|

A. Facts of the Case

1. A public sector company registered under the Companies Act, 1956 is engaged in construction and operation of hydro electric power projects.

2. The company borrows in foreign currency to meet its fund requirement for construction of projects. Such foreign currency loans are taken for acquiring assets from outside India and also for acquiring assets from within India. The querist has stated that all the agreements for foreign currency loans had been entered into prior to 01.04.2004. During the construction stage of a hydro project, no profit and loss account is prepared. Indirect expenditure during construction, such as, employee cost, depreciation and interest cost (net of any receipts) are taken to an account known as ‘Incidental Expenditure During Construction (IEDC)’, which is prepared in lieu of profit and loss account. The whole of the direct capital expenditure and the indirect expenditure during construction becomes the total capitalised cost of the project on commissioning of the project. Profit and loss account of a project is prepared from the date of commencement of commercial operation (COD). During the construction phase, the project is termed as ‘construction project’ and after COD, it is termed as ‘power station’.

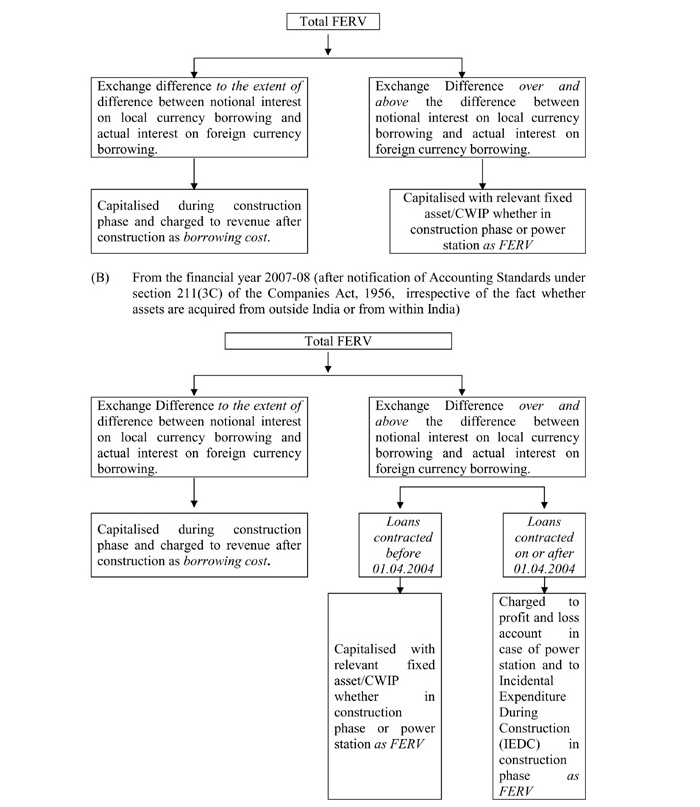

3. The querist has stated that the company has been giving accounting treatment to foreign exchange rate variation (FERV) on restatement of loan utilised for acquiring assets as per the provisions of Accounting Standard (AS) 11, ‘Accounting for the Effects of Changes in Foreign Exchange Rates’ (1994), read with Accounting Standard (AS) 16, ‘Borrowing Costs’, and Accounting Standards Interpretation (ASI) 102 on Interpretation of paragraph 4(e) of AS 16, issued by the Institute of Chartered Accountants of India, which is explained below through pictorial diagrams:

(A) Till the financial year 2006-07 (prior to notification of Accounting Standards under section 211(3C) of the Companies Act, 1956)

Case I: FERV in respect of loans contracted prior to 01.04.2004 for acquiring assets from outside India:

The whole of FERV (gain or loss) was capitalised keeping in view the provisions contained in Schedule VI3 to the Companies Act, 1956, irrespective of whether the project was a construction project or power station. In case of a construction project, FERV was debited/credited to Capital Work-in-Progress (‘CWIP’) and in case of power station the same was debited/credited to the respective fixed assets.

Case II: FERV (gain or loss) in respect of loans contracted prior to 01.04.2004 for acquiring assets from within India:

(Emphasis supplied by the querist.)

4. The company is under regulatory regime and tariff (sale price) for electricity is fixed by Central Electricity Regulatory Commission (CERC). The querist has stated that as per one of the latest regulation, exchange rate variation loss incurred by power station is recoverable from the beneficiary, i.e., the company’s customers. As such, according to the querist, irrespective of any accounting treatment of FERV, i.e., whether to charge/credit FERV in the profit and loss account or to capitalise/decapitalise in carrying value of assets, FERV shall not be having any impact on the profit and loss account in view of an earlier opinion expressed by the Expert Advisory Committee of the Institute of Chartered Accountants of India published as Query No. 37 in the Compendium of Opinions – Vol.XXV.

5. During the financial year 2007-08, the company has incurred FERV loss (net of FERV gain at one of the locations). FERV loss and gain was compared with the difference between the interest on local currency borrowings and the interest on foreign currency borrowings in order to know the amount of FERV which can be regarded as adjustment to interest cost in terms of paragraph 4(e) of AS 16, as per which, borrowing costs may include ‘exchange differences arising from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs’. FERV loss to the extent of difference between the interest on local currency borrowings and the interest on foreign currency borrowings has been accounted for as borrowing cost and charged to profit and loss account in case of power station. Following the same principle, FERV gain amounting to Rs. 7.41 crore arising out of the foreign currency loan contracted prior to 01.04.2004 in respect of one of the power stations was credited to the profit and loss account as borrowing cost (negative). This treatment was done because, as per the querist, such FERV loss/gain satisfies the criteria of paragraph 4(e) of AS 16 read with paragraph 3 of ASI 10 which is reproduced below:

“… If the difference between the interest on local currency borrowings and the interest on foreign currency borrowings is equal to or more than the exchange difference on the amount of principal of the foreign currency borrowings, the entire amount of exchange difference is covered under paragraph 4(e) of AS 16.”

In other words, according to the querist, FERV gain shall always be less than the difference between the interest on local currency borrowings and the interest on foreign currency borrowings and, as such, the whole of FERV gain qualifies to be covered under paragraph 4(e) of AS 16 (emphasis supplied by the querist).

6. However, during the audit of accounts for the financial year 2007-08, the government auditors gave an observation on the accounting treatment given by the company in respect of FERV gain. The contention of the auditors was that FERV gain should have been adjusted in the carrying amount of the respective fixed assets of the power station instead of crediting to the profit and loss account.

7. The management is of the view that ASI 10 on interpretation of paragraph 4(e) of AS 16 does not distinguish between FERV loss and FERV gain. As per the management, the basic underlying principle as given in ASI 10 is to treat the entire FERV as borrowing cost, if it is less than or equal to the difference between the interest on local currency borrowings and the interest on foreign currency borrowings. As such, by virtue of this principle, when FERV becomes borrowing cost, the provisions of AS 16 should apply. In this regard, the querist has reproduced the following extract from the company’s reply to the auditors:

“… In any case, the difference between interest on local currency borrowings and the interest on foreign currency borrowings in the above case is more than the FERV gain of Rs. 7.41 crore and accordingly the same has been recognised as an adjustment to the borrowing cost. If we were to adjust this gain in the carrying amount of respective assets, ASI 10 on AS 16 would not have been complied with.”

The auditors’ observation was not pressed further on the assurance that the management shall solicit the opinion of the Expert Advisory Committee of the Institute of Chartered Accountants of India on the issue (emphasis supplied by the querist).

B. Query

8. Keeping in view the above, the querist has sought the opinion of the Expert Advisory Committee on the following issues:

(i) Whether the accounting treatment followed by the company as explained in paragraph 5 above is correct.

(ii) Other alternative treatment, if any, in lieu of the aforesaid treatment.

C. Points considered by the Committee

9. The Committee notes that the basic issue raised by the querist relates to the treatment of FERV loss/gain on foreign currency loan transactions entered into prior to 1.4.2004. Therefore, the Committee has examined only this issue and has not examined any other issue that may be contained in the Facts of the Case, such as, non-preparation of profit and loss account for the construction project which needs to be examined separately, capitalisation of whole of the indirect expenditure incurred during construction of the project, etc. The Committee has also not examined the aspect of appropriateness of netting off of the FERV loss and FERV gain mentioned by the querist in paragraph 5 above, as the relevant information in this respect has not been provided. The querist has stated in the facts of the case that all the agreements for foreign currency loans had been entered into/contracted prior to 01.04.2004. The Committee presumes that the loan ‘transactions’ were entered into prior to 1.4.2004 and, therefore, Accounting Standard (AS) 11, ‘Accounting for the Effects of Changes in Foreign Exchange Rates’ (1994) is applicable. It appears to the Committee that interest on notional local currency borrowing exceeds interest on foreign currency borrowing in all the cases.

10. The Committee notes that AS 11, notified under the Companies (Accounting Standards) Rules, 2006, (the Rules), carries inter alia, the following footnote:

“In respect of accounting for transactions in foreign currencies entered into by the reporting enterprise itself or through its branches before the effective date of the notification prescribing this Standard under Section 211 of the Companies Act, 1956, the applicability of this Standard would be determined on the basis of the Accounting Standard (AS) 11 revised by the ICAI in 2003.”

The Committee notes that the preamble to AS 11 (revised 2003) states as follows:

“Accounting Standard (AS) 11, The Effects of Changes in Foreign Exchange Rates (revised 2003), issued by the Council of the Institute of Chartered Accountants of India, comes into effect in respect of accounting periods commencing on or after 1-4-2004 and is mandatory in nature from that date. The revised Standard supersedes Accounting Standard (AS) 11, Accounting for the Effects of Changes in Foreign Exchange Rates (1994), except that in respect of accounting for transactions in foreign currencies entered into by the reporting enterprise itself or through its branches before the date this Standard comes into effect, AS 11 (1994) will continue to be applicable.”

From the above, the Committee is of the view that in the year 2007-08, for the transactions entered into prior to 01.04.2004, AS 11(1994) continues to apply.

11. The Committee notes that AS 11 (1994) requires that the exchange differences arising on foreign currency borrowings for the purpose of acquiring fixed assets should be adjusted in the carrying amount of the respective fixed assets. The requirements in this regard are contained in paragraph 10 of the said Standard which is reproduced below:

“10. Exchange differences arising on repayment of liabilities incurred for the purpose of acquiring fixed assets, which are carried in terms of historical cost, should be adjusted in the carrying amount of the respective fixed assets. The carrying amount of such fixed assets should, to the extent not already so adjusted or otherwise accounted for, also be adjusted to account for any increase or decrease in the liability of the enterprise, as expressed in the reporting currency by applying the closing rate, for making payment towards the whole or a part of the cost of the assets or for repayment of the whole or a part of the monies borrowed by the enterprise from any person, directly or indirectly, in foreign currency specifically for the purpose of acquiring those assets.”

12 The Committee notes that Accounting Standard (AS) 16, ‘Borrowing Costs’, issued by the Institute of Chartered Accountants of India, came into effect in respect of accounting periods commencing on or after 1.4.2000. This Standard was later notified under the Companies (Accounting Standards) Rules, 2006. Paragraph 4(e) of this Standard states that borrowing costs include exchange differences arising from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs. The Institute of Chartered Accountants of India issued ASI 10 on Interpretation of paragraph 4(e) of AS 16, whose consensus portion formed the basis for the ‘Explanation’ to paragraph 4(e) of AS 16 which was notified under the Rules. The Committee notes the ‘Explanation’ to paragraph 4(e) which is reproduced below:

“Explanation:

Exchange differences arising from foreign currency borrowings and considered as borrowing costs are those exchange differences which arise on the amount of principal of the foreign currency borrowings to the extent of the difference between interest on local currency borrowings and interest on foreign currency borrowings. Thus, the amount of exchange difference not exceeding the difference between interest on local currency borrowings and interest on foreign currency borrowings is considered as borrowings costs to be accounted for under this Standard and the remaining exchange difference, if any, is accounted for under AS 11, The Effects of Changes in Foreign Exchange Rates. For this purpose, the interest rate for the local currency borrowings is considered as that rate at which the enterprise would have raised the borrowings locally had the enterprise not decided to raise the foreign currency borrowings.”

13. From the above, the Committee is of the following view in respect of foreign exchange loss on account of foreign currency borrowings for the purpose of fixed assets:

A. When the construction period is over, i.e., in case of power station

(i) Till the financial year 1999-2000 (i.e., upto 31st March, 2000)

The entire foreign exchange loss should be added to the cost of the relevant fixed assets.

(ii) From the financial year 2000-01 (i.e., from 1.4.2000)

(a) The foreign exchange loss on principal amount of foreign currency borrowings to the extent of the difference between interest on local currency borrowings and interest on foreign currency borrowings is a borrowing cost under paragraph 4(e) of AS 16. The same should be expensed, i.e., charged to the profit and loss account because the relevant fixed asset is not a qualifying asset under AS 16, irrespective of the requirements of Schedule VI (in relation to capitalisation of foreign exchange differences) which do not apply to borrowing cost.

(b) The foreign exchange loss other than that covered under (a) above should be added to the cost of the relevant fixed asset in view of the requirements of AS 11 (1994).

B. When the construction period is not over, i.e., in case of construction project

The entire foreign exchange loss should be added to the cost of the relevant fixed assets either as a part of the borrowing costs (keeping in view the applicability of paragraph 4(e) of AS 16) or as foreign exchange differences covered under AS 11 (1994).

14. The Committee is of the following view in respect of foreign exchange gain on foreign currency borrowings for the purpose of fixed assets:

A. When the construction period is over, i.e., in case of power station

The entire foreign exchange gain on the borrowings should be reduced from the cost of the fixed assets keeping in view the requirements of AS 11 (1994).

B. When the construction period is not over, i.e., in case of construction project

(i) Till the financial year 1999-2000 (i.e., upto 31st March, 2000)

The entire foreign exchange gain should be reduced from the cost of the relevant fixed assets keeping in view the requirements of AS 11 (1994).

(ii) From the financial year 2000-01 (i.e., from 1.4.2000)

The entire foreign exchange gain should be reduced from the cost of the relevant fixed assets either in the form of reduced borrowing costs (to the extent the foreign exchange loss was added to the cost of the fixed assets under paragraph 4(e) of AS 16) or as foreign exchange differences under AS 11 (1994).

15. With respect to the treatment followed by the company as stated in paragraph 5 above, from the year 2007-08, the Committee is of the view that the treatment followed by the company is not entirely correct. The treatment should be in accordance with the treatment explained in paragraphs 13 and 14 above. The Committee does not agree with the reasoning given by the querist in paragraph 5 above for the treatment followed by the company.

D. Opinion

16. On the basis of the above, under the presumptions/circumstances of the company as stated in paragraph 9 above, the Committee is of the following opinion on the issues raised by the querist in paragraph 8 above:

(i) The accounting treatment followed by the company as explained in paragraph 5 above is not entirely correct. The correct treatment would be the treatment explained in paragraphs 13 and 14 above.

(ii) In view of the correct treatment explained in paragraphs 13 and 14 above, the question of alternative treatment does not arise.

Opinion finalised by the Committee on 8.5.2009

The ASI 10 has been withdrawn by the Council of the Institute of Chartered Accountants of India and the Consensus portion thereof has been added as ‘Explanation’ to the paragraph 4(e) of Accounting Standard (AS) 16, ‘Borrowing Costs’.

Schedule VI has since been revised. Revised Schedule VI came into force for the Balance Sheet and Profit and Loss Account for the

1Opinion finalised by the Committee on 8.5.2009

2The ASI 10 has been withdrawn by the Council of the Institute of Chartered Accountants of India and the Consensus portion thereof has been added as ‘Explanation’ to the paragraph 4(e) of Accounting Standard (AS) 16, ‘Borrowing Costs’.

3Schedule VI has since been revised. Revised Schedule VI came into force for the Balance Sheet and Profit and Loss Account for the financial year commencing on or after 01.04.2011.

|