|

A. Facts of the Case

1. A company is a State Government undertaking registered

under the Companies Act, 1956. It has exclusive privilege of

supplying by wholesale and retail, Indian Manufactured Foreign

Sprit [IMFS] and beer items throughout the State. It has about

6700 retail vending shops, 41 IMFS depots, 33 district managers’ offices, and 5 senior regional managers’ offices throughout the

State.

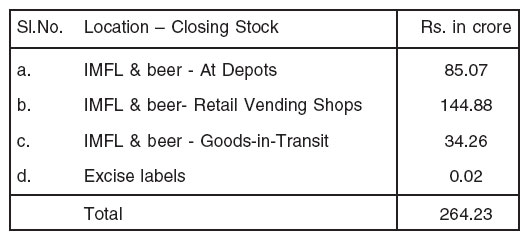

2. The company procures IMFS from 6 major suppliers and beer

from 3 suppliers. Purchase orders are placed with the

manufacturers/suppliers on the first of every month taking into

account the average sales of previous three months and goods-intransit

at the end of previous month. Further indents are issued

daily to the manufacturers/suppliers taking into account the stock

position at retail vending shops, depots and other seasonal

requirements (emphasis supplied by the querist).

3. The querist has stated that on receipt of indents, the

manufacturers/suppliers will pay State excise duty to the credit of

Government and then desptach the IMFS and beer products from

their factory/godown to the depots of the company as instructed/

directed. The invoice of the manufacturers/suppliers contains the

basic price, excise duty, trade discount on basic price and sales

tax on the net basic price and excise duty.

Vend Fee

4. The querist has informed that while issuing the indents, the

company also pays vend fee @ Rs.142 per case for IMFS and Rs.

36 per case for beer. This payment is due by virtue of Tamil Nadu

IMFS [Supply by Whole Sale] Rules, 1983. The relevant charging

rule, Rule 15(1A) as amended by Government Order G.O. Ms. No.

323 dated 10.9.2004 is reproduced hereunder:

“ In addition to the excise duty or countervailing duty, as the

case may be, paid in accordance with the provisions of subrule

(1) above, a vend fee at the rates specified below shall

also be collected from the licensee on the stock of Indian

Made Foreign Spirit received from the manufacturing units

inside the State or outside the State or removed from the

bonded warehouse licensed under the Tamil Nadu Indian Made

Foreign Spirit [Storage in Bond] Rules, 1981".

The querist has stated that in the present case, the licensee is the

company. Further, in the Rules, anywhere, no time-limit has been

prescribed for the payment of vend fee. By virtue of the said Rule 15(1A), since this has to be paid on the receipt of stock from the

manufacturing units, the company has adopted the system of

making payment of vend fee at the time of raising the indents.

This practice has been adhered to due to the receipt of goods by

41 depots scattered all over the State and further the centralised

office, which places indents, is unable to control the time of the

receipt of goods at various locations of the depots. Inspite of

raising inward documents, viz., Goods Receipt Acknowledgement

by the receiving depots, due to its diversification and being scattered

all over the State and further non-computerisation and nonintegration

of these documents coupled with the volume and

frequency of placing indents (almost daily indents are placed to

the manufacturers for supply and also daily receipt of goods takes

place), the company has been adhering to the system of making

the payment of vend fee on the same day of raising the indents.

Further, it is to be noted that the vend fee is not considered for

fixing selling price to consumers. This fee is paid out of the margin

of the company (emphasis supplied by the querist).

Transport Charges and Transit Insurance

5. The cost of transport including loading charges at the suppliers

end and the unloading charges at the end of the depots of the

company are borne by the suppliers through transport contractors

(the basic price paid to the manufacturers includes transport

charges). However, the transit insurance, i.e., the charges of

insurance for the movement of stock of IMFS and beer from the

factory/godown of the manufacturers/suppliers’ point to 41 IMFS

depots located throughout the State are borne by the company.

The company avails trade discount from suppliers to meet the cost

of transit insurance. The querist has also informed that as per the

condition no.10 of terms and conditions for the supply of IMFS by

local manufacturers for purchase of IMFS and beer, the stocks

received in good and perfect condition shall only be accepted and

payment made for. Stocks which are defective either in packing or

in quality or any other aspect during visual examination at the time

of delivery shall be rejected straightaway and such stock shall be

disposed off as per the rules in force. Similar conditions are included

in the case of supply of beer by local manufacturers (vide condition No.9 (a)), and import of IMFS from outside the State (vide condition

No.17). Hence, according to the querist, it may be noted that the

title over the goods passes on to the company only on receipt of

goods in good condition.

Fixation of Selling Price

6. The mode of fixation of selling price for IMFS and beer has

been supplied by the querist for the perusal of the Committee,

wherein, as per the querist, it is clear that the vend fee has not

figured as an element of cost in that fixation. It is paid by the

company out of its margin.

Transport of Goods to Retail Shops

7. The goods received at depots are transferred to retail vending

shops, which are managed by the company [as branches]. The

transport charges for these internal transfers to retail vending shops

are borne by the company. Further, stocks lying at depots and

retail vending shops are insured (for fire, flood, burglary, etc.) by

the company along with other risks, viz., cash in safe, money-intransit,

fire, fidelity, etc.

Valuation of Stock at Depots and Retail Vending Shops

8. As per the querist, the company has been valuing the closing

stock at lower of cost or market price and also based on the

principles laid down in Accounting Standard (AS) 2, ‘Valuation of

Inventories’. The inventory as on 31.03.2007 was at Rs. 264.23

crore as detailed hereunder:

Vend fee included in the ‘goods in transit’ is Rs. 2.84 crore and

vend fee included in the closing stock at depots and at retail

vending shops is Rs. 19.06 crore.

9. The cost elements considered for valuation of inventory are:

(i) Basic price paid to manufacturer (net of trade discount)

which also includes transport charges.

(ii) Excise duty paid by the manufacturer.

(iii) Sales tax paid by the manufacturer on above.

(iv) Amount incurred on transit insurance by the company.

These elements of cost are applied for valuation of inventory lying

in retail vending shops also.

Treatment of Vend Fee in the accounts

10. The company is paying vend fee on IMFS @ Rs. 142 per

case and on beer @ Rs. 36 per case at the time of issue of

indents as stated in earlier paragraphs. The said vend fee has

been charged to the profit and loss account as and when the

same has been incurred. However, at the end of the financial year

[say 31st March of every year], vend fee paid on the goods-intransit

has been treated in the accounts as ‘prepaid expenses’ on

the stand that the liability for payment of vend fee shall arise only

on the receipt of goods.

Recognition of goods-in-transit in books of account

11. The company has been recognising ‘goods-in-transit’ in the

books of account at the year-end on receipt of invoice.

B. Query

12. The querist has sought the opinion of the Expert Advisory

Committee on the following issues, considering paragraph 6 of AS

2, dealing with cost of inventories:

(a) Whether the vend fee (which is paid out of the profit)

and the transport cost [including loading and unloading]

incurred by the company for moving the goods from depots to retail vending shops can be included in the

term ‘cost of purchase’ or ‘other costs incurred in bringing

the inventories to their present location and condition’

and be taken as an element of cost for the purpose of

valuation of closing stock both at depots and retail shops.

In case of inclusion of the vend fee as an element of

cost in valuing the closing stock, what would be the

accounting treatment in the year in which it is

implemented [i.e., measurement and impact of such cost

on the opening stock]?

(b) For the year 2006-07, the Accountant General during

the supplementary audit of accounts under section 619(4)

of the Companies Act, 1956 objected to the treatment

of ‘prepaid expenses’ for the vend fee incurred on the

goods-in-transit and the company has revised its

accounts by charging these expenses to profit and loss

account disclosing the fact and also with a specific

mention that this will be referred to the Institute of

Chartered Accountants of India (ICAI) for expert opinion.

What would be the correct treatment in accounts with

regard to recognition of ‘goods-in-transit’, and the vend

fee paid on such goods-in-transit?

C. Points considered by the Committee

13. The Committee while answering the query has addressed

only the issues raised in paragraph 12 above and has not touched

upon any other issue arising from the Facts of the Case, such as,

appropriateness of the accounting policy of the company with

respect to valuation of closing stock at lower of cost or market

price, etc.

14. The Committee notes the following paragraphs from AS 2:

“6. The cost of inventories should comprise all costs of

purchase, costs of conversion and other costs incurred

in bringing the inventories to their present location and

condition.

Costs of Purchase

7. The costs of purchase consist of the purchase price

including duties and taxes (other than those subsequently

recoverable by the enterprise from the taxing authorities),

freight inwards and other expenditure directly attributable to

the acquisition. Trade discounts, rebates, duty drawbacks and

other similar items are deducted in determining the costs of

purchase.

Costs of Conversion

8. The costs of conversion of inventories include costs

directly related to the units of production, such as direct labour.

They also include a systematic allocation of fixed and variable

production overheads that are incurred in converting materials

into finished goods…”

“11. Other costs are included in the cost of inventories only

to the extent that they are incurred in bringing the inventories

to their present location and condition. For example, it may be

appropriate to include overheads other than production

overheads or the costs of designing products for specific

customers in the cost of inventories.”

“13. In determining the cost of inventories in accordance with

paragraph 6, it is appropriate to exclude certain costs and

recognise them as expenses in the period in which they are

incurred. Examples of such costs are:

(a) abnormal amounts of wasted materials, labour, or other

production costs;

(b) storage costs, unless those costs are necessary in the

production process prior to a further production stage;

(c) administrative overheads that do not contribute to

bringing the inventories to their present location and

condition; and

(d) selling and distribution costs.”

15. From the above, the Committee notes that as per AS 2, the

cost of inventories would include costs, apart from the cost of

purchase and cost of conversion, that are incurred in bringing the

inventories to their present location and condition. The Committee

is of the view that the test for determining whether or not the cost

of carrying out a particular activity should be included in the cost

of inventories is whether the activity contributes to bringing the

inventories to their present location and condition; the nomenclature

of the activity or the place where the activity is carried out is not

relevant.

16. The Committee is of the view that the term ‘distribution costs’

referred to in paragraph 13(d) of AS 2 reproduced above read with

paragraph 6 of AS 2, should be construed as distribution costs

which are incurred by the seller in making the goods available to

the buyer from the point of sale. In other words, distribution costs

used in the expression ‘selling and distribution costs’ would include

only those costs which are incurred for moving the goods from the

premises of the seller, whether from the branches or depots or

retail outlets to the premises of the buyer. Thus, the costs incurred

in moving the goods from the manufacturers’/ suppliers’ factory to

depots or from depots to seller’s retail outlets before sale, should

be construed as the costs incurred in bringing the inventories to

their present location and condition and, therefore, should be

included as part of the cost of inventories. The Committee is

further of the view that the expenditure incurred towards loading

and unloading of the material prior to effecting the sale is also

incurred to bring the inventories to their present location and

condition and, therefore, should be considered as element of cost

of inventory. However, to the extent the transportation and loading

and unloading costs are incurred in relation to despatch to retail

vending shops, such costs should not be considered in arriving at

the cost of inventories held at depots which are meant for despatch

to retail shops. Instead, such expenditure should be considered in

arriving at the cost of inventories held at retail shops as required

by paragraph 11 read with paragraph 6 of AS 2 since this

expenditure is incurred in changing the location of the merchandise,

i.e., bringing the inventories to the intended point of sale, i.e., the

retail vending shops.

17. As far as accounting treatment of vend fee is concerned, the

Committee is of the view that the same depends on the point of

time at which vend fee is considered to be levied on the goods as

that determines the nature of the expense. In this regard, the

Committee notes section 17-D of the Tamil Nadu Prohibition Act,

1937, which provides as follows:

“17-D. Payment of a sum in consideration of the grant of

any exclusive or other privilege or fee on licences for

manufacture or sale. – The State Government may, by rules,

levy a sum or fee or both in consideration of the grant of any

exclusive or other privilege under section 17-C and also a fee

on licences granted under section 17-C.”

(Section 17-C deals with the grant of exclusive privilege of

manufacturing, or selling by retail, or supplying by wholesale of

IMFS)

The Committee further notes that Rule 15(3) of Tamil Nadu Indian

Made Foreign Spirit (Supply by Wholesale) Rules, 1983, inter alia,

states as follows:

“An additional vend fee at the rates specified below shall also

be paid by the licensee on the quantities of IMFS and Beer

sold…”

The Committee also notes from the Facts of the Case that the

vend fee is payable on the receipt of IMFS (refer paragraph 4

above) as it is required to be ‘collected’ at that stage. From the

above, the Committee is of the view that the timing of levy of vend

fee is not clear, e.g., whether it is levied on receipt or at the point

of sale. The Committee further notes that at what point the vend

fee is levied is a legal issue. Accordingly, the same is not being

addressed as the Committee is prohibited to answer issues involving

pure interpretation of the relevant enactments under Rule 2 of its

Advisory Service Rules. Accordingly, first, it should be determined

from the legal point of view as to the point of time, the vend fee is

considered to arise. The Committee is of the view that if levy of

vend fee arises on receipt of the goods, it should be treated as

part of cost of inventories. However, if levy of vend fee arises on

sale of goods, the same should not be included as part of cost of inventories, in view of the same being a selling and distribution

cost as per paragraph 13 of AS 2.

18. As far as the treatment of goods-in-transit is concerned, the

Committee notes that paragraphs 9.14 and 9.16 of the Statement

on the Amendments to Schedule VI to the Companies Act, 1956,

issued by the Institute of Chartered Accountants of India, states

as below, although in the context of disclosure of the value of

imports of raw-materials etc., to fulfill the requirements under clause

4(D)(a)of Part II of Schedule VI:

“9.14 The value of imports should include goods which are in

transit on the balance sheet date, provided that the property

in those goods has already passed to the purchasing company.

For the purpose of determining whether or not the property

has passed, reference may be made to the terms of the

import contract, and recognised legal principles, relating to

this matter...”

“9.16 Since the requirement is to disclose the value of imports

during the accounting year, it may be necessary to determine

when the title to the goods has passed from the overseas

exporter to the Indian importer. The question as to when the

title to the goods has passed should be determined in

accordance with the well recognised legal principles relating

to this matter. The disclosure should be restricted to imports

where the title has passed within the accounting year

irrespective of whether or not payment has been made during

the year and irrespective of whether or not the goods have

been physically received during the year.”

19. The Committee further notes that in the context of recognition

of revenue from sale of goods, it has been well established from

the accounting point of view that in case there has been a transfer

of significant risks and rewards of ownership in the goods, revenue

can be recognised even though transfer of property in goods has

not taken place. In this regard, the Committee notes paragraph

6.1 of Accounting Standard (AS) 9, ‘Revenue Recognition’, as

below:

“6.1 A key criterion for determining when to recognise revenue

from a transaction involving the sale of goods is that the seller

has transferred the property in the goods to the buyer for a

consideration. The transfer of property in goods, in most cases,

results in or coincides with the transfer of significant risks and

rewards of ownership to the buyer. However, there may be

situations where transfer of property in goods does not coincide

with the transfer of significant risks and rewards of ownership.

Revenue in such situations is recognised at the time of transfer

of significant risks and rewards of ownership to the buyer.

Such cases may arise where delivery has been delayed

through the fault of either the buyer or the seller and the

goods are at the risk of the party at fault as regards any loss

which might not have occurred but for such fault. Further,

sometimes the parties may agree that the risk will pass at a

time different from the time when ownership passes.”(Emphasis supplied by the Committee.)

20. The Committee is of the view that the abovementioned

requirements recognise the primacy of substance over form which

should also be applied in case of purchases. Thus, the company

should recognise only those goods-in-transit in respect of which

significant risks and rewards of ownership have passed to the

company. The Committee is of the view that the question when

the transfer of significant risks and rewards of ownership takes

place depends on particular facts and circumstances of the case,

including the terms of the contract, express and/or implied, and

the conduct of the parties. In this regard, the Committee notes that

the querist has stated in the Facts of the Case that the cost of

transit insurance is borne by the company and that the stocks

received in good and perfect condition shall only be accepted and

payment made for. The Committee is of the view that apart from

these two factors, various other factors should also be considered

for ascertaining the timing of passing of significant risks and rewards

of ownership. For example, factors, like whether the company can

sell the goods to another party or pledge the same while these are

in transit, etc. will have to be taken into account in determining the

timing of transfer of significant risks and rewards of ownership.

21. As far as accounting treatment of vend fee paid on the goodsin-

transit is concerned, keeping in view the recommendations

contained in paragraph 17 above, it would not be considered as a

‘prepaid expense’ if the risks and rewards of ownership are passed

on to the company when the goods are in transit since it would be

considered as ‘constructive receipt’ if the point of levy of vend fee

is at the point of receipt of goods. However, if the levy of vend fee

is at the point of sale, it should be considered as prepaid expense.

D. Opinion

22. On the basis of the above, the Committee is of the following

opinion on the issues raised in paragraph 12 above:

(a) The transport cost (including loading and unloading cost)

incurred by the company form part of ‘other costs

incurred in bringing the inventories to their present

location and condition’ and should be taken as an

element of cost of inventory. However, to the extent

transportation and loading and unloading costs are

incurred in relation to despatch to retail vending shops,

such costs should not be considered in arriving at the

cost of inventories held at depots which are meant for

despatch to retail shops. Instead, such cost should be

considered in arriving at the cost of inventories held at

retail shops as discussed in paragraph 16 above. The

vend fee should be included in the cost of inventories

only when the levy of the fee is considered to arise at

the point of receipt of goods as discussed in paragraph

17 above. In such a case, the vend fee not included in

the opening stock should be considered as a ‘prior period

item’ under Accounting Standard (AS) 5, ‘Net Profit or

Loss for the Period, Prior Period Items and Changes in

Accounting Policies’ and treated accordingly.

(b) The goods-in-transit would be recognised as the

inventories of the company depending on whether the

significant risks and rewards of ownership of these goods

have been transferred to the company considering the

factors discussed in paragraph 20 above. As far as

vend fee paid on such goods-in-transit is concerned, it should be included as a part of cost of inventory only

when the liability in respect thereof arises as discussed

in paragraph 21 above.

|