|

A. Facts of the Case

1. A company is engaged in retail business operations over the

years. The company has been in footwear business since 1965

and has entered into Large Format Retail (hereinafter referred to

as ‘LFR’) business from the year 2005. Both the business lines

have been operated through ‘Hub ‘n Spoke’ module. At present

the footwear business of the company is being operated through

wholesale and retail outlets, and distribution centres across 22

Indian states and one manufacturing unit at Kolkata. Approximately

80% of the total footwear products traded under the company’s

brand name are procured from outside suppliers and the rest 20%

are manufactured at the company’s own manufacturing unit. Under

LFR business, the large number of rapidly changing merchandise

includes apparels, home need items, grocery items, etc. and the stores have been operated with a central warehouse. 100 per cent

of the products traded under LFR business are procured from

outside suppliers.

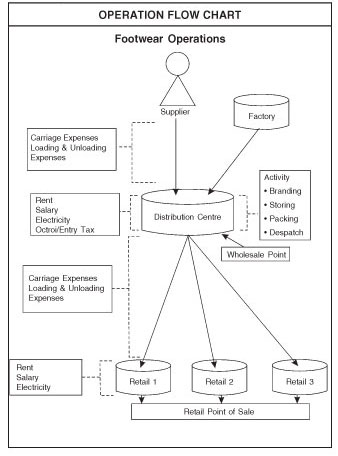

2. The operation activity flow of the company is as follows:

Footwear division:

(i) All finished goods are either manufactured at company’s

factory or procured from outside suppliers.

(ii) Purchased finished goods are branded and packed at

company’s own distribution centres either for further

despatch to the retail locations of sales across the

country or sold in bulk under wholesale terms at the

distribution centres itself.

(iii) Finished goods despatched to retail outlets from

distribution centres are stored at retail locations for sale

in due course.

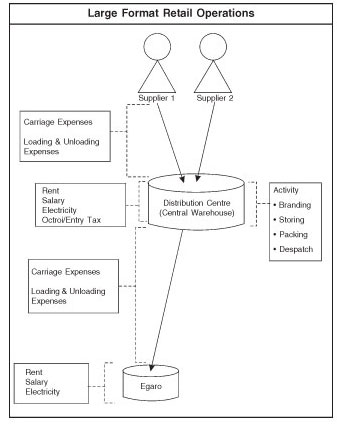

LFR division:

(i) Life style retail merchandise are procured from outside

suppliers.

(ii) Own branded merchandise are branded and packed at

supplier end.

(iii) Suppliers deliver merchandise, both own brand or other

brand, either at central warehouse or direct to stores

locations.

(iv) Merchandise received in central warehouse is affixed

with bar code, packed and forwarded to stores locations.

(v) From stores location, own brand and other brand,

merchandise are sold to retail customers.

3. As per the querist, the method and basis of inventory valuation

presently followed are as below:

(i) In line with Accounting Standard (AS) 2, ‘Valuation of

Inventories’, paragraph 18, inventories at different locations are considered under cost method for

measurement of value.

(ii) Similarly, the value of inventories has been assigned by

using FIFO formula as per paragraph 16 of AS 2.

4. The operation flow charts of both the divisions are as follows:

B. Query

5. The querist has sought the opinion of the Expert Advisory

Committee on the following issues:

(i) Whether rent, electricity and salary of the personnel

working for footwear distribution centres (DCs) where

merchandise are branded, packed and stored primarily before despatch towards retail point of sales, should be

considered in determining cost of footwear inventory at

DC level. (Emphasis supplied by the querist.)

(ii) As the company is operating through ‘Hub ‘n Spoke’

module, whether, carriage inwards cost and loading and

unloading costs incurred at footwear retail outlet points

in bringing the inventories to their present condition and

location, on being despatched from distribution centers,

should be included in determining cost of inventory at

footwear retail level. (Emphasis supplied by the querist.)

(iii) Whether rent and part of electricity charges that is directly

relatable to footwear storage, paid for footwear retail

outlets where merchandise has to be stored, as per

retail industry business practices, irrespective of

merchandise type/nature, time of sale, quantum of sale,

should be considered in determining cost of inventory

at footwear retail level. It is also to be considered that

goods have to be kept and maintained at retail store for

a considerable time before sale. (Emphasis supplied by

the querist.)

(iv) Whether rent, electricity charges and salary of

procurement and merchandising staff should be

considered in arriving at landed cost of merchandise

held at LFR–DC. [At LFR - DC major activities are (a)

branding, (b) tagging, (c) packing (d) storing and (e)

despatch to LFR retail store.] (Emphasis supplied by

the querist.)

(v) Whether rent, salary of logistics staff and portion of

electricity charges that is directly relatable to

merchandise storage at LFR store should be considered

in arriving at landed cost of merchandise held at LFR

store. [At LFR store major activities are (a) merchandise

supply chain management at store level, (b) storing, (c)

merchandise display and (d) sale. In LFR business,

numerous and variety of merchandise, backed by

intelligent logistics support, has to be maintained and carried at store level as per industry demand.] (Emphasis

supplied by the querist.)

C. Points considered by the Committee

6. The Committee notes that the basic issue raised by the querist

relates to inclusion of certain items as costs of inventories in

distribution centres (hereinafter referred to as ‘DCs’) and retail

outlets of Footwear and LFR businesses. Therefore, the Committee

has examined only this issue and has not examined any other

issue that may be contained in the Facts of the Case, such as,

valuation of inventories, cost formula, etc. Further, the Committee

restricts itself to the specific activities mentioned by the querist in

the issues raised. The Committee also notes that the querist has

used the expression ‘landed cost of merchandise’ in the Facts of

the Case without explaining its meaning. The Committee, in its

opinion given hereinafter, has considered the expenses referred to

in this regard from the point of view of whether the same should

be included in the cost of inventories concerned.

7. The Committee notes that the Institute of Chartered

Accountants of India has issued Accounting Standard (AS) 2,

‘Valuation of Inventories’, which has also been notified by the

Central Government under the Companies (Accounting Standards)

Rules, 2006. The Committee notes the following paragraphs from

AS 2:

“6. The cost of inventories should comprise all costs of

purchase, costs of conversion and other costs incurred

in bringing the inventories to their present location and

condition.

Costs of Purchase

7. The costs of purchase consist of the purchase price

including duties and taxes (other than those subsequently

recoverable by the enterprise from the taxing authorities),

freight inwards and other expenditure directly attributable to

the acquisition. Trade discounts, rebates, duty drawbacks and

other similar items are deducted in determining the costs of

purchase.

Costs of Conversion

8. The costs of conversion of inventories include costs

directly related to the units of production, such as direct labour.

They also include a systematic allocation of fixed and variable

production overheads that are incurred in converting materials

into finished goods…”

“11. Other costs are included in the cost of inventories only

to the extent that they are incurred in bringing the inventories

to their present location and condition. For example, it may be

appropriate to include overheads other than production

overheads or the costs of designing products for specific

customers in the cost of inventories.”

“13. In determining the cost of inventories in accordance with

paragraph 6, it is appropriate to exclude certain costs and

recognise them as expenses in the period in which they are

incurred. Examples of such costs are:

(a) abnormal amounts of wasted materials, labour, or other

production costs;

(b) storage costs, unless those costs are necessary in the

production process prior to a further production stage;

(c) administrative overheads that do not contribute to

bringing the inventories to their present location and

condition; and

(d) selling and distribution costs.”

8. From the above, the Committee notes that as per AS 2, the

cost of inventories would include costs other than cost of purchase

and cost of conversion as are incurred in bringing the inventories

to their present location and condition. The Committee is of the

view that the test for determining whether or not the cost of carrying

out a particular activity should be included in the cost of inventories

is whether the activity contributes to bringing the inventories to

their present location and condition; the nomenclature of the activity

or the place where the activity is carried out is not relevant.

9. The Committee is of the view that the term ‘distribution costs’ referred to in paragraph 13(d) of AS 2 reproduced above read with

paragraph 6 of AS 2, should be construed as distribution costs

which are incurred by the seller in making the goods available to

the buyer from the point of sale. In other words, distribution costs

used in the expression ‘selling and distribution costs’ would include

only those costs which are incurred for moving the goods from the

premises of the seller, whether from the factory or DCs or retail

outlets to the premises of the buyer. It does not include the cost of

moving the goods from the factory to DCs or from DCs to seller’s

retail outlets before sale.

10. The querist refers to the activities of the Footwear DCs as

branding (seems to be for purchased items), packing and storing

before despatch to retail outlets. The Committee is of the view

that rent, electricity and salary of the personnel working for

Footwear DCs are, in effect, product costs to the extent they are

related to branding because these are incurred in changing the

condition of the product from unbranded to branded. Since these

expenses are incurred in bringing the inventory to a saleable

condition, i.e., branded condition as intended by the management,

the same should be included in the cost of footwear inventory in

accordance with paragraph 6 of AS 2. The Committee also notes

that the above-mentioned expenses are storage cost to the extent

these are related to storage activity. Since the footwear

merchandise at the DCs are already finished goods requiring no

further processing, the storage cost incurred at the DCs is not of

the type which is necessary in the production process prior to a

further production stage. Hence, inclusion of such storage cost in

the cost of footwear inventory at DC level is prohibited by paragraph

13(b) of AS 2. As regards packing, the treatment of the aforesaid

expenses related to packing depends on whether packing material

cost itself is includible in the cost of inventories or not, which, in

turn, depends on the nature of packing.

11. As regards carriage inwards cost and loading and unloading

costs incurred at footwear retail outlet points in bringing the

inventories to their present condition and location, on being

despatched from DCs, the Committee is of the view that the same

should be included in the cost of inventories at retail footwear

level as required by paragraph 11 read with paragraph 6 of AS 2,

whether or not ‘Hub ‘n Spoke’ module is operated. For the reasons stated in paragraph 9 above, the Committee is of the view that these

are not ‘distribution costs’ mentioned in paragraph 13(d) of AS 2.

12. The Committee notes that at the footwear retail outlets, the

footwear merchandise are already finished goods requiring no

further processing. Hence, the cost of storing such goods in the

retail outlets is not of the type which is necessary in the production

process prior to further production stage. Hence, rent and part of

electricity charges, whether or not directly relatable to footwear

storage, paid for footwear retail outlets should not be included in

the cost of footwear inventory at the retail level as the inclusion of

the same is prohibited by paragraph 13(b) of AS 2.

13. The querist states that at the LFR – DC (which is the central

warehouse), major activities are (a) branding, (b) tagging, (c)

packing (d) storing and (e) despatch to LFR retail store. All

merchandise at LFR-DC are meant for despatch to retail outlets.

The Committee is of the view that to the extent the activities of the

procurement and merchandising staff are related to branding, the

salary of staff would be product costs for the reasons stated in

paragraph 10 above and, hence, should be considered in arriving

at the cost of inventories held at LFR-DC. Further, the Committee

is of the view that to the extent their activities are related to

tagging, their salary would also be product costs. In reaching this

conclusion, the Committee presumes that ‘tagging’ refers to

attaching a tag containing price and dimension details etc., to the

product as required under various laws, such as the Standards of

Weights and Measures Act, 1976 and, therefore, the Committee

is of the view that to attach a tag is a legal requirement to bring

the product to a saleable condition and is not an activity to promote

sales. To the extent the activities of the procurement and

merchandising staff are related to packing, the treatment of their

salary depends on whether the packing material cost itself is

includible in cost of inventories or not, which, in turn, depends on

the nature of packing. Since no further processing activity takes

place in LFR-DC, storage costs incurred at LFR-DC are not of the

type which is necessary in the production process prior to further

production stage. Inclusion of the same in the cost of inventories

is prohibited by paragraph 13(b) of AS 2. Hence, to the extent, the

activities of the procurement and merchandising staff are related to storage activities at LFR-DC, their salary should not be

considered in arriving at the cost of inventories held at LFR-DC.

For the reasons stated in paragraph 9 above, despatch to retail

outlets is not a distribution activity. To the extent the activities of

the procurement and merchandising staff are related to despatch

to retail stores, their salary should not be considered in arriving at

the cost of inventories held at LFR-DC which are meant for

despatch to retail stores. However, such cost should be considered

in arriving at the cost of inventories held at retail outlets as required

by paragraph 11 read with paragraph 6 of AS 2 since this

expenditure is incurred in changing the location of the merchandise,

i.e., bringing the inventories to the intended point of sale. The

above principles in respect of salary of procurement and

merchandising staff are equally applicable for rent and electricity

charges incurred at LFR-DC.

14. The Committee notes that at LFR stores, the merchandise

are already finished goods, not requiring any further processing.

Therefore, the storage cost is not a cost of the type which is

necessary in the production process prior to further production

stage. Inclusion of the same in the cost of inventory is prohibited

by paragraph 13(b) of AS 2. Consequently, rent, salary of logistics

staff and portion of electricity charges, whether or not directly

relatable to merchandise storage at LFR store, should not be

considered to derive the cost of inventory held at LFR store.

D. Opinion

15. On the basis of the above, the Committee is of the following

opinion on the issues raised in paragraph 5 above:

(i) Rent, electricity and salary of the personnel working for

Footwear DCs related to the activities of branding should

be considered in determining cost of footwear inventory

at DC level. To the extent these expenses are related to

storing, the same should not be considered in

determining cost of footwear inventory at DC level. As

regards packing, these expenses related to the same

can be included in the cost of the said inventory, if the

packing material cost itself is includible, which, in turn,

depends on the nature of packing.

(ii) Carriage inwards cost and loading and unloading costs

incurred at footwear retail outlet point in bringing the

inventories to their present condition and location, on

being despatched from distribution centres, should be

included in determining cost of inventory at footwear

retail level. This will be so whether or not ‘Hub ‘n Spoke’

module is operated.

(iii) Rent and part of electricity charges, whether or not

directly relatable to footwear storage, paid for footwear

retail outlets where merchandise have to be stored, as

per retail industry business practices, irrespective of

merchandise type/nature, time of sale, quantum of sale,

should not be considered in determining cost of inventory

at footwear retail level.

(iv) Rent, electricity charges and salary of procurement and

merchandising staff related to branding and tagging

activities should be considered in arriving at the cost of

inventories at LFR–DC as discussed in paragraph 13

above. To the extent these expenses are related to

storing, the same should not be considered in arriving

at the cost of inventories held at LFR-DC. As regards

packing, expenses related to the same can be

considered in arriving at the cost of inventories, if the

packing material cost itself is includible, which, in turn,

depends on the nature of packing. As regards despatch

to retail stores, to the extent the above expenses are

related to the said activity, the same should not be

considered in arriving at the cost of inventories held at

LFR-DC meant for despatch to retail stores, rather the

same should be considered in arriving at the cost of

inventories held at retail outlets.

(v) Rent, salary of logistics staff and portion of electricity

charges, whether or not directly relatable to merchandise

storage at LFR store, should not be considered in arriving

at the cost of inventories held at LFR store.

|