|

Query No. 14

Subject:

Accounting for deferred taxes.1

A. Facts of the Case

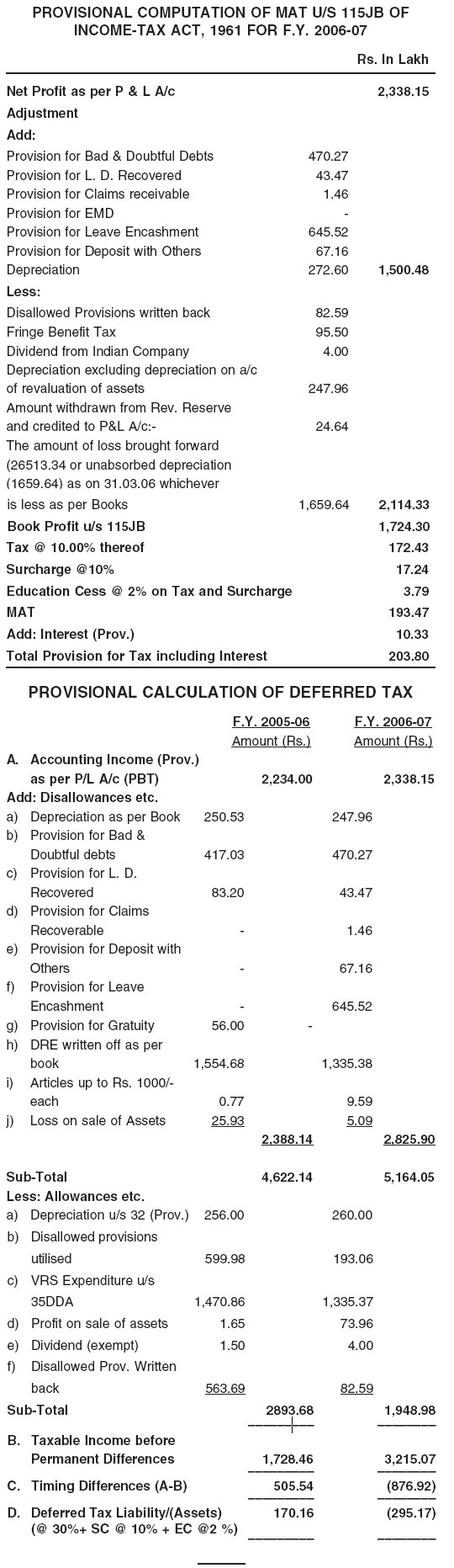

1. A Government of India enterprise under the Ministry of Steel

had been incurring losses from the financial year 1998-99 to

2003-04. As a result, the company is having unabsorbed

depreciation and accumulated losses. However, the company is paying Minimum Alternative Tax (hereafter referred to as ‘MAT’)

under section 115JB of the Income-tax Act, 1961.

2. The querist has referred to paragraph 17 of Accounting

Standard (AS) 22, ‘Accounting for Taxes on Income’, issued by

the Institute of Chartered Accountants of India, which states that

where an enterprise has unabsorbed depreciation or carry forward

of losses under tax laws, deferred tax assets should be recognised

only to the extent that there is virtual certainty supported by

convincing evidence that sufficient future taxable income will be

available against which such deferred tax assets can be realised.

The querist has informed that though the company had unabsorbed

depreciation and losses from financial year 1998-99 to 2003-04,

as per the above provisions of AS 22, it did not recognise deferred

tax assets due to lack of virtual certainty that sufficient future

taxable income will be available for realisation of the deferred tax

assets. For the year 2004-05 also, it did not recognise deferred

tax assets since the ‘virtual certainty’ condition was not met. The

querist has further informed that upto the financial year 2004-05,

as per financial data, only deferred tax asset was arising and

hence, the question of providing for deferred tax liability did not

arise.

3. During the financial year 2005-06, for the first time, the

company recognised deferred tax liability for Rs.170 lakh based

on provisional accounts. Again, during the financial year 2006-07,

deferred tax assets arose, which were not recognised for the

reasons stated in paragraph 2 above. At the same time, the

company did not reverse the opening deferred tax liability for Rs.170

lakh (created in the year 2005-06) during the financial year 2006-

07 and maintained the same figure in the balance sheet as at 31st

March, 2007.

4. The querist has informed that there were some items which

were getting reversed in the financial year 2006-07, like, provision

for bad debts, provision for liquidated damages, provision for

gratuity, expenditure on voluntary retirement scheme, etc.

5. The querist has supplied provisional computation of MAT under

section 115JB of the Income-tax Act, 1961 for the financial year

2005-06 and provisional calculation of deferred tax which is

contained in the Annexure, for the reference and perusal of the

Committee.

B. Query

6. Keeping the above in view, the querist has sought the opinion

of the Expert Advisory Committee on the following issues:

(i) Whether the company should reverse the deferred tax

liability created previously and make it nil during the

current year or the company should maintain the same

figure as deferred tax liability unless and until further

deferred tax liability is created or reduced as long as

the deferred tax asset is not recognised by the company.

(ii) Whether book profit as per the provisions of MAT will

be considered as taxable income for the purpose of

calculation of timing difference as per AS 22, when the

company is paying MAT or taxable income shall be

computed as per regular provisions of the Income-tax

Act to find out timing difference (i.e., difference between

accounting income and taxable income before permanent

difference).

C. Points considered by the Committee

7. The Committee notes that AS 22 deals with accounting for

both current tax and deferred tax. The principle underpinning

accounting for deferred taxes is that tax consequences of a

transaction should be recognised in financial statements during

the same period in which the underlying transaction is recognised

in the financial statements. Thus, accounting for deferred taxes

ensures proper matching of tax expense (saving) and the related

income (expense) recognised for accounting purposes.

8. From the information supplied by the querist in the Annexure,

the Committee notes that the basics of deferred tax accounting

have not been properly followed. The querist has started from

accounting income and made some adjustments to derive what

has been described as ‘taxable income before permanent

differences’. The difference between the two, which is naturally equal to the net effect of the adjustments made, has been described

as ‘timing differences’, which is multiplied by the tax rate and the

resulting figure has been stated as deferred tax liability or deferred

tax asset, as the case may be. Apart from deviation from the

principles of AS 22, this approach can lead to misleading results.

For example, some items, like, creation of provision for bad and

doubtful debts may result in deferred tax asset while excess of

depreciation for income-tax purposes over book depreciation

originating during the period may result in deferred tax liability.

Clubbing all differences into a one-line figure and describing the

same as ‘timing differences’ will result in set-off of deferred tax

assets against deferred tax liabilities even before prudence test is

applied which will distort the real picture. This may result in

understatement of deferred tax liabilities and overstatement of

profit, if prudence test fails on assessment of deferred tax assets

separately instead of mixing up with deferred tax liabilities. There

are other errors of principle also. For example, dividend income

exempted from tax has been deducted from accounting income

while deriving the so called ‘taxable income before permanent

differences’. It is a permanent difference. But, the one-line figure

described as ‘timing differences’ includes effect of dividend

exempted from tax. In other words, a permanent difference is

included in, and wrongly described as, timing difference. Thus,

though the querist has listed some sources of differences between

accounting income and taxable income, these have not been

properly segregated into permanent differences and timing

differences. Further, failure to segregate the timing differences

into originating and reversing differences may lead to incorrect

results. For example, a reversing timing difference in respect of a

deferred tax liability might be wrongly understood as an originating

timing difference in respect of a deferred tax asset. Also, there is

no such concept of ‘taxable income before permanent difference’

as mentioned by the querist. There is only accounting income

adjusted for permanent differences. There are also differences in

the amounts of some items between the provisional calculation

sheet of deferred taxes and the financial statements. While the

Committee notes the above points, it has not gone into the

correctness of computation of MAT and deferred tax liability, since

the query relates to principles only.

9. The requirements of AS 22, so far as measurement of deferred

taxes is concerned, are briefly summarised below:

(i) Normally, differences arise between accounting income

and taxable income. Such differences are classified as

timing differences and permanent differences. Timing

differences originate in one period and are capable of

reversal in one or more subsequent periods. Timing

differences arise because the period in which some

items of income and expenses are included in taxable

income does not coincide with the period in which these

are included or considered in arriving at accounting

income. Unabsorbed depreciation and losses are also

considered as timing differences. Permanent differences

are those that arise in a period but do not reverse

subsequently.

(ii) Permanent differences affect only current tax. They do

not affect deferred taxes.

(iii) Timing differences that are originating in a period may

result in creation of either deferred tax assets or deferred

tax liabilities, with corresponding credit/debit to the profit

and loss account. The deferred tax assets and liabilities

should be measured using the tax rates and tax laws

that have been enacted or substantively enacted by the

balance sheet date.

(iv) Timing differences that are reversing during the period

will result in liquidation (i.e., clearance) of the whole or

part of deferred tax assets/ deferred tax liabilities, already

created at the time of origination of timing differences,

with corresponding debit/credit to the profit and loss

account. For example, if depreciation for accounting

purposes for the period is less than depreciation for

income-tax purposes, a deferred tax liability arises. This

is because in future, depreciation for income-tax

purposes will be less than depreciation for accounting

purposes. Thus, while tax based on taxable income for

the current period is less than tax based on accounting income due to difference in depreciation, for future

period, tax based on taxable income will be more than

tax based on accounting income. Hence, a deferred tax

liability is provided for in the current period and cleared

in future when the depreciation difference reverses. This

matches tax expense with accounting income both for

the current period and the future period.

(v) While deferred tax liabilities should be recognised as

such, deferred tax assets should be considered

separately from deferred tax liabilities and recognised

only if the ‘prudence test’ is met. Accordingly, deferred

tax assets should be recognised and carried forward

only if there is a reasonable certainty that sufficient

taxable income will be available against which such

deferred tax assets can be realised. However, in case

an enterprise has unabsorbed depreciation or carry

forward losses, deferred tax assets should be recognised

only to the extent that there is virtual certainty supported

by convincing evidence that sufficient future taxable

income will be available against which such deferred

tax assets can be realised. The concepts of ‘reasonable

certainty’ and ‘virtual certainty’ have been explained in

relevant portions of AS 22. Deferred tax liabilities such

as those in (iv) above should be recognised even if the

deferred tax assets are not recognised.

(vi) As a corollary to point (v) above, originating timing

differences resulting in deferred tax assets and those

resulting in deferred tax liabilities should be separately

considered. They should not be mingled to see their

overall net effect. Further, to the extent a deferred tax

asset is not recognised in respect of an originating

difference due to failure to meet the prudence test, both

the origination and reversal of that difference will not

have deferred tax effects.

(vii) At each balance sheet date, an assessment should be

made of both unrecognised and recognised deferred

tax assets. To the extent prudence test is met, the former should be recognised and to the extent it is not

met, the carrying amount of the latter should be written

down. The corresponding adjustment should be

recognised in the profit and loss account. Reversal of a

previous write-down of deferred tax assets is also

permitted to the extent prudence test is subsequently

met.

10. The Committee notes that as per an announcement made by

the Council of the Institute of Chartered Accountants of India, tax

effect of any item should be recognised and presented in a manner

consistent with the manner in which that item itself is recognised

and presented. Thus, for example, if an item of income/expense is

directly adjusted in reserves, it should be net of tax effect. In other

words, the tax effect is also recognised in the reserves.

11. Thus, the basic steps involved in deferred tax accounting are

as follows:

(i) Identify the sources of differences between accounting

income and taxable income and their amounts.

(ii) Classify the differences between permanent differences

and timing differences.

(iii) Make further analysis of each item of timing difference

into originating differences and reversing differences.

(iv) Recognise deferred tax liabilities in full in respect of

originating timing differences during the period using

tax rates and tax laws that have been enacted or

substantively enacted by the balance sheet date.

(v) Liquidate deferred tax liabilities to the extent of reversal

of timing differences during the period in respect of

which they were created.

(vi) Recognise deferred tax assets in respect of originating

timing differences during the period to the extent

prudence test is met, using tax rates and tax laws that

have been enacted or substantively enacted by the

balance sheet date.

(vii) Liquidate deferred tax assets to the extent of reversal of

timing differences during the period in respect of which

they were created.

(viii) Reassess at each balance sheet date both unrecognised

and recognised timing differences. To the extent

prudence test is met, recognise deferred tax asset for

the former, using tax rates and tax laws that have been

enacted or substantively enacted by the balance sheet

date and to the extent the prudence test is not met,

write-down the carrying amount of the latter. Such writedown

can be reversed to the extent prudence test is

subsequently met.

(ix) Any deferred tax assets and liabilities previously created

and still appearing in the balance sheet because the

whole or a part of the timing differences in respect of

which they were created are yet to reverse, should be

adjusted for the effect of changes in tax laws and tax

rates, if any, enacted or substantively enacted by the

balance sheet date.

12. Thus, difference between accounting income adjusted for

permanent differences, and taxable income computed under tax

laws should be the net effect of originating as well as reversing

timing differences. As already explained, such a difference should

be analysed source-wise with further analysis into originating and

reversing differences, to ascertain and account for their deferred

tax impact. The Committee notes that this has not been followed

as per the Facts of the Case.

13. Further, the Committee notes that AS 22 has transitional

provisions, which should have been followed on the date on which

it became mandatory for the company.

14. The company should pass necessary rectification entries. For

this purpose, the company should ascertain the entries that should

have been passed in accordance with the principles stated above,

right from the time AS 22 became mandatory to it, assess their net

effect and consequential changes, if any (such as, initial adjustment of transitional deferred tax liability against debit balance in the

profit and loss account because of inadequacy of revenue reserves

and clearance of the said debit balance against subsequent profits),

and compare the same with the effect of the entries actually passed

right from the time AS 22 became mandatory. Adjustments

pertaining to previous periods should be treated as prior period

items in accordance with Accounting Standard (AS) 5, ‘Net Profit

or Loss for the Period, Prior Period Items and Changes in

Accounting Policies’. The Committee is of the view that though AS

5 deals with prior period items in the context of profit and loss

account only, the accounting principles of prior period items are

equally applicable to balance sheet items also.

15. As regards ‘MAT’, the Committee notes that the Institute of

Chartered Accountants of India has issued Accounting Standards

Interpretation 6, ‘Accounting for Taxes on Income in the context of

Section 115JB of the Income-tax Act, 1961’, which has been

subsequently withdrawn and the consensus of the same has been

inserted as Explanation to paragraph 21 of AS 22 notified by the

Central Government under the Companies (Accounting Standards)

Rules, 2006. This Explanation reads as below:

“Explanation:

(a) The payment of tax under section 115JB of the

Income-tax Act, 1961 (hereinafter referred to as the

‘Act’) is a current tax for the period.

(b) In a period in which a company pays tax under

section 115JB of the Act, the deferred tax assets

and liabilities in respect of timing differences arising

during the period, tax effect of which is required to

be recognised under this Standard, is measured

using the regular tax rates and not the tax rate under

section 115JB of the Act.

(c) In case an enterprise expects that the timing

differences arising in the current period would

reverse in a period in which it may pay tax under

section 115JB of the Act, the deferred tax assets

and liabilities in respect of timing differences arising during the current period, tax effect of which is

required to be recognised under AS 22, is measured

using the regular tax rates and not the tax rate under

section 115JB of the Act.”

16. As regards the computation of timing differences in the context

of ‘MAT’, the Committee notes that section 115JB is an independent

section which operates in a particular situation where the tax

payable under the normal provisions is less than 10 per cent of

the book profit as determined under that section. The ‘book profit’

for the purposes of ‘MAT’ may or may not be equal to accounting

income. Section 115JB does not in any way alter the taxable

income computed under the normal provisions of the tax law.

17. From the above, the Committee is of the view that while

arriving at timing differences, treatment of items of income and

expense for accounting purposes should be compared with the

treatment of such items for computation of taxable income under

the normal provisions of tax law. Those differences, if any, which

are not permanent in nature, will be timing differences. Treatment

of incomes and expenses for computation of book profit for the

purposes of MAT is irrelevant for computing timing differences.

The timing differences should be analysed item-wise and also

further analysed into originating and reversing differences.

D. Opinion

18. On the basis of the above, the Committee is of the following

opinion on the issues raised in paragraph 6 above:

(i) The company should have followed the proper approach

to deferred tax accounting as explained above. Since

this was not done, necessary rectification entries as

stated in paragraph 14 above should be passed.

Thereafter, the reversal of the deferred tax liability

created in accordance with the aforesaid procedure

should be done, if appropriate, as explained in the above

paragraphs.

(ii) Book profit as per the provisions of MAT should not be

considered as taxable income for the purposes of AS 22. Differences in treatment of items of expenses and

income for accounting purposes as compared to

computation of income for tax purposes under normal

tax provisions (instead of computation of book profit for

MAT purposes), which are not permanent in nature,

should be considered in arriving at timing differences in

the year of payment of MAT.

Annexure

1 Opinion finalised by the Committee on 30.5.2008

|