|

Query No. 32.

Subject:

Provision for disputed interest liability on term loan. 1

A. Facts of the Case

1. An unlimited liability company ‘D’ was promoted by entities ‘E’, ‘G’ and ‘B’ along with ‘X’ State Power Development Corporation Limited in early 1990s to set up an integrated power plant in two phases (Phase I : Block 1; and Phase II : Blocks 2 & 3 along with an integrated 5 MMTPA Liquified Natural Gas (LNG) terminal in the State. The project was planned based on Reliquified Natural Gas (RLNG) as primary fuel and Naphtha / HSD as secondary fuel. Phase I of the project commenced operations on Naphtha in May 1999 and thereafter the operations were suspended in May 2001 due to disputes between company ‘D’ and ‘X State Electricity Board’ (XSEB) arising out of

(a) operational compliances,

(b) lesser build-up in power demand and resulting default by XSEB in power purchase, and

(c) higher fuel cost as well as higher fixed cost.

2. This dispute led to stoppage of operation of Phase I of the plant and suspension of erection and commissioning activities of Phase II. In respect of Phase II of the project, Block 2 was under commissioning stage and few erection works and commissioning of Block 3 were pending. Substantial work was also pending at the LNG Receiving Terminal and marine facilities when all the construction activities of the project were stalled in May 2001.

3. The querist has stated that the Government of India (Union Cabinet), in its meeting held on 2nd November, 2004, constituted an Empowered Group of Ministers (EGoM) to revive the project while addressing all issues pertaining to company ‘D’. To finalise a viable restructuring plan for the project, EGoM proposed the following:

- Indian Financial Institutions (IFIs) to negotiate and buy-out debt of offshore stakeholders, i.e., foreign banks, Overseas Private Investment Corporation (OPIC) and Export Credit Agencies (ECAs).

- Government guaranteed bonds to be issued by a Financial Special Purpose Vehicle (FSPV) to be promoted by IFIs for the purpose of buying out the above-mentioned debts.

- Negotiations and settlements to buy-out non-debt claims and equity of entities ‘G’, ‘B’ and overseas private investment corporation by the IFIs.

- Project assets of company ‘D’ proposed to be transferred to a new Project SPV (PSPV) on sale/ auction basis through Debt Recovery Tribunal (DRT) process. The Project SPV would be capitalised by way of equity / advance bid-security from two companies, A and B. In addition, Indian lenders would also infuse fresh equity which would enable settlement of non-debt claims and help restart/ complete the project. Promoted by the two companies A and B, company ‘R’ was incorporated on 8th July, 2005 to undertake the construction and completion of the project and to manage the project facilities. Following the out of court settlement between company ‘D’ and XSEB, the assets of company ‘D’ were transferred to company ‘R’ at a price of Rs. 8,485 crore in October 2005 through the Debt Recovery Tribunal (DRT) process on sale basis.

- PSPV to undertake construction and completion of the project and operate and manage the project facilities.

- XSEB to offtake power from the project on a long-term take-or-pay basis at a plant load factor (PLF) of 80%.

- Indian lenders’ debt to be assumed by the Project SPV on restructured terms.

4. Based on the scheme, as mentioned above, the dispute between company ‘D’ and XSEB was resolved following an out of court settlement, and ‘consent terms’ in this regard were filed in the Supreme Court on putting a stop to all legal proceedings in India and abroad in respect of this dispute.

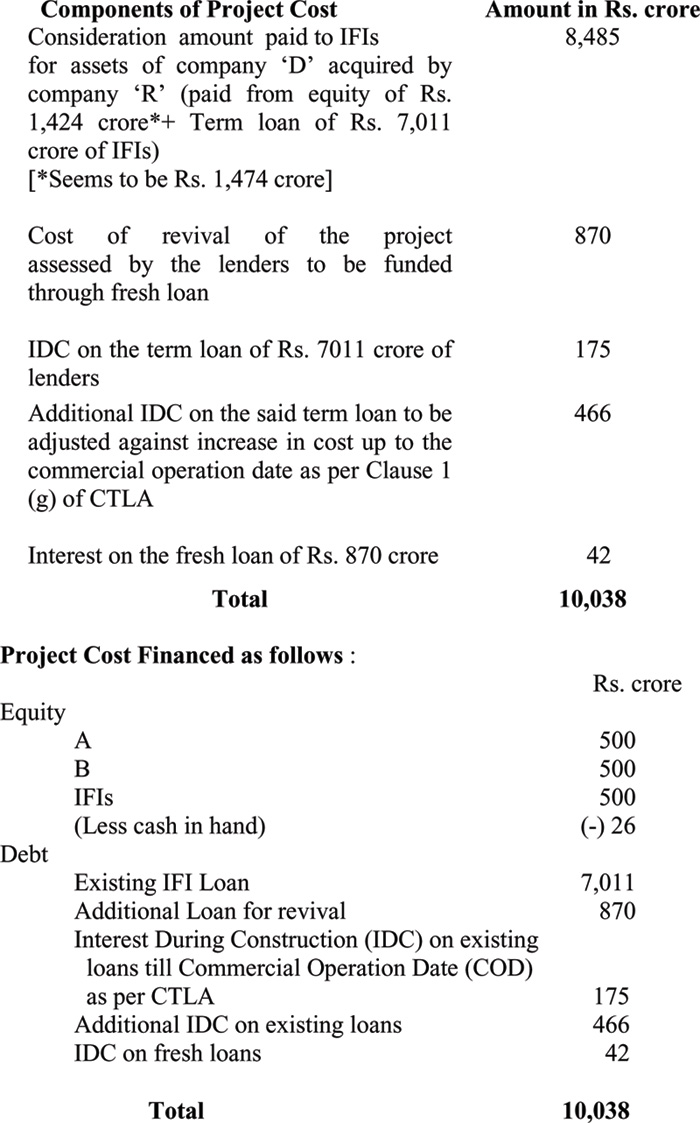

5. The Board of company ‘R’ approved on 15th September, 2005, an investment of Rs. 10,038 crore for acquiring the existing assets of the project at Rs. 8,485 crore and additional investment of Rs. 1,553 crore for completion of balance works, for project revival, including interest during construction (IDC) of Rs. 683 crore. Company ‘R’ also executed the Common Term Loan.

Agreement (CTLA) with the existing lenders on 28.09.2005 for Rs. 7,011.85 crore. The details of the project cost and its financing are stated by the querist to be as follows:

6. To assess the revival cost of the project, ‘T’ was hired as consultant by lenders. Based on T’s assessment, at the point of execution of the CTLA, the total cost of revival was estimated at Rs. 870 crore, which consisted of Rs. 214 crore for power block and Rs. 656 crore for LNG block. T’s estimates, as per the querist, were based on walk-down visual survey and not on detailed inspection.

7. R-LNG was expected to be made available from June 2006 and all the power blocks were expected to be operational by November 2006. At the time of execution of CTLA itself, there was a dispute on revival cost as assessed by lenders’ consultants and as assessed by companies A and B (promoters). As against the lenders’ consultants estimated cost of revival Rs. 870 crore, companies A and B were of the view that revival cost of the project would be around Rs. 2,000 crore. Due to this, some clauses were added in the agreement to cap the revival cost at Rs. 870 crore and any increase in the said revival cost was to be adjusted from additional IDC.

8. The relevant provisions of the CTLA relating to IDC, additional IDC, COD and completion cost are given hereunder:

- Clause 1(A)(c) – Additional IDC means the interest, until the Block Commercial Operation Date of third block of the power plant, in addition to the IDC.

- Clause 1(A)(g) - Block Commercial Operation Date shall mean

- in relation to the first block of the power plant, 1st September, 2006,

- in relation to the second block of the power plant, 1st October, 2006; and

- in relation to the third block of the power plant, 1st November, 2006

or such other later date in relation to (i), (ii) or (iii) as may be determined by mutual agreement between the borrower and the lenders.

- Clause 1(A)(m) – Commercial Operation Date shall mean the Block Commercial Operation Date for the third block of the power plant as declared by the borrower after demonstrating the Maximum Continuous Rating or Installed Capacity (each as defined or construed in accordance with the PPA) through a successful trial run after notice to the Offtaker, in relation to the third block of the power plant.

- Clause 1(A)(o) – Completion Cost means the aggregate of amounts payable (excluding any Interest During Construction) by the borrower for the completion of the Project.

- Clause 1(A)(s) Construction Period means the time period commencing from the date of first disbursement till the Commercial Operation Date.

- Clause 1(A)(jj) – IDC means the interest until the Block Commercial Operation Date of the third block of the power plant aggregating to amounts not less than Rs.175 crore collectively for all the lenders and individually with respect to each lender (detail provided).

- Clause 1(A)(ll) – Interest During Construction means the aggregate of the following incurred during the construction period:

- IDC;

- Additional IDC; and

- Fees, interest, costs and commissions payable by the borrower to its financiers or its credit enhancers in relation with the finance availed by the borrower.

- Clause 1(A)(iii) Project means the development, construction, commissioning, operation and maintenance of 2150 MW (net capacity) gas based power plant and a 5.0 million tones per annum (MTPA) LNG Terminal at Guhaghar, Ratnagiri district in the State.

- Clause 1(A)(jjj) Project Cost means the amounts expended for the acquisition, construction and completion of the Project (including interest during construction) to the extent of Rs. 10,038 crore.

- Clause 6(a) provides – Save and except as mentioned below, interest at the Interest Rate shall be payable on the Loans:

IDC shall be payable by the borrower to the lenders on the Interest Payment Dates. Without prejudice to the foregoing, on the Interest Payment Date immediately following the Commercial Operation Date, Additional IDC, if any, shall be payable by the borrower to the lenders (other than one of the lenders), which amounts shall be determined as follows:

if the Completion Cost is Rs. 870 crore, the additional IDC shall be Rs. 466 crore; and if the Completion Cost increases from Rs. 870 crore, the amounts constituting the Additional IDC payable by the borrower shall be decreased by such increase in amount.

The querist has stated that the amount of additional IDC of Rs. 466 crore mentioned in the agreement has been calculated on the assumption of commercial operation dates as per clause 1(A)(g) of the agreement, as quoted above. As commercial operation dates of all the blocks have changed, the calculation of additional IDC needs to be revised on the basis of actual commercial operation dates. (Emphasis supplied by the querist.)

- Clause 6(b) provides – The Loans shall carry the following rate of interest (“Interest Rate”):

- On and from the date falling (i) eleven (11) calendar months; (ii) twelve (12) calendar months; and (iii) thirteen (13) calendar months respectively, from (A) the date of first disbursement of Loan or (B) upon the Borrower receiving possession of the Project Assets as per the Consent Terms, whichever is later, notwithstanding anything, the Block Proportionate Loans (other than the Loan from one of the lenders) relevant to each block of the power plant shall carry a rate of interest of 9% p.a. with monthly rests.

- The Part A Loan from one of the lenders shall carry a rate of interest of 8.5% p.a. with monthly rest.

- The Part B Loan from one of the lenders shall carry a rate of interest of 9.76% p.a. payable annually.

- Clause 7 provides –

- The borrower shall pay to each lender, interest on the Loan of that lender for the Interest Period at the Interest Rate plus interest tax and other statutory levies as applicable from the date of disbursement of each tranche of such Loan. The borrower shall pay the lenders, accrued (and theretofore unpaid) interest on the loan on the Interest Payment Dates. The first Interest Payment Date in relation to the Part B Loan from one of the lenders shall be April 1, 2008.

- All interest payable pursuant to this Agreement shall accrue from day to day and shall be calculated on the basis of a year of 365 days.

- The borrower acknowledges that the Facility provided under this Agreement is for a commercial transaction and waives any defenses available under usury or other laws relating to the charging of interest and other monies payable hereunder.

- Clause 23 of CTLA states –

- As a result of increase in Completion Cost, if the Project Cost exceeds Rs. 10,038 crore, the lenders shall take suitable financial structuring to ensure that Project Cost does not exceed Rs. 10,038 crore.

- In case the Completion Cost increases by more than 10% of Rs. 870 crore, it is agreed between the parties that Central Electricity Authority (for the power plant) and the Lenders LNG Engineer (for the LNG facilities) shall be engaged for reviewing the cost for completion. The borrower shall accept the recommendations, if any, pursuant to such review, made by the Central Electricity Authority (for the power plant) and the Lenders LNG Engineer (for the LNG facilities). The Lenders LNG Engineer and the Central Electricity Authority shall be appointed at the expense of the borrower for the aforesaid purpose.

- Clause 28(ii) of the CTLA states – Each lender shall have the right to set off against amounts payable by the borrower to the Secured Parties under the Financing Documents.

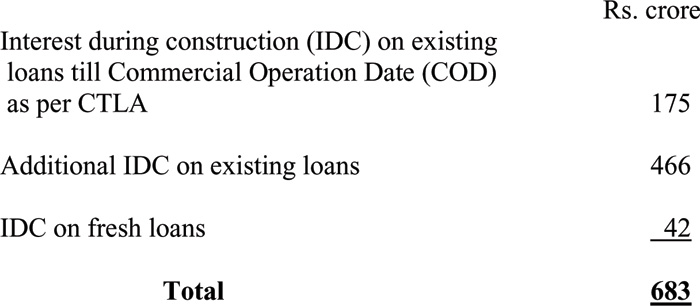

9. As stated in paragraph 5 above, the interest during construction was provided in the CTLA, as follows:

10. As per present assessment, the revival cost of the project has been estimated at Rs. 2,364 crore instead of Rs. 870 crore assumed in the CTLA. Commercial operation dates (CODs) of power blocks have also been revised as follows :

As per CTLA Revised as

First Power Block 1st Sept., 2006 1st Sept., 2007

Second Power Block 1st Oct., 2006 21st Nov., 2007

Third Power Block 1st Nov., 2006 yet to be declared

11. As per clause 1(A)(c) of the CTLA, Additional IDC means the interest, until the Block Commercial Operation Date of the third block of power plant, in addition to the IDC. Further, clause 6(a) of CTLA, inter alia, provides that “if the Completion Cost is Rs. 870 crore the additional IDC shall be Rs. 466 crore; and if the Completion Cost increases from Rs. 870 crore, the amounts constituting the Additional IDC payable by the Borrower shall be decreased by such increase in amount.” The querist has stated that the amount of additional IDC of Rs. 466 crore mentioned in CTLA has been calculated on the assumption of commercial operation dates of September, October and November 2006. The CTLA provides that actual commercial operation date would be mutually agreed by lenders and borrower. As commercial operation dates of all the blocks have changed, the calculation of additional IDC needs to be revised on the basis of actual commercial operation dates. (Emphasis supplied by the querist.) As per the above clause, increase in completion cost has to be adjusted from additional IDC in terms of CTLA. Additional IDC has to be revised in view of revised commercial operation dates.

12. As mentioned in paragraph 3 above, EGoM is reviewing the revival of the project. In terms of clause 23 of CTLA, as stated above, it is provided that as a result of increase in completion cost, if the project cost exceeds Rs. 10,038 crore, the lenders shall take suitable financial structuring to ensure that project cost does not exceed Rs. 10,038 crore. This matter has also been deliberated in EGoM and other meetings at various levels in the Government wherein representatives of promoters and lenders participated.

13. According to the querist, in view of the increase in the revival cost and change in commercial operation dates, the lenders are required to revise the amount of additional IDC and complete the suitable financial structuring to ensure that project cost does not exceed Rs. 10,038 crore as per CTLA. Company ‘R’ is of the view that in terms of the CTLA, increase in revival cost is to be reduced from revised additional IDC as per CTLA. As the increase in revival cost is more than the additional IDC, no additional amount of IDC is payable to the lenders. Thus, it is observed by the querist, that till the above activity and financial restructuring is complete, IDC beyond Rs. 175 crore is not due and thus, not provided for in the books of account.

14. Lenders are, however, of the view that the rate of interest applicable to the loans and the manner in which it would accrue and be payable, during the originally envisaged implementation period and thereafter, is firmly set out in clauses 6(a), 6(b)(i) and 7 of the CTLA, and that company ‘R’ needs to provide for interest on the loans, post the originally envisaged commercial operation dates, in its books of account, on the basis of the contractual arrangement prevailing at this juncture between the company and the lenders. Lenders are of the view that unless the interest liability, which is known, firm and can be quantified, is provided for in the books of account, the financial statements of the company would not be deemed to present a true and fair view of the state of affairs of the company, as per the provisions of the Companies Act, 1956 and the relevant Accounting Standards. It has been further observed by the lenders that various options for restructuring to maintain long-term viability of the project are being discussed under the aegis of the Government of India and a final view is yet to emerge in the matter and not charging interest on the loans, post the originally envisaged commercial operation date, is not an option that is under consideration/ discussion. Hence, not providing for interest in the books of account on the assumption that loan/interest would be waived is neither correct nor appropriate.

15. As per the querist, the same view, as mentioned in paragraph 14 above, was taken by the lenders at the time of finalisation of annual accounts of the company for the year ended 31st March, 2007. During the course of review of the annual accounts by the C&AG, on a reference from C&AG, lenders’ views were informed vide letter dated 4th February, 2008. As required by C&AG vide its letter dated 6th February, 2008, company ‘R’ submitted its reply vide letter dated 8th February, 2008 to the C&AG, reiterating that, in terms of the applicable Accounting Standards, the company has not provided any interest liability beyond the originally envisaged commercial operation date of 30th September, 2006, till the matter of financial restructuring is under consideration of the Government of India. This was accepted by the C&AG.

16. Thus, company ‘R’ is of the view that the annual accounts of the company have been drawn up in accordance with the provisions of the Companies Act, 1956 and the applicable Accounting Standards. The annual accounts of company ‘R’ for the year ended 31st March, 2007 were duly audited by a firm of Chartered Accountants appointed by the C&AG, and the same position was also accepted by the C&AG during the course of review of the annual accounts for the same period. There is no change in the position in respect of drawl of annual accounts for the year ended 31st March, 2008. It may be pertinent to mention that necessary disclosure in the annual accounts in the notes to accounts has been made, as stated below :

Note No. 1 : The company took over the project of erstwhile …(name of company ‘D’) as per the decree of the Court. Pending completion of revival works of Power Blocks and LNG facilities as a whole, provisional completion cost of the project as approved by Empowered Group of Ministers (EGoM)/ Government of India (GoI) was Rs. 100,380 million + Rs. 2,650 million on account of XSEB’s equity for consideration other than cash. Further, as per Common Term Loan Agreement (CTLA) dated 28th September, 2005 between the lenders and the company, the lenders have given the commitment that, “as a result of increase in completion cost, if the project cost exceeds Rs. 100,380 million, the lenders shall take suitable financial structuring to ensure that the project cost does not exceed Rs. 100,380 million”. The revival cost of Rs. 8,700 million, estimated at the time of take over of assets, has now been estimated Rs. 23,640 million (without IDC) and in view of this increase, financial restructuring of the project is under consideration of lenders/GoI.

Note No. 2 : In terms of the CTLA with banks and financial institutions, loans aggregating Rs. 70,119 million were given to the company, and the commercial operation dates of power blocks I, II & III were scheduled on 1st September 2006, 1st October 2006 and 1st November 2006 respectively. In line with these commercial operation dates, interest during construction (IDC) on the loan of Rs. 70,119 million was quantified at Rs. 1,750 million. In addition, additional IDC was quantified at Rs. 4,660 million with the provision in CTLA that, “if the completion cost is Rs. 8,700 million the additional IDC shall be Rs. 4,660 million and if the completion cost increases from Rs. 8,700 million, the amount constituting the additional IDC payable by the borrower shall be decreased by such increase in amount”.

Considering the current estimated completion cost of Rs. 23,640 million (without IDC) and financial restructuring of the project being under consideration of the lenders/GoI, company’s liability of interest on the loans of Rs. 70,119 million, beyond Rs. 1,750 million, which was the agreed IDC, has not been recognised as contingent or firm liability by the company and has, therefore, not been provided for in the accounts. The amount not so recognised is estimated at Rs. 8,420 million.

B. Query

17. The querist has sought the opinion of the Expert Advisory Committee as to whether the annual accounts of the company which have been drawn, as stated above, have been drawn in accordance with the provisions of the Companies Act, 1956 and the applicable Accounting Standards on the subject.

C. Points considered by the Committee

18. The Committee notes that the basic issue raised by the querist relates to appropriateness of non-provision of interest beyond the originally scheduled (block) commercial operation date. Therefore, the Committee has examined only this issue and has not examined any other issue that may be contained in the Facts of the Case.

19. From the Facts of the Case, the Committee notes that there is a dispute between the company and its lenders on the need for making provision in the financial statements for interest on term loan beyond the originally scheduled (Block) commercial operation date. The Committee also notes that the C&AG agreed with the contention of the company in not making the provision.

20. At the outset, the Committee wishes to point out that the Committee refrains from interpreting the terms of the Common Term Loan Agreement (‘CTLA’) since that is beyond the scope of the Committee’s advisory role. Similarly, the Committee refrains from expressing any view involving legal implications, such as, the consequences of CTLA not foreseeing and providing a remedy to the shifting of Block Commercial Operation Date.

21. The Committee notes that paragraph 46 of the ‘Framework for the Preparation and Presentation of Financial Statements’, issued by the Institute of Chartered Accountants of India, inter alia, states that the application of appropriate accounting standards normally results in financial statements that convey what is generally understood as a true and fair view of the financial position, performance and cash flows of an enterprise.

22. As per paragraph 10 of Accounting Standard (AS) 1, ‘Disclosure of Accounting Policies’, issued by the Institute of Chartered Accountants of India as well as notified under the Companies (Accounting Standards) Rules, 2006, (hereinafter referred to as the ‘Rules’), ‘accrual’ is one of the fundamental accounting assumptions. As per the accrual concept, revenues and costs are accrued, that is, recognised as they are earned or incurred (and not as money is received or paid) and recorded in the financial statements of the periods to which they relate. The Committee notes that there is a dispute between the company and its lenders as to whether interest after the originally scheduled commercial operation date accrues or not till the financial restructuring is over.

23. The Committee notes the following paragraphs from Accounting Standard (AS) 29, ‘Provisions, Contingent Liabilities and Contingent Assets’, issued by the Institute of Chartered Accountants of India as well as notified under the ‘Rules’:

“10.1 A provision is a liability which can be measured only by using a substantial degree of estimation.

10.2 A liability is a present obligation of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.

10.3 An obligating event is an event that creates an obligation that results in an enterprise having no realistic alternative to settling that obligation.

10.4 A contingent liability is:

(a) a possible obligation that arises from past events and the existence of which will be confirmed only by the occurrence or non occurrence of one or more uncertain future events not wholly within the control of the enterprise; or

(b) a present obligation that arises from past events but is not recognised because:

(i) it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or

(ii) a reliable estimate of the amount of the obligation cannot be made.”

“10.6 Present obligation - an obligation is a present obligation if, based on the evidence available, its existence at the balance sheet date is considered probable, i.e., more likely than not.

10.7 Possible obligation - an obligation is a possible obligation if, based on the evidence available, its existence at the balance sheet date is considered not probable.”

“14. A provision should be recognised when:

(a) an enterprise has a present obligation as a result of a past event;

(b) it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation; and

(c) a reliable estimate can be made of the amount of the obligation.

If these conditions are not met, no provision should be recognised.

15. In almost all cases it will be clear whether a past event has given rise to a present obligation. In rare cases, for example in a lawsuit, it may be disputed either whether certain events have occurred or whether those events result in a present obligation. In such a case, an enterprise determines whether a present obligation exists at the balance sheet date by taking account of all available evidence, including, for example, the opinion of experts. The evidence considered includes any additional evidence provided by events after the balance sheet date. On the basis of such evidence:

(a) where it is more likely than not that a present obligation exists at the balance sheet date, the enterprise recognises a provision (if the recognition criteria are met); and

(b) where it is more likely that no present obligation exists at the balance sheet date, the enterprise discloses a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote (see paragraph 68).

16. A past event that leads to a present obligation is called an obligating event. For an event to be an obligating event, it is necessary that the enterprise has no realistic alternative to settling the obligation created by the event.”

“18. It is only those obligations arising from past events existing independently of an enterprise’s future actions (i.e. the future conduct of its business) that are recognised as provisions. …”

“26. An enterprise should not recognise a contingent liability.

27. A contingent liability is disclosed, as required by paragraph 68, unless the possibility of an outflow of resources embodying economic benefits is remote.”

“29. Contingent liabilities may develop in a way not initially expected. Therefore, they are assessed continually to determine whether an outflow of resources embodying economic benefits has become probable. If it becomes probable that an outflow of future economic benefits will be required for an item previously dealt with as a contingent liability, a provision is recognised in accordance with paragraph 14 in the financial statements of the period in which the change in probability occurs (except in the extremely rare circumstances where no reliable estimate can be made).”

“66. For each class of provision, an enterprise should disclose:

(a) the carrying amount at the beginning and end of the period;

(b) additional provisions made in the period, including increases to existing provisions;

(c) amounts used (i.e. incurred and charged against the provision) during the period; and

(d) unused amounts reversed during the period.

67. An enterprise should disclose the following for each class of provision:

(a) a brief description of the nature of the obligation and the expected timing of any resulting outflows of economic benefits;

(b) an indication of the uncertainties about those outflows. Where necessary to provide adequate information, an enterprise should disclose the major assumptions made concerning future events, as addressed in paragraph 41; and

(c) the amount of any expected reimbursement, stating the amount of any asset that has been recognised for that expected reimbursement.

68. Unless the possibility of any outflow in settlement is remote, an enterprise should disclose for each class of contingent liability at the balance sheet date a brief description of the nature of the contingent liability and, where practicable:

(a) an estimate of its financial effect, measured under paragraphs 35-45;

(b) an indication of the uncertainties relating to any outflow; and

(c) the possibility of any reimbursement.

…”

“71. Where any of the information required by paragraph 68 is not disclosed because it is not practicable to do so, that fact should be stated.

72. In extremely rare cases, disclosure of some or all of the information required by paragraphs 66-70 can be expected to prejudice seriously the position of the enterprise in a dispute with other parties on the subject matter of the provision or contingent liability. In such cases, an enterprise need not disclose the information, but should disclose the general nature of the dispute, together with the fact that, and reason why, the information has not been disclosed.”

24. From the above, the Committee is of the view that the company should, based on all the available evidence, assess whether there is a present obligation or a possible obligation towards the interest liability beyond the originally scheduled commercial operation date. If it is considered probable (i.e., more likely than not) that a present obligation towards interest liability exists at the balance sheet date and it is probable that the said obligation will be settled and a reliable estimate can be made, the company should recognise a provision for the interest liability and make related disclosures. If, however, it is considered that the recognition criteria for making a provision are not met, then, the company should not make a provision for the disputed interest liability. In that situation, the company should disclose the same as a contingent liability, with relevant disclosures in this regard as per AS 29, unless the possibility of an outflow of resources embodying economic benefits is remote.

D. Opinion

25. On the basis of the above, and while refraining from interpreting the terms of the Agreement and also refraining from expressing any view involving legal implications, the Committee is of the opinion that the company should, based on all the available evidence, assess whether there is a present or possible obligation towards the interest liability beyond the originally scheduled commercial operation date. If it is considered probable that a present obligation exists at the balance sheet date and the said obligatin will be settled, of which a reliable estimate can be made, the company should recognise a provision for the interest liability and make related disclosures. If, however, it is considered that the recognition criteria for making a provision are not met, then, the company should instead, disclose the same as a contingent liability, with relevant disclosures in this regard as per AS 29, unless the possibility of an outflow of resources embodying economic benefits is remote. If the above-said requirements are complied with, the Committee is of the opinion that the annual accounts of the company would be considered to have been drawn in accordance with the provisions of the Companies Act, 1956 and the applicable Accounting Standards.

1Opinion finalised by the Committee on 22.1.2010

|