|

A. Facts of the Case

1. A public sector company is engaged in construction of ships and ship repair activities. The company has an accumulated loss of Rs.847.42 crore as on 01.04.08 and a deferred tax asset of Rs.102.36 crore. As per the Income-tax Returns filed by the company and income tax assessments, the amount of unabsorbed depreciation and carried forward losses of the company is Rs. 255.51 crore. The company has also realised deferred tax asset to the extent of Rs.6.66 crore in the financial year 2007-08.

2. During the audit of accounts of the company for the financial year 2007-08, the government auditor had raised an observation in respect of accounting for deferred tax asset and issued a provisional comment as follows:

“As per paragraph 17 of Accounting Standard (AS) 22, ‘Accounting for Taxes on Income’, where an enterprise has unabsorbed depreciation or carry forward of losses under tax laws, deferred tax assets should be recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which deferred tax assets can be realised. Inspite of non-existence of virtual certainty supported by convincing evidence of availability of future taxable income and carrying an unabsorbed depreciation of Rs.13,019.94 lakh as on 31.03.08, the company recognised deferred tax asset. This has resulted in overstatement of deferred tax assets and profit after taxation, and understatement of accumulated losses by Rs.11,446.90 lakh.”

3. The company replied to the government auditor that there exists virtual certainty that sufficient future taxable income will be available for realising the above-mentioned deferred tax asset based on the following facts:

(a) The company has secured an order from Indian Navy for refit and modernisation of a submarine for a contract value of Rs.629 crore on nomination basis. As a part of this contract, the Indian Navy has catered Rs.50 crore for creating additional infrastructural facilities and it has been agreed in the contract on the modus operandi for amortisation of the said amount of Rs.50 crore over the future medium refits / normal refits. This fact confirms the existence of future profitable orders from Indian Navy in addition to the existing order.

(b) The company secured profitable orders for construction of six 53000 DWT Bulker for an order value of Rs.625.28 crore. The total ship-building order book position at present is around Rs.970 crore.

(c) The company also diversified its activities into repair of oil rigs and successfully acquired this expertise and completed the repairs of Jack-up Rig (JUR) of a company at a cost of more than Rs.100 crore. Recently, the company also secured another order for repair of another JUR of the same company at a contract price of Rs.361 crore. The company expects a series of such repair orders continuously.

(d) The financial restructuring proposal of the company is in the advanced stage of consideration by the Government of India. The said proposal has been submitted by the administrative ministry, the Ministry of Shipping, Road Transportation & Highways to the Cabinet Committee on Economic Affairs for their approval. The proposal envisages sanction of grants waiver of loans and interests amounting to Rs.1,03,200 crore. On approval of the proposal, the said amount will be credited to the profit and loss account as income and the company will immediately realise the entire deferred tax asset accounted for in the previous years.

(e) The books of account are prepared under ‘going concern concept’.

(f) Further to the above, the querist has submitted that an amount of Rs.141.15 crore representing the items covered under section 43B of the Income-tax Act, 1961 which shall be disallowed for computation of tax for the assessment year 2008-09, shall be allowed as expenditure in the year of payment without any time limit. Accordingly, as per the querist, virtual certainty exists for realisation of deferred tax assets in respect of these items amounting to Rs.47.98 crore.

(g) As regards provisions made in the accounts for liquidated damages, doubtful advances, guarantee repairs and other contingencies which shall be disallowed at the time of assessment, shall be allowed in the year of crystallisation of the expenditure without any time limit. Hence, the deferred tax asset so provided amounting to Rs.18.09 crore shall be realised with certainty.

(h) The querist has also submitted that there exists unabsorbed depreciation under the Income-tax Act, 1961 available for set-off in the future years to the tune of Rs.130.20 crore and the deferred tax asset on the said amount of unabsorbed depreciation would be Rs.44.25 crore, which will also be realised with certainty, since, according to the querist, as per the Income-tax Act, 1961, the unabsorbed depreciation can be set off without any time limit in accordance with section 32(2) of the Act. The querist has further submitted that the company is having brought forward losses to the tune of Rs.185.00 crore and deferred tax asset in respect of the same has not been considered since there is a time limit of 8 years for absorption of the same as per the Income-tax Act, 1961.

Based on the above facts, the company is of the view that there exists virtual certainty with convincing evidence that the company will have taxable income in the immediate future and will be able to realise the deferred tax assets.

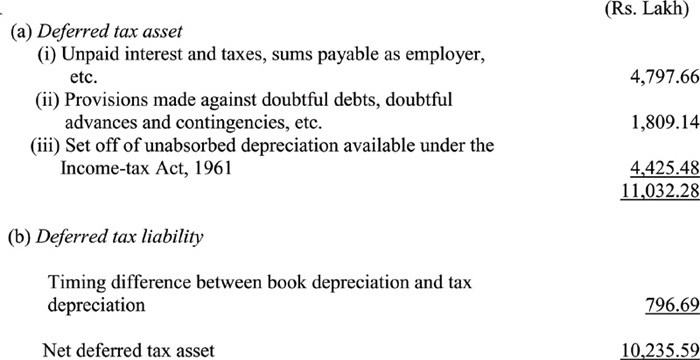

4. The querist has mentioned that the deferred tax asset as at 31-3-2008 comprises the following:

5. The querist has stated that having examined the management’s contention mentioned at paragraph 3(a) to (d) above in the light of specific clarifications of Accounting Standards Interpretation (ASI) 92 , ‘Virtual certainty supported by convincing evidence’, issued by the Institute of Chartered Accountants of India, read with specific provisions in paragraphs 17, 18 and 32 of AS 22, and also in the light of the past trend that ship-building activity of the company was a loss making activity, the auditor opined that there does not exist virtual certainty with convincing evidence in a concrete form as on the date of the balance sheet, i.e., on 31st March, 2008 about the company having taxable income in the immediate future and hence, the accounting for deferred tax assets is not in line with AS 22.

6. The company replied to the government auditor that considering that most of the ship-building orders are profitable and further, submarine refit order and all ship repair orders including major repair orders, such as, lay-up repairs of rigs are profit making, the deferred tax assets are realisable based on the overall profitability of the company. Since there is a virtual certainty of earning future profits which would realise the deferred tax assets recognised in the accounts, the accounting for deferred tax assets is in line with AS 22.

B. Query

7. The querist has sought the opinion of the Expert Advisory Committee as to whether the accounting for deferred tax assets by the company is in compliance with AS 22, based on the inputs as stated above in respect of virtual certainty of future taxable income.

C. Points considered by the Committee

8. The Committee notes that the basic issue raised in the query relates to recognition of deferred tax asset in situations of unabsorbed depreciation and brought forward losses. The Committee has, therefore, considered only this issue and has not touched upon any other issue arising from the Facts of the Case, such as, offsetting of deferred tax assets and deferred tax liabilities, propriety of accounting to be done by the company in respect of expected grants/waiver of loans and interests, etc. Further, the Committee’s opinion is based on accounting principles and it has not gone into the calculations or computation of deferred tax assets.

9. The Committee notes paragraphs 17 and 18 of AS 22, which provide as below:

“17. Where an enterprise has unabsorbed depreciation or carry forward of losses under tax laws, deferred tax assets should be recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised.

18. The existence of unabsorbed depreciation or carry forward of losses under tax laws is strong evidence that future taxable income may not be available. Therefore, when an enterprise has a history of recent losses, the enterprise recognises deferred tax assets only to the extent that it has timing differences the reversal of which will result in sufficient income or there is other convincing evidence that sufficient taxable income will be available against which such deferred tax assets can be realised. In such circumstances, the nature of the evidence supporting its recognition is disclosed.”

10. The Committee further notes that AS 22 notified by the Central Government under the Companies (Accounting Standards) Rules, 2006, contains, inter alia, an Explanation to paragraph 17 thereof regarding virtual certainty (which was hitherto contained in the consensus portion of ASI 9) which provides as below:

“Explanation:

1. Determination of virtual certainty that sufficient future taxable income will be available is a matter of judgement based on convincing evidence and will have to be evaluated on a case to case basis. Virtual certainty refers to the extent of certainty, which, for all practical purposes, can be considered certain. Virtual certainty cannot be based merely on forecasts of performance such as business plans. Virtual certainty is not a matter of perception and is to be supported by convincing evidence. Evidence is a matter of fact. To be convincing, the evidence should be available at the reporting date in a concrete form, for example, a profitable binding export order, cancellation of which will result in payment of heavy damages by the defaulting party. On the other hand, a projection of the future profits made by an enterprise based on the future capital expenditures or future restructuring etc., submitted even to an outside agency, e.g., to a credit agency for obtaining loans and accepted by that agency cannot, in isolation, be considered as convincing evidence.”

11. On the basis of the above, the Committee is of the view that the orders secured by the company, as mentioned by the querist in paragraphs 3(a) to (c) above, may be considered while creating deferred tax asset provided these are binding on the other party and it can be demonstrated that they will result in future taxable income. However, mere projections made by the company indicating the earning of profits from future orders contemplated in paragraphs 3(a) and (c) above, or financial restructuring proposal under consideration of the Government of India or the fact that the books of account of the company are prepared on ‘going concern’ basis as mentioned by the querist in paragraphs 3(d) and (e) respectively, may not be considered as convincing evidence of virtual certainty as contemplated in the ‘Explanation’ to paragraph 17 of AS 22 reproduced above. Further, the mere fact that the items covered under section 43B of the Income-tax Act, 1961, the provision for liquidated damages, doubtful advances, guarantee repairs and other contingencies, and unabsorbed depreciation can be carried forward for unlimited number of years, can also not be a ground for recognising a deferred tax asset, as mentioned by the querist in paragraphs 3(f), (g) and (h) respectively, since paragraph 17 of AS 22 read with its ‘Explanation’, requires virtual certainty supported by convincing evidence at the date of the balance sheet. The Committee also wishes to point out that a deferred tax asset can be created to the extent that future taxable income will be available from future reversal of any deferred tax liability recognised at the balance sheet date. To that extent, it would not be necessary to consider the level of virtual certainty supported by convincing evidence.

D. Opinion

12. On the basis of the above, the Committee is of the opinion that subject to paragraph 8 above, accounting for deferred tax asset by the company would be in compliance with AS 22 only to the extent it is in accordance with paragraph 11 above.

1Opinion finalised by the Committee on 24.08.2009

2The ASI has been withdrawn by the Council of the Institute of Chartered Accountants of India and the Consensus portion thereof has been added as ‘Explanation 1’ to the paragraph 17 of AS 22.

|