|

A. Facts of the Case

1. A public sector company is manufacturing industrial chemicals

and fertilizers. In the manufacture of the same, it uses many

inputs as well as catalysts. As per design, catalysts are directly

used in the production process to facilitate reaction. As these

catalysts do not participate in the reaction these are classified as

process chemicals and consumables rather than raw material

inputs. Catalysts are of high value. Such catalysts are replaced

when their charge gets over or does not support the performance as desired. The company uses various catalysts in its production

which is product/plant specific. The charge of some of the catalysts,

normally called as the life of the catalyst, may be over in one year

whereas sometimes it gets extended up to 5-7 years. The first

charge of the catalyst is capitalised along with the plant.

2. The company prepares annual cost statements based on

absorption costing method for valuation of its stock of finished

products. As the expected life/utility of catalyst exceeds over a

year there is a scope for consideration of pro-rata cost of catalyst

based on its expected life while arriving at the cost of production

of the finished product. However, since inception, consistently the

company charges off the entire cost of catalyst replaced in the

year of its replacement. The reasons for the same are as under:

(i) The expected life is subject to innumerable and dynamic

variables of continuously running plants and material

conditions. Thus, there is no standard input-output

relationship between expected life and the quantity of

catalyst consumed.

(ii) The company has experienced erratic fluctuations in

the actual life as compared to its estimated life in all

cases.

(iii) Moreover, in every annual shutdown, the catalysts are

reviewed and some of the catalysts are topped-up, i.e.,

part replacement is done to support performance. Hence,

the company is also required to maintain inventory of

such catalysts to meet operating requirements.

(iv) Catalysts are product/plant specific, thus forming part

of direct cost of production.

(v) Once a catalyst has become completely useless, it is

disposed off as scrap.

(vi) Pro-rata charging off the cost of catalyst requires bringing

back to inventory, the quantity of catalysts already issued

to process which is highly unascertainable and

impractical.

3. The querist has informed that the company has adequately

disclosed the fact in its accounting policy in this regard as follows:

“cost of manufactured goods comprises of direct cost (including

cost of catalyst replaced during the year), variable production

overheads and fixed production overheads on absorption

costing method”.

The querist has also informed that the company’s accounting policy

also states that “the company does not value stocks in process at

the close of the year as the same is not practicable”.

4. During the year 2007-08, the Government auditors have

queried that this practice is not as per paragraph 8 of Accounting

Standard (AS) 2, ‘Valuation of Inventories’, since the company is

charging off the entire cost of catalyst in the year in which it is

incurred even though the life of the catalyst is four years. This is

resulting in abnormal expense during the first year of replacement

of catalyst. Paragraph 8 of AS 2 relates to treatment of cost of

conversion. During the year 2007-08, the company incurred a cost

of Rs. 24.71 crore for the replacement of catalyst in its ammonia

plant and has charged off the same in the accounts of the year

without spreading over the cost of catalyst for four years. This has

resulted in overstatement of finished goods (urea) and material

consumed to the extent of Rs. 1.75 crore and Rs. 18.53 crore

respectively, and understatement of profit to the extent of Rs.

16.78 crore.

5. To the above observation of the Government auditors, the

company replied that as the usage of the catalyst in production

process is not systematic, the company has been charging off the

cost of the catalyst in the year of replacement itself. The company

also argued that the expected life of the catalyst as arrived at by

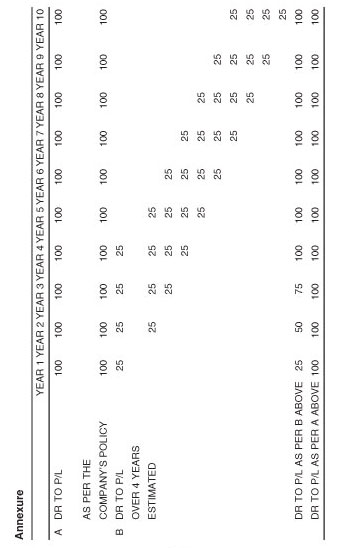

the auditors is notional. Further, as explained in Annexure I by the

querist, any other method followed would result in the same charge

to the profit and loss account.

6. The Government auditors have cleared the accounts only on

the assurance that an expert opinion on this accounting treatment

would be obtained from the Institute of Chartered Accountants of

India.

B. Query

7. The querist has sought the opinion of the Expert Advisory

Committee on the following issues arising from the above facts:

(i) Whether the company is correct in its accounting

treatment for catalysts.

(ii) Whether the current practice of the company is contrary

to paragraph 8 of AS 2.

C. Points considered by the Committee

8. The Committee, while expressing its opinion, has restricted

itself to the issues raised with regard to accounting for catalyst as

stated in paragraph 7 above and has not considered any other

issue that may raise from the Facts of the Case, such as, the

accounting policy of the company regarding not valuing the stockin-

process at the close of the year.

9. The Committee notes from the Facts of the Case that the

catalysts having high values are used in the production process.

The catalysts have a life more than one year although the life may

fluctuate considerably keeping in view the conditions in which the

same is used. Further, a catalyst may be reused after recharging

the same. Once a catalyst becomes completely useless it is

disposed off as scrap.

10. The Committee notes that a catalyst meets the definition of

an asset since it is a resource controlled by the enterprise from

which its future economic benefits are expected to flow to the

enterprise. Unless the amount of an asset is not material, it is

necessary to determine the nature of the asset in order to determine

its appropriate accounting. Keeping in view the nature of the

catalyst, the Committee is of the view that the catalysts can either

be inventories or fixed assets. In this context, the Committee notes

the definition of ‘fixed asset’ given in paragraph 6.1 of Accounting

Standard (AS) 10 ‘Accounting for Fixed Assets’, as below:

“6.1 Fixed asset is an asset held with the intention of being

used for the purpose of producing or providing goods or

services and is not held for sale in the normal course of

business.”

The Committee also notes the definition of ‘inventories’ given in

paragraph 3 of AS 2, as follows:

“Inventories are assets:

(a) held for sale in the ordinary course of business;

(b) in the process of production for such sale; or

(c) in the form of materials or supplies to be consumed

in the production process or in the rendering of

services.

11. The Committee notes from the Facts of the Case that a catalyst

only facilitates the process of production of a product. Without the

catalyst plant and machinery can still operate and the product can

still be produced. Accordingly, catalyst cannot be considered of

the nature of plant and machinery, which converts raw materials

into finished products. The catalyst is also not of the nature of an

asset which is kept for administrative use. Accordingly, the

Committee is of the view that the catalyst is not of the nature of a

fixed asset as contemplated in AS 10. On the other hand, the

Committee is of the view that the catalyst is used in the process of

production and is of the nature of supply to be consumed in the

production process. It should be considered of the nature of a

consumable even though its life may be greater than one year. In

other words, the Committee is of the view that a catalyst is covered

by the definition of the term ‘inventories’ under AS 2. Accordingly,

in the view of the Committee, the principles of AS 2 should be

applied for the purpose of measurement and presentation of

catalysts. Keeping in view the above considerations, the Committee

is of the view that the first charge of the catalyst should not be

capitalised along with the plant as being presently done by the

company.

12. From the above, the Committee is of the view that catalysts

should be valued at the lower of cost and net realisable value as

prescribed in paragraph 5 of AS 2. At the end of the year, where

the catalysts are still in use, the cost thereof to be charged under

cost of conversion as per paragraph 8 of AS 2 should be only to

the extent of catalysts consumed during the period. To the extent

the catalyst is yet to be consumed, it should be treated as inventory, for whose valuation purposes, the balance cost of the catalysts

should be compared with the net realisable value thereof. With

regard to determination of net realisable value, the Committee is

of the view that paragraph 24 of AS 2 reproduced below should be

applied:

“24. Materials and other supplies held for use in the production

of inventories are not written down below cost if the finished

products in which they will be incorporated are expected to be

sold at or above cost. However, when there has been a decline

in the price of materials and it is estimated that the cost of the

finished products will exceed net realisable value, the materials

are written down to net realisable value. In such circumstances,

the replacement cost of the materials may be the best available

measure of their net realisiable value.”

Accordingly, the Committee is of the view that the accounting

policy of the company in respect of catalyst would be correct if the

net realisable value thereof, as determined above, is nil.

D. Opinion

13. On the basis of the above, the Committee is of the following

opinion on the issues raised by the querist in paragraph 7 above:

(i) The company would be correct in its accounting treatment for

catalysts if the net realisable value as determined in accordance

with paragraph 12 above is nil.

(ii) The current practice of the company is contrary to paragraph

8 of AS 2.

|