|

Query No. 27

Subject:

Virtual certainty for the purpose of recognition of deferred tax assets.1

A. Facts of the Case

1. A company is a subsidiary of a foreign company, which through its subsidiaries, owns 75% of the company’s share capital. The company primarily deals with consumer durables white goods, such as, refrigerators, washing machines, air conditioners, microwave ovens, etc. The company also exports home appliances to various parts of the world.

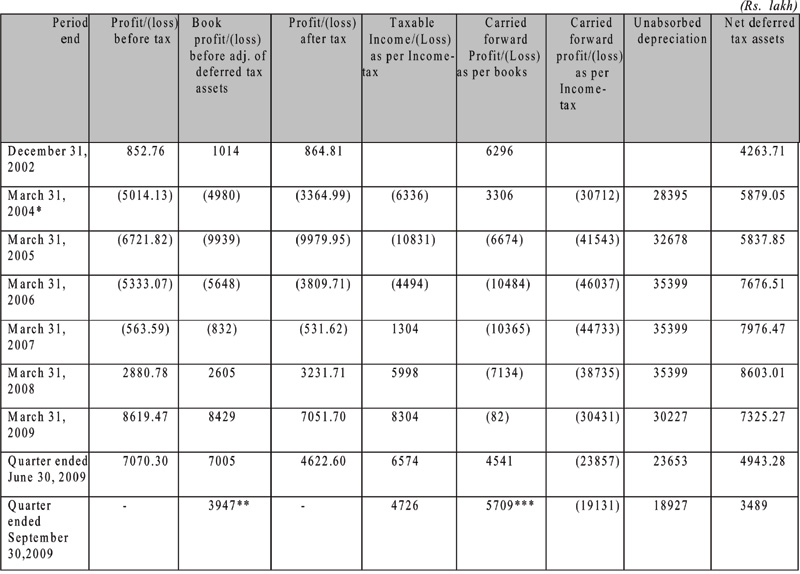

2. The querist has stated that the company had recognised deferred tax asset in the year 2001 as per the requirements of Accounting Standard (AS) 22 , ‘Accounting for Taxes on Income’, which became mandatorily applicable to the company in that year. Since then the company has been reviewing the carrying amount of deferred tax assets based on reversal/occurrence of timing differences over years. The gross deferred tax assets as recognised by the company primarily represent carried forward losses and unabsorbed depreciation which are available for set off in future years for tax purposes. The querist has provided a summary of profits earned, accumulated balance of profit and loss account, net deferred tax assets in company’s books over the past years, etc., as follows:

* The year-end was shifted to March.

**After considering MAT Surcharge and Cess of Rs. 346 lakh.

***After appropriation of dividend on preference capital of Rs. 1130 lakh and tax thereon of Rs. 192 lakh.

According to the querist, it is apparent from the above that the company earned profits in the year 2002 and was in losses in the subsequent four years. Due to external market environment, the company suffered losses in the past that resulted into negative accumulated profit and loss balance as shown above. The above mentioned accumulated balance of profit and loss account is after considering the impact of recognition of deferred tax assets on carried forward losses and unabsorbed depreciation.

3. The querist has further stated that the company has recognised the deferred tax assets on the basis of past profitability trends and is confident that subsequent realisation of the deferred tax assets as created is virtually certain in the near future based on existing business model of the company and the same has also been disclosed in detail in the notes to accounts to the financial statements of respective years.

4. According to the querist, the auditors of the company have been, since the year 2004, qualifying their opinion in respect of recognition of deferred tax assets as they are of the opinion that the basis as considered by the company for recognition of deferred tax assets to determine virtual certainty is not in line with the requirements of AS 22 and Accounting Standards Interpretation (ASI) 9 2 , ‘Virtual certainty supported by convincing evidence’, issued by the Institute of Chartered Accountants of India. The querist has reproduced ASI 9 as below:

“ISSUE

1. Paragraph 17 of AS 22 requires that “Where an enterprise has unabsorbed depreciation or carry forward of losses under tax laws, deferred tax assets should be recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised”.

2. The issue is what amounts to ‘virtual certainty supported by convincing evidence’ for the purpose of paragraph 17 of AS 22.

CONSENSUS

3. Determination of virtual certainty that sufficient future taxable income will be available is a matter of judgement and will have to be evaluated on a case to case basis. Virtual certainty refers to the extent of certainty, which, for all practical purposes, can be considered certain. Virtual certainty cannot be based merely on forecasts of performance such as business plans.

4. Virtual certainty is not a matter of perception and it should be supported by convincing evidence. Evidence is a matter of fact. To be convincing, the evidence should be available at the reporting date in a concrete form, for example, a profitable binding export order, cancellation of which will result in payment of heavy damages by the defaulting party. On the other hand, a projection of the future profits made by an enterprise based on the future capital expenditures or future restructuring etc., submitted even to an outside agency, e.g., to a credit agency for obtaining loans and accepted by that agency cannot, in isolation, be considered as convincing evidence.

BASIS FOR CONCLUSIONS

5. In a situation where an enterprise does not have unabsorbed depreciation or carry forward of losses, the degree of certainty required under AS 22 for recognition of deferred tax asset is ‘reasonable certainty’. In contrast, as a measure of greater prudence, AS 22 prescribes a much higher level of certainty, i.e., virtual certainty, for recognition of deferred tax asset in a situation where an enterprise has unabsorbed depreciation or carry forward of losses. Therefore, the level of certainty required for recognition of deferred tax asset in a situation where an enterprise has unabsorbed depreciation or carry forward of losses is much more than the situation where the enterprise does not have the same.

6. Projections on the basis of future actions of an enterprise cannot be considered as convincing evidence since the enterprise may change its plans on the basis of subsequent developments.”

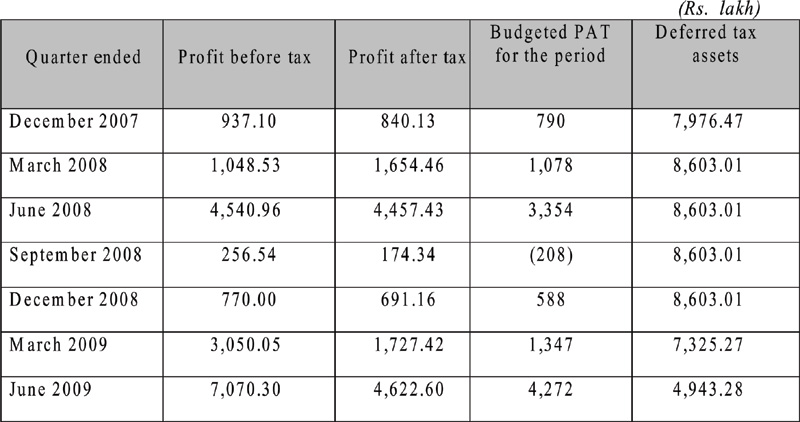

5. As per the querist, the company has started earning profits from the year 2007 and has been consistently earning profits since last seven quarters. Moreover, the profit expectation as set out by the company in its annual budgets has also been exceeded/achieved. The querist has provided the details of profits earned and budgeted profits of the company in the said period as follows:

The querist has stated that as evident from the above profit trend, corresponding reversal of deferred tax assets during the above period, and keeping in view future profit projections, the management of the company feels that there is sufficient convincing evidence that recognised deferred tax asset would be realised in future years.

6. The querist has also stated that strict interpretation of ASI 9 suggests that convincing evidence can only be supported by firm sales orders or profits earned in subsequent period, whereas, in case of consumer goods industries, like in the case of the company, the concept of firm sales order does not exist. Thus, in the view of the querist, presence of convincing evidence should be inferred from facts like:

(a) Current product pricing and profitability trends;

(b) Company’s market share; and

(c) Growth forecast based on Gross Domestic Product (GDP) estimates.

Moreover, according to the querist, the company’s performance over the past years and market share along with industry growth should also be considered. ASI 9 enumerates availability of order books as a convincing evidence to establish virtual certainty. As the order book is available only in certain industries, the intent of ASI 9 would not have been to restrict industries, like consumer goods industries, retail industries, service industries, automobiles and ancilliaries, etc., which are primarily not operating on long order books. Thus, as per the querist, for such industries, factors, as discussed above, should be considered to establish whether convincing evidence exists or not. Availability of an order book is one of the examples and not the sole criterion to be considered as convincing evidence to establish virtual certainty under ASI 9. Paragraph 3 of ASI 9 states that determination of virtual certainty that sufficient future taxable income will be available is a matter of judgement and will have to be evaluated on a case to case basis. The company has shown consistent performance in the last two years as discussed above and this trend should also be considered as a convincing evidence to establish that it is virtually certain that the company will have sufficient future taxable income to realise its deferred tax assets.

7. The querist has stated that the past trend indicates that deferred tax assets as created, will be realised within the next 12-18 months. Accordingly, in the view of the querist, virtual certainty should be based on exploration of the most recent profit trends which have been consistent with a robust growth record and not merely on forecasts of performance, such as, business plans. The querist has also submitted that all the accumulated book losses have already been liquidated and the company has positive carried forward profit in the books of account as on 30th June, 2009.

B. Query

8. The querist has sought the opinion of the Expert Advisory Committee on the following issues:

(i) Where it appears to be evident that the balance of the already recognised deferred tax assets will get realised in the next 12-18 months and as this period falls within the ambit of short term, whether such realisation can be considered as virtually certain and recognition of deferred tax assets by the company on this basis as justified.

(ii) Whether in the case of the company, the auditor’s report needs to be qualified on recognition of deferred tax assets and whether such a qualification is also required to be considered to compute the distributable profits of the company as per section 205 of the Companies Act, 1956. The company has issued 10% cumulative redeemable preference shares in earlier years and dividend payable as on 31st March, 2009 on the same is Rs. 5,700 lakh. Since the company had a distributable profit before considering the impact of the above mentioned qualification till the quarter ended 30th June, 2009, whether the company can declare interim dividend in the year 2009-10 to pay part of accumulated dividend on preference shares.

C. Points considered by the Committee

9. The Committee, while answering the query, has considered only the issues raised in paragraph 8 above and has not examined any other issue that may arise from the Facts of the Case. The issue raised in paragraph 8(ii) above regarding computation of distributable profits and declarlation of interim dividend as per the requirements of the Companies Act, 1956 is a legal interpretation of the Companies Act, 1956, which the Committee is prohibited from answering as per Rule 2 of its Advisory Service Rules. Accordingly, the Committee refrains from answering the same.

10. The Committee notes paragraphs 17 and 18 of Accounting Standard (AS) 22, ‘Accounting for Taxes on Income’, which are reproduced below:

“17. Where an enterprise has unabsorbed depreciation or carry forward of losses under tax laws, deferred tax assets should be recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised.

18. The existence of unabsorbed depreciation or carry forward of losses under tax laws is strong evidence that future taxable income may not be available. Therefore, when an enterprise has a history of recent losses, the enterprise recognises deferred tax assets only to the extent that it has timing differences the reversal of which will result in sufficient income or there is other convincing evidence that sufficient taxable income will be available against which such deferred tax assets can be realised. In such circumstances, the nature of the evidence supporting its recognition is disclosed.”

11. The Committee further notes that the consensus portion of ASI 9 issued by the Institute of Chartered Accountants of India reproduced in paragraph 4 above has subsequently been incorporated as ‘Explanation 1’ to paragraph 17 of AS 22 notified under the Companies (Accounting Standards) Rules, 2006. The Committee notes that it, inter alia, provides that “virtual certainty refers to the extent of certainty, which, for all practical purposes, can be considered certain” (emphasis supplied by the Committee). The Committee also notes that the ‘Basis for Conclusions’ contained in ASI 9, makes a distinction between ‘reasonable certainty’ and ‘virtual certainty’. It states that in a situation where unabsorbed depreciation and carried forward losses exist, it is the ‘virtual certainty’ which is required for recognition of deferred tax asset. The Committee is of the view that factors, such as, company’s market share, growth forecast based on GDP system indicating the earning of profit, and the confidence of the company that subsequent realisation of the deferred tax assets is virtually certain in near future, as mentioned by the querist to be convincing evidence, are only factors that may be taken into consideration for future projections. These may, at best, indicate a ‘reasonable certainty’ of future profitability. However, in the present situation of unabsorbed depreciation or carry forward of losses, as per paragraph 17 of AS 22, the Standard requires ‘virtual certainty’ supported by ‘convincing evidence’. In the view of the Committee, the factors as stated above by the querist, cannot be considered as convincing evidence of virtual certainty as contemplated in the Explanation to paragraph 17 of AS 22 (erstwhile ASI 9).

12. The Committee also notes that in the absence of any confirmed sales orders as on the date of the balance sheet, the company has not forwarded any support in favour of any existing convincing evidence that sufficient future taxable income will be available. The Committee is of the view that in the case of the company, even though it is engaged in the sale of consumer durables, it is possible to have confirmed sales orders on the date of the balance sheet in the form of domestic orders from dealers or export orders. The Committee, however, wishes to point out that deferred tax assets can be created in respect of unabsorbed depreciation and brought forward losses to the extent that future taxable income will be available from future reversal of any deferred tax liabilities recognised at the balance sheet date. To that extent, it would not be necessary to consider virtual certainty supported by convincing evidence.

D. Opinion

13. On the basis of the above, the Committee is of the following opinion on the issues raised in paragraph 8 above:

(i) The company is not justified in recognising deferred tax assets on unabsorbed depreciation and brought forward losses as per tax laws in its accounts merely on the basis of financial future projections and its confidence of availability of taxable income. However, to the extent of the availability of future taxable income, if any, by virtue of the future reversal of any deferred tax liability recognised at the balance sheet date, the deferred tax assets can be recognised. Please refer to paragraphs 11 and 12 above.

(ii) In the case of the company, the auditor’s report needs to be qualifed as the company is not justified in recognising deferred tax assets. As stated in paragraph 9 above, the issue relating to computation of distributable profits and declaration of interim dividend as per the requirements of the Companies Act, 1956, is not answered in accordance with Rule 2 of the Advisory Service Rules of the Committee.

1Opinion finalised by the Committee on 15.12.2009

2 The ASI has been withdrawn by the Council of the Institute of Chartered Accountants of India and the Consensus portion thereof has been added as ‘Explanation 1’ to the paragraph 17 of AS 22.

|