|

A. Facts of the Case

1. A company was incorporated in the year 1976 as a wholly owned Government of India enterprise under the administrative control of the Ministry of Power to plan, promote, investigate, survey, design, construct, generate, operate and maintain hydro and thermal power stations and to explore and utilise the power potential of North East in particular. The company is presently running three hydro projects and two thermal projects in north-eastern States and is catering to the demand of north-eastern States only. The company’s shares are not listed with any stock exchange. The authorised and paid up share capital of the company as on 31.03.2008 are Rs. 3500 crore and Rs. 3178.93 crore, respectively. The turnover of the company for the year ending 31.03.2008 is Rs. 860.31 crore.

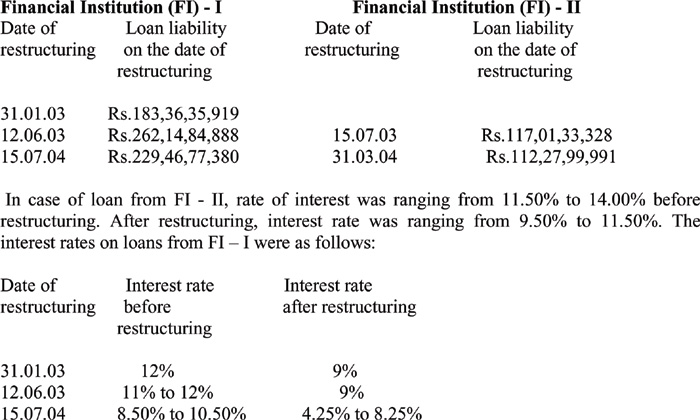

2. With a view to take the benefit of reduction of interest rates in general, the company has undergone restructuring of loans availed from financial institutions for financing of capital assets. The querist has informed that the purpose of restructuring of loan was to convert high interest cost bearing loan into low interest cost bearing loan. At the time of restructuring, the construction of the assets was already complete and the assets were in use. The details of the restructuring scheme have been provided by the querist as follows:

3. The querist has further stated that the company, as per its accounting policy, treats the premium paid for restructuring the loan availed from financial institutions for reduction in interest rates as deferred revenue expenditure and the same is written off over the balance tenure of loan.

4. The querist has stated that in case any loan is repaid in full in a year, prepayment charges paid are written off in the year of repayment itself. Through a separate letter, the querist has, however, informed that the prepayment charges are treated as deferred revenue expenditure.

B. Query

5. The querist has sought the opinion of the Expert Advisory Committee as to whether the accounting policy adopted by the company is in compliance with the existing Accounting Standards and the generally accepted accounting principles. If not, the querist has sought advice with respect to the modifications required.

C. Points considered by the Committee

6. The Committee, while answering the query, has considered only the issues raised in paragraph 5 above and has not touched upon any other issue that may arise from the Facts of the Case.

7. The Committee notes that paragraph 3.1 of Accounting Standard (AS) 16, ‘Borrowing Costs’, notified under the Companies (Accounting Standards) Rules, 2006, provides that “Borrowing costs are interest and other costs incurred by an enterprise in connection with the borrowing of funds.” Further, the Standard contemplates “amortisation of discounts or premiums relating to borrowings” as a component of borrowing costs (paragraph 4(b) of AS 16). Thus, the borrowing costs comprise the amount of premium amortised during the period. The Committee notes from the above that since the restructuring premium in the present case is incurred in connection with the borrowings of the company, it is a borrowing cost as per the provisions of AS 16. The Committee also notes that although as per AS 16, borrowing costs include amortisation of discounts or premiums relating to borrowings, it does not prescribe amortisation of such costs.

8. Now, the question arises as to how such premium should be recognised in the financial statements of the company. In this regard, the Committee notes that as per the Framework for the Preparation and Presentation of Financial Statements, issued by the Institute of Chartered Accountants of India, in case an expenditure meets the definition of the term ‘asset’ and the recognition criteria thereof, the same should be recognised as an asset; failing which, the expenditure should be expensed in the profit and loss account in the year in which the expenditure is incurred. The Committee notes that the term ‘asset’ has been defined in the Framework as follows:

“An asset is a resource controlled by the enterprise as a result of past events from which future economic benefits are expected to flow to the enterprise.” (Paragraph 49(a))

9. On the basis of the above, the Committee is of the view that the premium paid towards restructuring of a loan meets the definition of an asset since it is paid in consideration of paying lesser interest in future and, therefore, is a resource controlled by the entity having future economic benefits. In substance, it can be considered as an advance payment of interest whose benefit will be realised over the tenure of the loan. The Committee is, therefore, of the view that following the principle of ‘accrual’, viz., “revenues and costs are accrued, that is, recognised as they are earned or incurred (and not as money is received or paid) and recorded in the financial statements of the periods to which they relate” (paragraph 10(c) of Accounting Standard (AS) 1, ‘Disclosure of Accounting Policies’), since the premium paid for restructuring of the loan is related to and incurred for the purpose of reduction in the interest over the balance tenure of the loan, the asset, i.e., the premium paid should be amortised over the balance tenure of the loan on straight line basis or by using effective interest rate method. The periodic amortisation of the premium should be recognised in the profit and loss account of the relevant period as the construction of the assets is already complete.

10. Insofar as the pre-payment charges for the loan are concerned, the Committee notes that the querist has given contradictory statements in paragraph 4 above with respect to the accounting treatment followed by the company. The Committee is of the view that in order to determine the accounting treatment, the substance of the transaction should be seen. In substance, if the prepayment of loan is extinguishment of the existing liability, to the extent these charges are incurred towards extinguishment of the existing loan liability, the same should be expensed in the statement of profit and loss as these charges would not have any future economic benefit. However, in case, in substance, the prepayment of loan is not extinguishment of the existing liability, it should be considered as restructuring of the liability and accordingly, the treatment prescribed in the above paragraphs should be followed.

D. Opinion

11. On the basis of the above, the Committee is of the opinion that the accounting policy of the company treating the premium paid on restructuring and prepayment charges as deferred revenue expenditure, is not in compliance with the existing generally accepted accounting principles. The premium paid for restructuring should be amortised over the balance tenure of the loan on straight line basis or by using effective interest rate method, as discussed in paragraph 9 above. In respect of the prepayment charges, the Committee is of the opinion that if prepayment of the loan is, in substance, extinguishment of the existing loan liability, the same should be expensed in the statement of profit and loss. However, in case, in substance, the prepayment of loan is not extinguishment of the existing liability, it should be considered as restructuring of the liability and accordingly, the treatment prescribed for premium paid on restructuring should be followed, as discussed in paragraph 10 above. The accounting policy should be modified accordingly.

1Opinion finalised by the Committee on 15.12.2009

|