|

Query No. 21

Subject: Accounting treatment of ‘Amounts Billed to Clients’ and ‘Work-in-Progress’.

A. Facts of the Case

1. A Government of India enterprise (hereinafter referred to as ‘the company’) is an integrated engineering project management and construction company having rich experience of handling wide range of projects and turnkey execution capabilities in major areas of operation. The projects undertaken are spread over a number of years and are being executed in India and abroad. The accounting policy followed by the company is as follows:

Accounting Policy No. 3 (Revenue recognition)

(a) Work done

(i) Work done for the year is arrived at by subtracting opening work in progress from the accumulated work in progress for each contract. In respect of cases where ultimate collection with reasonable certainty is lacking at the time of claim, recognition is postponed till collection is made.

(ii) Valuation of work-in-progress: Work-in-progress is valued by taking cumulative actual costs incurred upto the end of the year without considering miscellaneous income, plus proportionate estimated profit, based on contract cost reviewed at the end of each year allocated on “percentage of completion method”.

(iii) At the year-end, works executed but not measured /partly executed are accounted for based on the certification by engineers, entries arising out of such accounting are reversed in the following accounting year. Accordingly, statutory obligations are met with at the time of actual receipt /issue of bills/claims.

(iv) In case of projects foreclosed/terminated, revenue is recognised only to the extent of contract value of which recovery is probable.

(v) Revenue from consultancy services is recognised on proportionate completion method. In respect of cases where ultimate collection with reasonable certainty is lacking at the time of claim, recognition is postponed till collection is made.

(vi) In case of contracts where the contract costs exceed the contract revenues, anticipated loss is recognised immediately.

(b) Escalation and extra works not provided for in the contract with client, claims out of arbitration awards and insurance claims are accounted for on receipt basis.

(c) Liquidated damages arising from contractual obligations in respect of contracts under dispute/negotiation and not considered payable/receivable are not accounted for till final settlement.

Accounting Policy No. 5 (Inventory/ Work in Progress)

The contract is considered as closed for accounting purposes upon final billing, commissioning certificate, commercial run, foreclosure and /or termination, whichever is earlier. Till closure of each contract, cumulative value of ‘amount billed to client’ is shown under ‘other current liabilities’ and cumulative amount of work done is shown as ‘work-in-progress’ under ‘Inventories’. On closure/foreclosure/termination of a contract ‘amount billed to client’ is set off against value of ‘work-in-progress’.

2. While finalising the annual accounts of the company for the financial year 2012-13, the statutory auditors have raised an objection that the presentation of work-in-progress (WIP) and amount billed to client is not in line with Accounting Standard (AS) 7, ‘Construction Contracts’ and not as per the practice followed by other construction companies. Presently, as per the accounting policy no. 5, “till closure of the contract, cumulative value of amount billed to client is shown under other current liabilities and cumulative amount of work done is shown as work-in-progress under inventories. On closure of contract, amount billed to client is set off against value of work-in-progress”. In this connection, the company assured the statutory auditors that it will seek the opinion from the Expert Advisory Committee (EAC) of the Institute of Chartered Accountants of India (ICAI) during the financial year 2013-14 in respect of presentation of amount billed to client and work-in-progress.

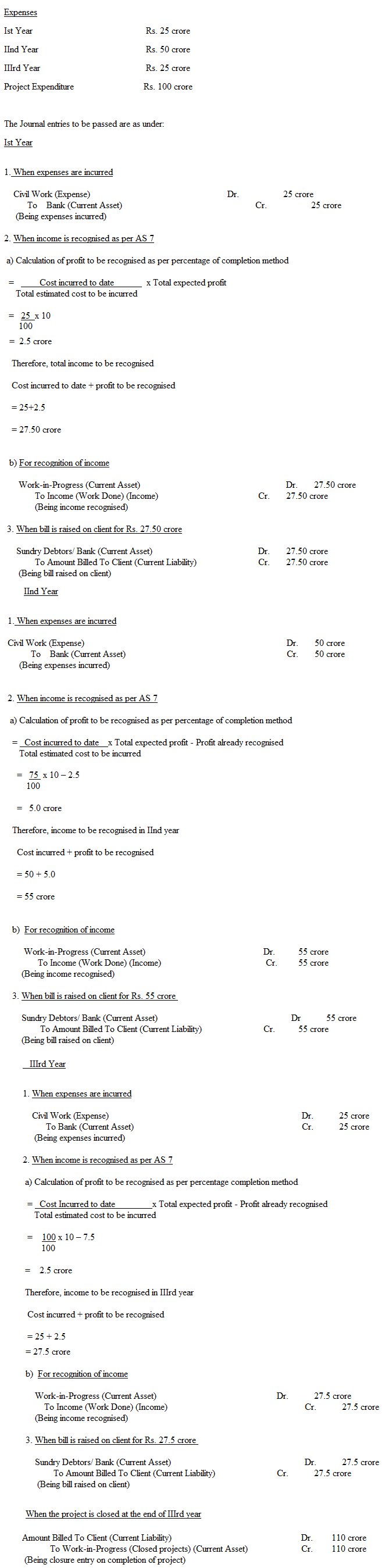

3. The querist has explained the accounting treatment followed by the company with the help of the following illustration:

Suppose the company is executing a project worth Rs. 110 crore. The project is expected to earn a profit of Rs. 10 crore after taking into account the project expenses of Rs. 100 crore over the 3 year duration, as per the following break-up:

Ledgers:

Work-in-progress:

Dr. Cr.

1st year |

27.50 crore |

|

1st year |

|

2nd year |

55.00 crore |

|

2nd year |

|

3rd year |

27.50 crore |

|

3rd year |

|

|

|

|

On project closure |

110.00 crore |

Total |

110.00 crore |

|

Total |

110.00 crore |

Amount billed to client:

Dr. Cr.

1st year |

|

|

1st year |

27.50 crore |

2nd year |

|

|

2nd year |

55.00 crore |

3rd year |

|

|

3rd year |

27.50 crore |

On project closure |

110.00 crore |

|

|

|

Total |

110.00 crore |

|

Total |

110.00 crore |

4. The querist has mentioned that in the year 1987, the EAC of the ICAI had issued an opinion on presentation of work-in-progress and amount billed to client. The opinion was published in Volume VII of the Compendium of Opinions (Query No. 1.19), wherein it was opined that:

“(i) The revenue should be recognised in respect of the value of work accomplished on the contracts by evaluating the work-in-progress.

(ii) Work-in-progress should be shown under the head ‘Current Assets’ and valued at cost incurred on the contract plus profit taken thereon in accordance with the formulae followed by the company, less cash received from the clients (progress payments). Alternatively, progress payments can be shown under the head ‘Current Liabilities’.

(iii) In view of the above, ‘Amount billed to clients A/c’ and ‘Clients A/c’ will not appear anywhere on the ‘Liabilities’ and ‘Assets’ side of the balance sheet.”

B. Query

5. In view of the above, the querist has requested the Expert Advisory Committee of the ICAI to give its opinion as to whether the accounting treatment followed by the company with regard to presentation of work-in-progress as envisaged in the company’s accounting policy no. 5 as stated above, is correct or not. Further, as per the revised AS 7, whether there is any change in the opinion on the above subject dated July 29, 1987 of the Committee.

C. Points considered by the Committee

6. The Committee notes that the basic issue raised by the querist relates to whether the accounting treatment followed by the company with regard to presentation of work-in-progress as envisaged in the company’s accounting policy no. 5 as stated above, is correct or not. Accordingly, the Committee has considered only this issue and has not considered any other issue that may arise from the Facts of the Case, such as, correctness of accounting policies followed by the company as explained in paragraph 1 above, viz., recognition of revenue from consultancy services, accounting of claims out of arbitration awards, insurance claims, liquidated damages arising from contractual obligations, entries passed by the company for works executed but not measured/partly executed and reversal of such entries in the following accounting year, etc. The Committee presumes that the extant query has been raised in the context of contracts entered into during accounting periods commencing on or after 1.4.2003, to which revised AS 7 is applicable.

7. The Committee notes from the Facts of the Case that the company is recognising ‘amount due from customers for contract work done’ as ‘receivables’, and is also recognising cumulative value of ‘amount billed to client’ as ‘other current liability’. Further, the cumulative amount of work done is shown as ‘work-in-progress’ under ‘Inventories’ on the assets side of the balance sheet at cumulative actual costs incurred upto the end of the year and proportionate estimated profit. On closure/foreclosure/termination of a contract, ‘amount billed to client’ is set off against value of ‘work-in-progress’.

8. The Committee notes that Accounting Standard (AS) 7 (revised 2002), ‘Construction Contracts’ notified under the Companies (Accounting Standards) Rules, 2006 (hereinafter referred to as the ‘Rules’), requires in paragraph 21, that “contract revenue and contract costs associated with the construction contract should be recognised as revenue and expenses respectively by reference to the stage of completion of the contract activity at the reporting date”. The Committee further notes that paragraph 24 of AS 7 (revised 2002), notified under the Rules states that “the recognition of revenue and expenses by reference to the stage of completion of a contract is often referred to as the percentage of completion method”.

9. The Committee further notes the following paragraphs of AS 7 (revised 2002), notified under the Rules:

“25. Under the percentage of completion method, contract revenue is recognised as revenue in the statement of profit and loss in the accounting periods in which the work is performed. Contract costs are usually recognised as an expense in the statement of profit and loss in the accounting periods in which the work to which they relate is performed. However, any expected excess of total contract costs over total contract revenue for the contract is recognised as an expense immediately in accordance with paragraph 35.

26. A contractor may have incurred contract costs that relate to future activity on the contract. Such contract costs are recognised as an asset provided it is probable that they will be recovered. Such costs represent an amount due from the customer and are often classified as contract work in progress.”

“39. An enterprise should disclose the following for contracts in progress at the reporting date:

(a) the aggregate amount of costs incurred and recognised profits (less recognised losses) upto the reporting date;

(b) the amount of advances received; and

(c) the amount of retentions.”

“41. An enterprise should present:

(a) the gross amount due from customers for contract work as an asset; and

(b) the gross amount due to customers for contract work as a liability.

42. The gross amount due from customers for contract work is the net amount of:

(a) costs incurred plus recognised profits; less

(b) the sum of recognised losses and progress billings

for all contracts in progress for which costs incurred plus recognised profits (less recognised losses) exceeds progress billings.”

10. From the above, the Committee is of the view that under the percentage of completion method, revenue is recognised on the basis of stage of completion irrespective of the fact whether or not payment has been received or settled. Work-in-progress can be recognised and presented only in respect of costs incurred by an enterprise that relate to future activity on the contract, provided these are capable of recovery. For example, an enterprise might have bought construction material which will be used in future for completing the contract. The Committee, however, notes from the Facts of the Case that the company is treating even the costs that relate to construction activities completed and estimated profit element thereon as work-in-progress, which is not correct. The Committee is further of the view that the amount corresponding to the contract revenue less progress billings should be presented as receivable from the client, generally termed as ‘unbilled revenue’ on the assets side of the balance sheet in accordance with paragraph 42 of AS 7 reproduced above. The Committee is of the view that it is the advance payment received from the customers that does not relate to the contract activity performed which is recognised as a liability. Accordingly, the Committee is of the view that the recognition of liability as ‘Amount Billed to Clients A/c’ in respect of work completed and setting it off against value of ‘work-in-progress’ which is also cumulative value of work done on the closure/foreclosure/termination of the contract is not correct. In view of disclosure requirements prescribed in paragraph 39 of AS 7 reproduced above, with regard to contracts in progress, the company should disclose in the notes to accounts, the aggregate amount of costs incurred and recognised profits (less recognised losses) upto the reporting date.

11. With regard to the earlier opinion as referred to by the querist, the Committee is of the view that the earlier opinion with regard to valuation of work-in-progress was given considering the requirements of paragraph 15.1 of pre-revised AS 7, which required to disclose the progress payments either as a liability or as a deduction from the amount of contract work-in-progress. Since pre-revised AS 7 is not applicable in the extant case due to issuance of revised AS 7, which contains specific requirements with regard to the costs that can be classified as contract work-in-progress as discussed above, the earlier opinion of the EAC is not applicable.

D. Opinion

12. On the basis of the above, the Committee is of the opinion that the accounting treatment, followed by the company with regard to presentation of work-in-progress as envisaged in the company’s accounting policy No. 5 as stated above, is not correct. Work-in-progress should be recognised and presented only in respect of costs incurred by an enterprise that relate to future activity on the contract, provided these are capable of recovery, as discussed in paragraph 10 above.

With regard to earlier opinion as referred to by the querist, the Committee is of the view due to issuance of revised AS 7, the earlier opinion of the EAC, which was based on pre-revised AS 7 is not applicable, as discussed in paragraph 11 above.

______________________________

[1]Opinion finalised by the Committee on 24.7.2014.

|