot be

considered as a direct cost of acquisition thereof and

accordingly, should not have been added to the cost of

investments. The treatment followed by the company to

recognise these losses in the profit and loss account

was in order.

(ii) Combination of call and put options cannot be considered

as a forward exchange or another financial instrument

that is in substance a forward exchange contract as

envisaged in paragraph 36 of AS 11. For authoritative

source of technical guidance for options contracts please

see (iii) below.

(iii) In view of the fact that options contracts are not forward

exchange contracts or another financial instrument that

is in substance a forward exchange contract as envisaged

in paragraph 36 of AS 11, the company can follow AS

30, corresponding to IAS 39, with regard to hedge

accounting provisions in case the combination(s) of

options taken by the company constitute(s) a hedging

instrument(s) after having satisfied all the requirements

related to hedge accounting, e.g., those related to hedge

effectiveness, documentation, etc.

1Opinion finalised by the Committee on 13.11.2007.

2A firm commitment is a binding agreement for the exchange of a specified

quantity of resources at a specified price on a specified future date or dates.

3A forecast transaction is an uncommitted but anticipated future transaction.

|