|

A. Facts of the Case

1. A company is a joint venture between Government of India and the Government of National Capital Territory of Delhi, and is engaged in the business of construction, operation and maintenance of Mass Rapid Transit System (MRTS) in the National Capital Region.

2. The operation of MRTS involves incurrence of huge capital expenditure. Consequently, depreciation constitutes a significant element of cost of operations. Automatic Fare Collection (AFC) System used for collection of fares and the Signalling and Telecommunication (S&T) Equipments used for signalling and operation of trains are important constituents of capital cost of the MRTS.

3. Operational timings of the MRTS are from 6.00 A.M. to 11.00 P.M. Depreciation on assets including AFC and S&T equipments used in MRTS has so far been charged on the basis of single shift rates. The company has followed this practice since inception.

4. The querist has stated that during the year 2007-08, the Government auditors have raised the issue that since the MRTS is working through out the year from 6.00 A.M. to 11.00 P.M., whether the company should charge depreciation on single shift basis (i.e., @ 4.75%) on the Automatic Fare Collection (AFC) System and the Signalling and Telecommunication (S&T) equipments. The alternative view can be that depreciation on these assets should be charged on double shift basis (i.e., @ 7.42%), as the system is working in double shifts and these assets are not specifically listed in Note 6 to Schedule XIV to the Companies Act, 1956 amongst items on which extra shift depreciation need not be charged.

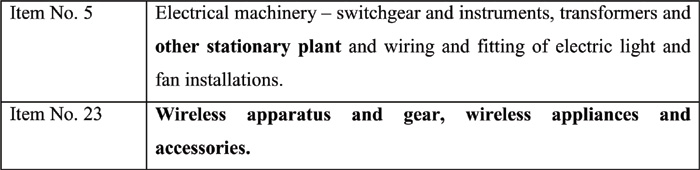

5. The view of the company is that AFC System and S&T equipments mainly consist of cables and wires, wireless apparatus and electrical stationary plant. As per the querist, such equipments are covered under item Nos. 5 and 23 of clause 6 of the Notes to Schedule XIV to the Companies Act, 1956 for which no extra shift depreciation (NESD) is to be charged. The relevant extracts from clause 6 are given below:

(Emphasis supplied by the querist.)

6. To substantiate the view of the company that the AFC and S&T equipments used in MRTS fall within the two items referred to in Schedule XIV, a report of technical experts on technical nature and structure of these systems was sought by the company. This procedure, as per the querist, is well recognised under Standard on Auditing (SA) 620 (AAS 9), ‘Using the Work of an Expert’2 , which, as per the querist, recognises that since the auditor is not expected to have the expertise of a person trained for, or qualified to engage in, the practice of another profession or occupation, such as an actuary or engineer, he is entitled to rely on work performed by others, provided he exercises adequate skill and care and is not aware of any reason to believe that he should not have so relied. The querist has drawn the attention of the Committee to paragraphs 1 and 2 of SA 620 in this respect.

7. The querist has provided the following extracts from the report of two internal experts, both of whom are stated to be Chief Engineers (S&T) and experts in telecommunication and signalling system respectively, having extensive experience in the matter. Both belong to the Indian Railways Service of Signal & Telecommunication Engineers (IRSSE) and are presently working in the company on deputation.

(a) Telecommunication System

- The telecommunication system acts as the communication backbone for signalling systems and other systems, such as, Supervisory Control and Data Acquisition (SCADA), AFC, etc. and provides telecommunication services to meet operational and administrative requirements of metro network.

- The wireless mobile radio communication system is the most significant component of the telecommunication system. Other constituents of the system are telephone exchange and Synchronous Digital Hierarchy (SDH), passenger information display and announcement system and Closed Circuit Television (CCTV) system.

(b) Automatic Fare Collection System

- The most significant constituents of Automatic Fare Collection System are the retractable type entry-exit gates provided at each station which control the entry to/exit from the station based on smart cards/tokens issued to passenger by manually-operated ticket office machines.

A copy of the report and a brief description of the professional qualifications and experience of the internal experts have been supplied by the querist for the perusal of the Committee.

8. According to the querist, from the above, it is clear that the essential nature of telecommunication system is that of wireless communication system. Hence, as per the querist, it falls under item 23 of note 6 to the Schedule XIV, i.e., wireless apparatus and gear, wireless appliances and accessories. Similarly, the automatic fare collection system consists of specialised entry/exit gates, which are in the nature of specialised stationary plant (item 5 of Note 6 to Schedule XIV).

9. The querist has stated that it would be significant to note that all major equipments, e.g., locomotives, rolling stock, etc., constituting the company’s system are depreciated at single shift rates.

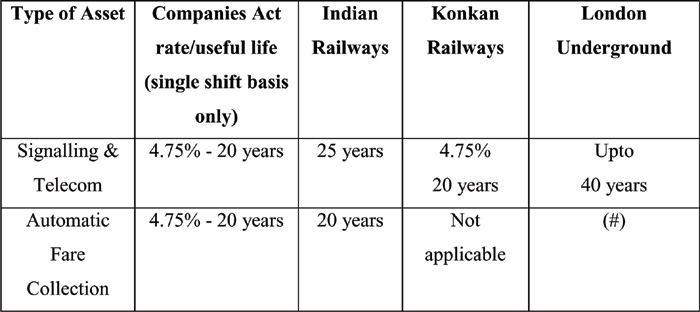

10. The querist has also mentioned that the useful life of similar equipments has been evaluated by other players in the industry on a similar basis as would be evident from the following table:

(#) AFC equipment is supplied under a private finance initiative contract.

B. Query

11. During discussion with the Member Audit Board (MAB) Office, it was agreed that the issue will be referred to the Expert Advisory Committee of the Institute of Chartered Accountants of India for its expert opinion. Accordingly, the querist has sought the opinion of the Expert Advisory Committee on the following issues:

(a) Where an engineering system is specific to the business of an undertaking, whether its nature should be a matter of expert engineer’s technical opinion in order to determine the overall category of assets listed in Schedule XIV to the Companies Act, 1956, in which the respective assets fall (so as to decide about the appropriate rate of depreciation).

(b) Assuming that the expert’s opinion is a correct analysis of the nature of AFC System and S&T equipments, whether it is reasonable to conclude that these are covered under items 5 and 23 of clause 6 of the notes to Schedule XIV to the Companies Act, 1956.

C. Points considered by the Committee

12. The Committee, while expressing its opinion, has considered only the issues raised in paragraph 11 above, viz., whether the report of a technical expert can be used while determining the overall category of assets listed in Schedule XIV to the Companies Act, 1956 and whether on the basis of the experts’ opinion obtained by the company it is reasonable to conclude that AFC System and S&T equipments are covered under items 5 and 23 of clause 26 of the Notes to Schedule XIV to the Companies Act, 1956. The Committee has not touched upon any other issue that may arise from the Facts of the Case, such as, whether the extra shift depreciation would be applicable to the company keeping in view its normal working hours, i.e., whether the working hours of the company could be called as extra shift, or the appropriateness of the depreciation policy of the company for other equipments, such as, locomotives, rolling stocks, etc.

13. The Committee notes that the basic purpose of charging depreciation is to allocate depreciable value of an asset over its useful life so as to exhibit a true and fair view of the financial statements. The Committee notes that the Guidance Note on Accounting for Depreciation in Companies, issued by the Institute of Chartered Accountants of India, provides in paragraph 9 that ‘in arriving at the rates at which depreciation should be provided the company must consider the true commercial depreciation, i.e., the rate which is adequate to write off the asset over its normal working life. If the rate so arrived at is higher than the rates prescribed under Schedule XIV, then the company should provide depreciation at such higher rate but if the rate so arrived at is lower than the rate prescribed in Schedule XIV, then the company should provide depreciation at the rates prescribed in Schedule XIV, since these represent the minimum rates of depreciation to be provided. Since the determination of commercial life of an asset is a technical matter, the decision of the Board of Directors based on technological evaluation should be accepted by the auditor unless he has reason to believe that such decision results in a charge which does not represent true commercial depreciation.” From the above, the Committee is of the view that determination of commercial life would also depend on the category of assets in which the concerned asset falls under Schedule XIV. In case of highly technical assets, in the view of the Committee, the help of an expert may be taken in determining the category of assets under Schedule XIV in which the concerned asset would fall.

14. The Committee notes that the Institute of Chartered Accountants of India has issued Standard on Auditing (SA) 620 (AAS 9), ‘Using the Work of an Expert’. This Standard recognises that an auditor may have to rely on the expertise of a person trained for, or qualified to engage in, the practice of another profession or occupation. The Standard prescribes various procedures and precautions the auditor must undertake under such circumstances. The Committee specially draws attention to the following paragraphs of SA 620 (AAS 9):

Skills and Competence of the Expert

“7. When the auditor plans to use the expert’s work as audit evidence, he should satisfy himself as to the expert’s skills and competence by considering the expert’s:

- professional qualifications, licence or membership in an appropriate professional body, and

- experience and reputation in the field in which the evidence is sought.

However, when the auditor uses the work of an expert employed by him, he will not need to inquire into his skills and competence.

Objectivity of the Expert

8. The auditor should also consider the objectivity of the expert. The risk that an expert’s objectivity will be impaired increases when the expert is:

- employed by the client, or

- related in some other manner to the client.

Accordingly, in these circumstances, the auditor should (after taking into account the factors in paragraphs 6 and 7) consider performing more extensive procedures than would otherwise have been planned, or he might consider engaging another expert.

Evaluating the Work of an Expert

9. When the auditor intends to use the work of an expert, he should examine evidence to gain knowledge regarding the terms of the expert’s engagement and such other matters as:

- the objectives and scope of the expert’s work,

- a general outline as to the specific items in the expert’s report,

- confidentiality of the expert’s work, including the possibility of its communication to third parties,

- the expert’s relationship with the client, if any,

- confidentiality of the client’s information used by the expert.

10. The auditor should seek reasonable assurance that the expert’s work constitutes appropriate audit evidence in support of the financial information, by considering:-

- the source data used,

- the assumptions and methods used and, if appropriate, their consistency with the prior period, and

- the results of the expert’s work in the light of the auditor’s overall knowledge of the business and of the results of his audit procedures.

The auditor should also satisfy himself that the substance of the expert’s findings is properly reflected in the financial information.

The auditor should also satisfy himself that the substance of the expert’s findings is properly reflected in the financial information.

11. The auditor should consider whether the expert has used source data which are appropriate in the circumstances. The procedures to be applied by the auditor should include:

- making inquiries of the expert to determine how he has satisfied himself that the source data are sufficient, relevant and reliable, and

- conducting audit procedures on the data provided by the client to the expert to obtain reasonable assurance that the data are appropriate.

12. The appropriateness and reasonableness of assumptions and methods used and their application are the responsibility of the expert. The auditor does not have the same expertise and, therefore, cannot always challenge the expert’s assumptions and methods. However, the auditor should obtain an understanding of those assumptions and methods to determine that they are reasonable based on the auditor’s knowledge of the client’s business and on the results of his audit procedures.”

15. With respect to the issue raised by the querist in paragraph 11(b) above, the Committee is of the view that the report of the technical experts submitted in the present case regarding the nature of AFC System and S&T equipments is not technically complete as only the functions of the relevant assets have been discussed in the said report. No technological arguments have been given in the report to support (or otherwise) inclusion of the said items of assets under item nos. 5 and 23 of clause 6 of the Notes to Schedule XIV to the Companies Act, 1956. Accordingly, no conclusion can be drawn from the said report. In any case, the Committee is of view that the auditor will have to assess the reliability of the report of the experts keeping in view the discussion in paragraph 14 above.

D. Opinion

16. On the basis of the above, the Committee is of the following opinion on the issues raised by the querist in paragraph 11 above:

(a) The services of a technical expert may be used for determining the category of assets listed in Schedule XIV to the Companies Act, 1956, subject to the considerations/discussion in paragraph 14 above.

(b) In the present case, the experts’ report is not technically complete as discussed in paragraph 15 above. Accordingly, no conclusion can be drawn from the said report regarding inclusion of AFC System and S&T equipments under items 5 and 23 of clause 6 of the notes to Schedule XIV to the Companies Act, 1956. In any case, the auditor will have to assess the reliability of the report of the experts keeping in view the discussion in paragraph 14 above.

|