|

Query No. 37.

Subject:

Creation of deferred tax assets. 1

A. Facts of the Case

1. A company is a central public sector enterprise under the Ministry of Oil and Natural Gas. The querist has stated that at present, the company has five business segments as below:

(i) Manufacture and servicing of electrical switchgears,

(ii) Execution of turnkey electrical projects,

(iii) Blending of lube oil,

(iv) Repair of industrial motors, and

(v) Third party inspection agency business for power projects.

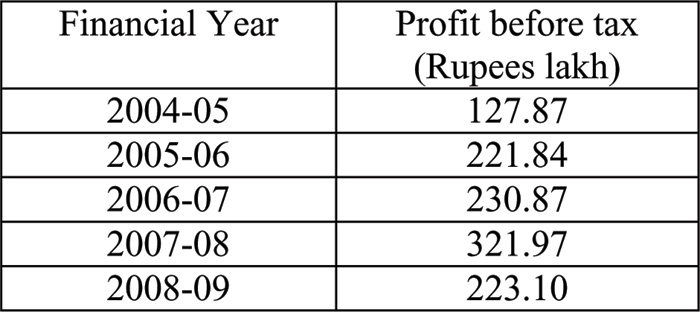

2. The company intermittently suffered losses till the financial year 2003-04. Since the financial year 2004-05, the company is earning uninterrupted profit, details of which are given below:

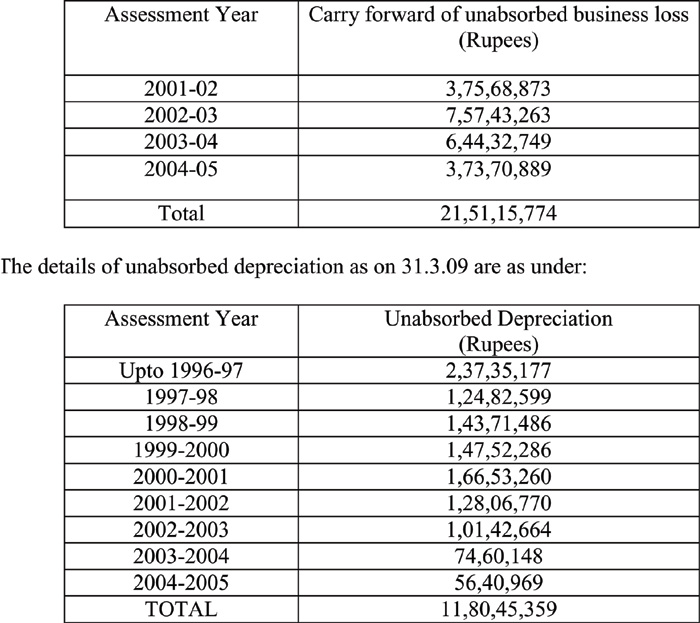

3. The querist has stated that as a result of past losses, the accumulated balance of loss at the end of the financial year 2008-09, stood at Rs. 50.33 crore. Resultantly, the company has negative net worth of Rs. 8.02 crore as on 31st March, 2009. The company is a sick industrial company within the meaning of the Sick Industrial Companies (Special Provisions) Act, 1985 and has submitted a restructuring plan to the Government of India. These past losses have, however, given rise to accumulated business loss and unabsorbed depreciation in favour of the company as per the Income-tax Act, 1961. The details of such unabsorbed business loss as on 31.3.09 are as under:

4. The querist has further stated that since the financial year 2004-05, successive auditors conducting statutory audits of the company have emphasised in their audit reports that the company was not recognising effects of deferred tax in the books of account as is required mandatorily by Accounting Standard (AS) 22, ‘Accounting for Taxes on Income’. Therefore, as per the querist, while preparing accounts for the financial year 2007-08, the company had to introduce tax effect accounting in its books by creating net deferred tax asset consisting of unabsorbed depreciation and provision for doubtful debts, and adjusting therefrom deferred tax liability consisting of differential effects of depreciation. The transitional adjustment for creating deferred tax asset was effected by crediting debit balance of profit and loss account.

5. According to the querist, pursuing the policy of rigid conservatism, the company chose to ignore unabsorbed business loss in deferred tax computation because unabsorbed business loss has finite time limit of carry forward, which is eight assessment years reckoned from the assessment year in which loss was suffered. Unabsorbed depreciation was, however, taken into consideration in the computation of deferred tax asset as this has no time limit for carry forward as per the Income-tax Act, 1961.

6. The querist has informed that for the financial year 2009-10, the management is virtually certain that the company will earn profit. The expectation is based on the improved order position and upward trend in the power sector in which the company operates. The querist has also pointed out that the power sector is targeting an all time high generation of over 78,000 mw in the 11th plan (2007-12). In order to meet the above target, accelerated power development and reform programme (APDRP) has been revamped with an increased allocation of funds. This higher allocation is directly benefiting and will continue to benefit manufacturers of power equipments and turnkey contractors in power sector, like, the company. Besides, according to the querist, the following facts serve as convincing evidence supporting the virtual certainty perception of the company:

(i) The company, since the financial year 2004-05, is uninterruptedly making profits, the details of which have been given in paragraph 2 above.

(ii) The management, while preparing accounts of the company for the financial year 2008-09 has reviewed its going concern status and is of the opinion that there exists no indicator casting significant doubt on the company’s ability to continue as a going concern. This view of the management has been endorsed by the auditors in accordance with Auditing and Assurance Standard (AAS) 16, ‘Going Concern’2 , issued by the Institute of Chartered Accountants of India, and the said fact has been duly disclosed in the audit report for the financial year 2008-09.

(iii) The project division of the company has been awarded contracts worth Rs. 68.6 crore till September 2009. Turnover achieved by this segment in the financial year 2008-09 was only Rs. 4.70 crore.

(iv) The company has embarked on a new segment of operation namely testing and inspection services for power projects and upto September 2009, has been awarded contracts worth Rs. 7.00 crore.

Besides the above, orders worth Rs. 8.5 crore are in the pipeline.

(v) For the switchgear segment, the orders booked along with the orders in the course of negotiation with prospective and existing customers coupled with the buoyancy in the segment indicate that the company will continue to retain its present business trend.

(vi) Electrical repair division has already booked orders worth Rs. 4.56 crore in the half year ended 30th September, 2009. The corresponding figure for the last year was Rs. 3.22 crore. Given the current positive state in the segment, it is expected that the upswing in order booking will continue.

(vii) Lube division has already bagged orders worth Rs. 81.63 lakh. The corresponding figure for the last year was Rs. 56.17 lakh.

Riding on the factors enumerated above and based on worst case scenario, as per the querist, the company presently estimates that it will continue to post profit in the coming years.

7. The querist has informed that the company is already enjoying set-off of unabsorbed business loss in income-tax assessments and the same will continue in the remaining period of three years out of the prescribed time frame of eight assessment years.

8. The querist has also mentioned in this context that the company as a strategic measure has tried to insulate itself from the risk of declining profit by resorting to diversified business activities and thereby ensuring that unforeseen loss of profit in one segment is offset by profits earned in other segments.

B. Query

9. Based on the facts and evidence adduced above, the provisions contained in paragraphs 15, 16 and 26 of AS 22 and also taking into consideration the facts that the accumulated loss of the company as on 31st March, 2009 is Rs. 50.33 crore, the company is a sick industrial company within the meaning of the Sick Industrial Companies (Special Provisions) Act, 1985, and that the company has submitted a restructuring plan to the Government of India, the querist has sought the opinion of the Expert Advisory Committee as to whether the company should retain deferred tax assets in its books.

C. Points considered by the Committee

10. The Committee notes that the company has created deferred tax assets for the first time in the financial year 2007-08 and has raised an issue as to whether the company should retain such deferred tax assets in its books while preparing financial statements for the financial year 2008-09 considering the various facts enumerated by the querist in the Facts of the Case. Accordingly, the Committee, while expressing its opinion has considered only this issue and has not touched upon any other issue that may arise from the Facts of the Case, such as, computation of deferred tax assets, transitional adjustments of creation of deferred taxes in the books of account of the company, propriety of ignoring unabsorbed business losses in deferred tax computation, offsetting of deferred tax assets and deferred tax liabilities, etc.

11. The Committee notes paragraphs 15, 16 and 26 of AS 22 referred by the querist in paragraph 9 above and paragraphs 17 and 18 thereof which provide as below:

“15. Except in the situations stated in paragraph 17, deferred tax assets should be recognised and carried forward only to the extent that there is a reasonable certainty that sufficient future taxable income will be available against which such deferred tax assets can be realised.

16. While recognising the tax effect of timing differences, consideration of prudence cannot be ignored. Therefore, deferred tax assets are recognised and carried forward only to the extent that there is a reasonable certainty of their realisation. This reasonable level of certainty would normally be achieved by examining the past record of the enterprise and by making realistic estimates of profits for the future.

17. Where an enterprise has unabsorbed depreciation or carry forward of losses under tax laws, deferred tax assets should be recognised only to the extent that there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised.

18. The existence of unabsorbed depreciation or carry forward of losses under tax laws is strong evidence that future taxable income may not be available. Therefore, when an enterprise has a history of recent losses, the enterprise recognises deferred tax assets only to the extent that it has timing differences the reversal of which will result in sufficient income or there is other convincing evidence that sufficient taxable income will be available against which such deferred tax assets can be realised. In such circumstances, the nature of the evidence supporting its recognition is disclosed.”

“26. The carrying amount of deferred tax assets should be reviewed at each balance sheet date. An enterprise should write-down the carrying amount of a deferred tax asset to the extent that it is no longer reasonably certain or virtually certain, as the case may be (see paragraphs 15 to 18), that sufficient future taxable income will be available against which deferred tax asset can be realised. Any such write-down may be reversed to the extent that it becomes reasonably certain or virtually certain, as the case may be (see paragraphs 15 to 18), that sufficient future taxable income will be available.”

12. The Committee notes from the Facts of the Case that the company has unabsorbed depreciation and carried forward losses as on 31st March, 2009. Accordingly, in the view of the Committee, the provisions contained in paragraph 17 of AS 22 instead of paragraphs 15 and 16 thereof shall apply to the present case. Thus, deferred tax asset in the present case, can be retained and carried forward only to the extent there is virtual certainty, supported by convincing evidence (rather than mere reasonable certainty), that sufficient future taxable income would be available against which such deferred tax assets can be realised.

13. The Committee further notes that AS 22 notified by the Central Government under the Companies (Accounting Standards) Rules, 2006, contains, inter alia, an Explanation to paragraph 17 thereof regarding virtual certainty (which was hitherto contained in the consensus portion of Accounting Standards Interpretation (ASI) 9, Virtual certainty supported by convincing evidence, issued by the Institute of Chartered Accountants of India), which provides as below:

“Explanation:

1. Determination of virtual certainty that sufficient future taxable income will be available is a matter of judgement based on convincing evidence and will have to be evaluated on a case to case basis. Virtual certainty refers to the extent of certainty, which, for all practical purposes, can be considered certain. Virtual certainty cannot be based merely on forecasts of performance such as business plans. Virtual certainty is not a matter of perception and is to be supported by convincing evidence. Evidence is a matter of fact. To be convincing, the evidence should be available at the reporting date in a concrete form, for example, a profitable binding export order, cancellation of which will result in payment of heavy damages by the defaulting party. On the other hand, a projection of the future profits made by an enterprise based on the future capital expenditures or future restructuring etc., submitted even to an outside agency, e.g., to a credit agency for obtaining loans and accepted by that agency cannot, in isolation, be considered as convincing evidence.”

14. On the basis of the above, the Committee is of the view that the confirmed orders secured by the company upto the reporting date, i.e., as on March 31, 2009 can only be considered while creating deferred tax asset provided these are binding on the other party and it can be demonstrated that they will result in future taxable income. However, mere projections made by the company indicating the earning of profits from future orders and upward trend in power sector, or submission of financial restructuring proposal to the Government of India or allocation of funds under APDRP, or the fact that the books of account of the company are prepared on ‘going concern’ basis, as mentioned by the querist, can not be considered as convincing evidence of virtual certainty as contemplated in the ‘Explanation’ to paragraph 17 of AS 22 reproduced above. These may, at best, indicate a ‘reasonable certainty’ of future profitability. Further, the mere fact that unabsorbed depreciation can be carried forward for unlimited number of years, as mentioned by the querist in paragraph 5 above, can also not be a ground for recognising a deferred tax asset since paragraph 17 of AS 22 read with its ‘Explanation’, requires virtual certainty supported by convincing evidence at the date of the balance sheet. The Committee also wishes to point out that a deferred tax asset can be created to the extent future taxable income will be available from future reversal of any deferred tax liability recognised at the balance sheet date. To that extent, it would not be necessary to consider the level of virtual certainty supported by convincing evidence.

D. Opinion

15. On the basis of the above, the Committee is of the opinion that the company should retain deferred tax assets in its books only to the extent it is virtually certain, supported by convincing evidence, as on the date of the balance sheet, that sufficient future taxable income would be available against which such deferred tax assets can be realised. Factors to be taken into account for determining ‘virtual certainty’ are discussed in paragraph 14 above.

1Opinion finalised by the Committee on 22.1.2010

2Auditing and Assurance Standard (AAS) 16 has been revised, renamed, renumbered and categorised as Standard on Auditing (SA) 570 (Revised), ‘Going Concern’. |