Query No. 34 Subject: Accounting for payments made by the company for Prospective Multirole Fighter (PMF) Project.[1] 1. A company (hereinafter referred to as the ‘company’) is a navratna public sector undertaking (PSU) under the Department of Defence Production, Ministry of Defence (MoD). It is a Government company as per section 617of the Companies Act, 1956. State-of-the-art design and production infrastructure for Aircraft, Helicopters, Engines, Accessories and Support Systems have been established by the company. The company is currently handling the design and development of Light Combat Aircraft (LCA), Intermediate Jet Trainer (IJT), Prospective Multirole Fighter (PMF), Multi-role Transport Aircraft (MTA), Hindustan Turbo Trainer (HTT-40), Light Combat Helicopter (LCH), Light Utility Helicopter (LUH), etc. 2. The querist has stated that design and development activities of aircraft / helicopters are in general carried out in the following stages considering the customer requirements / specifications:

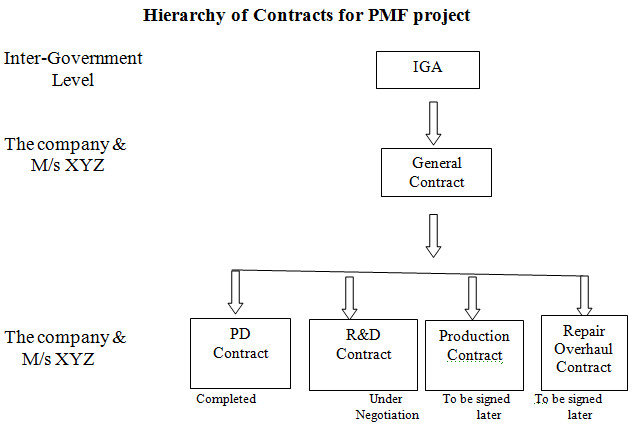

3. Prospective Multirole Fighter (PMF) project is a collaborative design and development (D&D) effort being undertaken by the company and Russian partner pursuant to an Inter-Government Agreement (IGA) signed on 18th October, 2007 between the Governments of the Republic of India and the Russian Federation. As per the IGA, the company is designated as the implementation agency from the Indian side and M/s XYZ has been designated as the implementation agency from the Russian side. The IGA for the PMF project lays down the broad agreements between the Indian and Russian Governments on all matters connected with the project and defines the representatives of the two Governments who will administer the IGA. It also defines the organizations in both the countries who are tasked with the actual implementation of the project underlying the IGA. All further contracts under the aegis of the IGA are signed between the two implementation organizations. For PMF project, the Government of India nominated the company as the implementation organisation from the Indian side owing to the company’s past experience and its prominent position in the field of aeronautics in India. The company and M/s XYZ have further signed a General Contract that governs the broad principles of cooperation, general terms and conditions and execution stages. The D&D of the PMF is implemented in the following two main stages:

For better understanding of the facts, the querist has provided the hierarchy of contracts for PMF project as follows:

4. During the PD stage, as per the milestones defined in the PD Contract, the company received various deliverables (goods and services) from M/s XYZ in the financial year (F.Y.) 2011-12 and F.Y. 2012-13. For F.Y. 2012-13, the aggregate value of such deliverables amounted to Rs. 1136.74 crores for which payment was made to M/s XYZ as per the provisions of the PD Contract. The company, as per its accounting policy 9.2, accounted the payment to M/s XYZ as D&D expenditure and D&D sales during F.Y. 2012-13. 5. Audit, vide their enquiry, commented upon the company’s accounting for payments to M/s XYZ as D&D expenditure/ sales in F.Y. 2012-13 that:

6. After the factual position was explained by the company in its written response, a provisional comment was issued by the audit stating that payments made by the company to M/s XYZ cannot be considered as part of the company’s development expenditure and sales. However, the references to AS 9 and AS 26 in the earlier enquiry were not present in the provisional comments. 7. After submission by the company of explanations to the provisional comments, the comments were ultimately dropped. However, in view of the issues raised by audit, the company gave an assurance that the matter will be referred to the Expert Advisory Committee of the Institute of Chartered Accountants of India (ICAI) for an opinion and that necessary accounting action, if any, following the opinion will be undertaken during F.Y. 2013-14. 8. PMF Project involves design and development in collaboration with Russian partner of an advanced fighter aircraft that will have state-of-the-art technological features. D&D of PMF will lead to certification of this aircraft for use primarily by the Russian and Indian Air Forces. 9. Based on the IGA signed between the two Governments on co-operation in development and production of the aircraft, a General Contract was signed on 22.12.2008 between M/s XYZ and the company. The General Contract outlines the broad principles of co-operation, general terms and conditions and execution stages of the project. As per bilateral understanding, funding for the project will be equally shared between the Indian and the Russian Governments.

10. The design of PMF is based on the basic structural and system design of a similar Russian aircraft, the development of which is under a separate Russian Government project. To this baseline design, which is adopted for PMF, suitable modifications to meet the specifications as per the joint technical requirements have to be incorporated by the company and M/s XYZ as per mutually agreed work share to create the aircraft. Although the scope of activities in the PMF project includes many activities towards development of new technologies that can be classified as research. However, as per the querist, the share of such activities as a proportion of the overall cost of the PD stage is not very significant. Hence, it is safe to state that the scope of work in the PMF project will more appropriately meet the definition of development as per AS 9. Moreover, there are no significant uncertainties regarding the technical feasibility of the product. In view of all these aspects, the scope of work of PMF cannot be classified meaningfully as ‘research’ as per AS 26. 11. The PD Contract between the company and M/s XYZ was signed on 21.12.2010 after the MoD completed the contract and price negotiations and obtained clearance from the Cabinet Committee on Security (CCS). The Government of India formally accorded sanction to the company for the PD phase of PMF project in January, 2011 and an amendment dated March, 2011. The Indian portion of expenditure on PMF Project is met from the capital budget of the Indian Air Force.

12. The total sanction for the PD phase was 315.2 million USD with the following breakup.

13. The deliverables to the company from the Russian side as per PD contract are broadly summarised below:

14. Indian and Russian sides commenced their works relating to Preliminary Design (PD) of the PMF in February, 2011 (T0 as per the PD Contract). The company along with other Indian co-executers progressed with the Indian work share. Russian side progressed with their work share responsibilities as per the PD contract and completed various milestones. With completion of both Indian and Russian deliverables and activities, the PD Contract has been closed by June, 2013. Accounting treatment of D&D sales in general by the company: 15. During D&D, a product required by the customer is designed and developed by the company and certified for service usage. Based on successful D&D, the customer will order production and delivery of the product on a large scale. This latter stage is usually termed as Series Production. 16. The cost of the D&D is fully funded by the customer (IAF, Navy, Army, etc.). During D&D, expenditures are incurred by the company on the following major items:

17. The unique feature of the D&D stage is that although various goods and services as above are generated in the process of D&D, these are not deliverable to the customer. Rather, these goods and services can be construed as consumed by the D&D process itself. Production and consumption of these goods and services are evidenced to the customer by completion of various milestones and activities of the D&D project. 18. During D&D, customer normally releases funds to the company based on a set of project milestones which are reflected in the sanction letters or contracts as applicable. D&D expenses accrue progressively as each stage of D&D is being completed. The recognition of revenues for D&D projects is normally based on such defined milestones and activities.

19. D&D projects are normally taken up by the R&D centres of the company which are dedicated to design and development of products and services and the related development of technologies. The R&D centres of the company are approved by the Department of Scientific and Industrial Research (DSIR) and the approvals are periodically renewed. For these R&D centres, all expenditures related to D&D projects can be assumed to be incurred in the ordinary course of business. 20. The expenditure incurred on design and development projects can be broadly classified under three categories.

21. As per accounting policy 9.2 of the company, development sales are set up on incurrence of expenditure identifiable to work orders and milestones achieved as per contract. Where milestones have not been defined, sales will be as per actual incurrence of expenditure. 22. Expenditure and sales in respect of all customer-funded D&D projects of the company are being accounted for as per the above accounting policy in a consistent manner over the years. Accounting treatment of D&D cost of PMF and analysis of the Audit Comments: 23. The D&D of the aircraft under PMF project is undertaken by the Aircraft Research & Design Centre (ARDC) of the company as the prime agency supported by other R&D centres of the company, divisions of the company and external agencies such as the Defence Research & Development Organisation (DRDO)/ Council of Scientific & Industrial Research (CSIR) laboratories. 24. The deliverables from M/s XYZ to the company during the PD stage as per the PD Contract and the development expenditure/ sales accounted for by the company in the relevant financial years based on these deliverables are summarised below in the Table:

25. In addition to the above, expenditures incurred by the company on its own and expenditures of its Indian partners have also been accounted for as per accounting policy 9.2 in both the above financial years. There have been no audit observations in respect of the sales of Rs. 125.93 crore booked in F.Y. 2011-12 as per the Table above. However, audit made observations on the sales of Rs. 1,136.74 crore booked in F.Y. 2012-13, which is the subject of the present referral. “Development Sales in Note 22 of the Accounts includes Rs. 1,13,674.01 lakh being expenses incurred on Indian Prospective Multi-Role Fighter (PMF) towards training to Indian Specialists, training materials, supply of Design documents and special Software / Database etc. for which payment was made to Russian side as project expenditure and accounted in the books as Direct Expenses under Note - 30. These Project Expenses have been accounted as Development Sales as per Accounting Policy 9.2.” (Emphasis supplied by the querist.) On this Note, audit had remarked in the Provisional Comments that:

The audit observations and the point-wise responses have been provided by the querist for the perusal of the Committee.

27. The querist has stated that in order to gain a comprehensive understanding of the linkage between the work share and joint funding of the PMF project and thereby understand the basic issues which are at the root of the objections raised by the Government audit, it is necessary to analyse certain specific provisions of the IGA, General Contract and the PD contract and to derive logical conclusions therefrom. Accordingly, relevant extracts of various contracts and accounting policy of the company have also been provided by the querist for the perusal of the Committee. 28. Work share of PMF project for the total R&D stage can be divided into two categories based on the mode of execution.

(Emphasis supplied by the querist.)

29. The payments to M/s XYZ under the PD Contract amounting to a total of 243.2 Million USD are under category b(ii) above. The Indian share of 52 Million USD is under b(i) above. Both these expenditures are thus pursuant to Indian work share execution and derived from the overall 50% Indian funding for PMF project. These are thus, as per the querist, legitimate development expenditures of the company as the sole implementation agency from Indian side and as recipient of all Indian Government funding to PMF project. 30. Also, it can be observed that category (a) in paragraph 28 above represents 50% funding for the project by the Russian Government in which the company or the Government of India has no payment obligations. Therefore, according to the querist, the question of compensation for IPR or such other transfer payments to Russia does not arise in the case of PMF project. Further, with regard to creation of IPR for the company, the querist has separately clarified that in the case of PMF project, IGA is the uppermost contract from which all the other contracts derive their validity and strength. So, it is evident that no contract below the level of IGA can override the provisions in the IGA. As far as IPR is concerned, the IGA contains the following wordings:

In view of the above, it would be clear that the rights in respect of IP will get transferred to the Government of India as a party to the IGA. Additionally, the rights are shared between the Indian and the Russian Governments as ‘Parties’. Coming to the specific issue of control, the company is not an agent, representative or delegate of the Government of India, but is only the organization nominated by the Government of India to implement the PMF programme from the Indian side. Therefore, it would be obvious that the company is in no position to exercise any control over the manner in which the rights under the PMF program are utilised by the Government of India in the future. Even though the General Contract and the PD contract have clauses regarding IP and mention the company as the Indian party, from the overriding nature of the IGA, it would be evident that the company will hold any such rights as a nominee of the Government of India. Also, at any stage during the project, Government of India would be free to alienate the rights of the company in this project and nominate any other entity in India to continue the implementation of the programme. In summary, the element of control which is an essential requirement of AS 26 is not met in the case of PMF project. Further, since the rights under the PMF programme, including the rights to produce the PMF aircraft after successful development, vest in the Government of India and Russia, there is no reasonable basis to expect that the future benefits from the project will definitely flow to the company. Form the foregoing, it would be apparent that the essential criteria as per AS 26 to recognise an intangible asset are not met in the case of PMF project. Consequently, as per paragraph 8 of AS 26, “if an item covered by this Standard does not meet the definition of an intangible asset, expenditure to acquire it or generate it internally is recognised as an expense when it is incurred”. 32. The querist has further clarified that the company should not be considered as an agent of the Government. The querist is of the view that if this line of reasoning was taken, as per AS 9, the receipts on account of the PMF project should not be recognised as revenue and instead, only the commission payable to the company should be treated as revenue. In the case of PMF, as there is no such commission payable to the company, the revenue should be nil. In a general sense, for a company to be treated as an instrumentality or an agent of the ‘State’, it needs to be discharging functions or conducting business as a proxy of the ‘State’ and these functions should be sovereign in nature. In reality, this is not at all the case. According to the querist, if all PSUs in India were thus interpreted as agents of the India State, then none of them can recognise revenues as per AS 7 or AS 9. The querist has further stated that the Government of India, vide DPE O.M. No. 16(10)/90-GM dated 9th November, 1990 has instructed that when PSUs enter into commercial contracts, the following clause should mandatorily be incorporated.

33. The querist has also clarified separately that the origin of the PMF project is the IAF’s strategic requirement for a fifth generation fighter aircraft to meet its long term objectives of defence of the Indian nation. The acquisition mode chosen by the Government was the IGA route and the company was nominated (by the Government of India through the IGA) as the organization in India who will develop and produce the PMF aircraft in collaboration with Russian partners. Any product to be designed and developed should have a technical specification through which the customer defines the comprehensive set of requirements as applicable to the product. In the present case, the Technical Specification of the PMF aircraft are embodied in a joint Indo-Russian document called the Tactical Technical Assignment (TTA) which is signed by:

The General Contract and the Preliminary Design Contract for PMF both mention that PMF will be designed and developed as per the TTA. Therefore, although there is no contract signed between the company and IAF in this case, the nature of IAF’s position as the customer for PMF and the position of the company as the provider of services to IAF are both unmistakably inferable from the bilateral contracts mentioned above, the TTA and the role of MoD as mentioned earlier. 34. Unlike the case where a readymade equipment is procured off-the-shelf by IAF, the PMF aircraft has to be designed, developed and certified before it can be inducted into IAF (and Russian Air Force) during the production phase. This task of design & development has been assigned to the company on the Indian side through the IGA. Apart from funding, supervision, reviews, making its bases available for flight testing, etc., IAF does not undertake on its own any tasks of design and development. Therefore, as far as the underlying design engineering services involved in creation of PMF for IAF is concerned, according to the querist, the company is the service provider to IAF who is the company’s customer for the PMF project. The funds provided to the company for PMF project under the PD contract as per the Government sanction are to be utilised by the company basically for the following types of expenditures:

Funds required for all the above types of expenditures are claimed by the company from IAF through invoices raised by the company. The Government sanction specifies the stages of completion at which such invoices can be raised. Similarly, all payments made by the company to Russian party and to other organisations are based on invoices raised by such parties on the company. 35. According to the querist, there are two options available for revenue recognition in the extant case:

Even a perfunctory reading of AS 7 would suggest that the application of the Accounting Standard is appropriate to contracts pertaining to construction of physical assets, such as, roads, dams, bridges, buildings, refineries etc. The creation of physical assets appears to be the main purpose and the services associated with such creation appear to be of a subsidiary significance. Also, in such contracts, it is rarely required to undertake research or development as defined in AS 26. On the other hand, AS 9 is the Standard that specifically deals with revenue recognition more comprehensively and is therefore, considered appropriate in the case of PMF project. As aforementioned, the company is the executor of the PMF project and IAF is its customer. All the activities undertaken during the creation of the PMF aircraft will meet the definition of development as per AS 26. Therefore, the revenues arising against rendering of design engineering services by the company to IAF for development of PMF aircraft will have to be treated as revenues from rendering of services under AS 9. As a corollary, once development is completed, delivery of aircraft in large numbers to IAF will result in revenues from sale of goods. Also, as the company is engaged routinely in design, development, production, overhaul, etc. of aircraft, the development of PMF is “in the course of the ordinary activities of the enterprise (the company)”. 36. Further, paragraph 4.1 of AS 9 states that:

All the requirements for measurement of revenue are met in the case of PMF project. It was also established earlier that the concept of agency relationship is not applicable in this case. Paragraph 7.1 of AS 9, inter alia, states “Revenue from service transactions is usually recognised as the service is performed, either by the proportionate completion method or by the completed service contract method”. In the case of PMF project, the audit objection was related to recognition of expenditures and revenues on account of payments made by the company to the Russian party. Revenue was recognised based on proportionate completion method based on predefined milestones as per the PD contract. These milestones were also linked to various deliverables from the Russian side to the company. Therefore, when the milestones as per the PD Contract were completed and deliverables were received by the company, a well-defined and rational basis existed to recognise revenue by the proportionate completion method. Supply of goods and rendering of services by the Russian party is an essential ingredient for the company to fulfil its obligation as service provider to IAF who provided the funding and is the company’s customer. Therefore, from the company’s perspective, no special treatment needs to be adopted whether certain deliverables are procured from the Russian side or from any other supplier. All such expenditures which flow from valid commercial contracts signed by the company on its own capacity are inextricably connected with execution of the PMF project and are therefore, of the same character irrespective of the fact that the Russian party is also the company’s partner in the project. Paragraph 9.1 of AS 9 states “Recognition of revenue requires that revenue is measurable and that at the time of sale or the rendering of the service it would not be unreasonable to expect ultimate collection”. In the instant case, revenue was exactly measureable as explained above. Also, as per the Government sanction to the company, for all payments due to the Russian side, the company was authorised to collect the funds from IAF in advance and remit to the Russian side based on completion of milestones as per the PD Contract. The exchange rate variation due to movements in Rupee/Dollar rate from the date of drawal of advance and the date of remittance to Russia was also fully protected as per the sanction. Therefore, collection was never under any uncertainty. In summary, the company maintains that the accounting for revenues of PMF project in respect of payments made to the Russian side fully complies with the provisions of AS 9. B. Query 37. The querist has sought the opinion of the EAC as to whether the accounting treatment of the payments to the Russian side towards goods and services received by the company in accordance with the PD Contract for the PMF project as development expenditure and recognising as development sales during F.Y. 2012-13 as per accounting policy 9.2 of the company is in order. C. Points considered by the Committee 38. The Committee notes that the issue raised by the querist relates to appropriateness of accounting treatment of the payments made to the Russian side towards goods and services received by the company pursuant to the PD contract for developing the preliminary design of the PMF (Project Multi Fighter) project as ‘development expenditure’ and also correspondingly recognising such payments as ‘development sales’. The Committee has, therefore, examined only this issue and has not examined any other issue that may arise from the Facts of the Case, such as, nomenclature of revenue and expenditure as ‘development sales’ and ‘development expenditure’, determination and measurement of project costs and revenues, recognition of revenue and expenditure relating to subsequent phases of the PMF project, accounting in the books of account (prepared, if any) of IAF, whether the activities carried out under the PMF project can be considered as ‘research’ activities as per AS 26, etc. Further, while considering the facts and forming its views on the aforesaid accounting treatment, the Committee has relied only on the extracts of the agreements furnished by the querist. The Committee has also presumed from the Facts of the Case that there is a principal to principal relationship, viz., no agency relationship, between the company and the Government or the IAF. 39. The Committee understands from the Facts of the Case that PMF project in the extant case is a design and development (D&D) activity, where the company considers IAF as its customer. Further, Preliminary Design (PD) stage is one of the stage of such D&D activity and for undertaking the activities of PD stage, a PD contract has been entered into by the company with M/s XYZ for its share of work under the PMF Project. The Committee also notes that according to the agreements (refer paragraph 28(b)(ii) of the Facts), with respect to the share of work to be performed by the company, the company has the option of either carrying out the work by itself, or sub-contracting the work to be carried out, with the first choice of refusal to be given to M/s XYZ from the Russian side. The company has opted for sub-contracting a part of the work to M/s XYZ, for which a separate agreement (PD contract) has been entered into between the company and M/s XYZ. 40. The Committee notes that as per PD contract, the scope of work to be performed by M/s XYZ includes preliminary designs, documentation, special software/ database and training for employees, etc. Accordingly, the issue that arises from the above is whether the expenditure incurred towards these activities by the company results into creation of an asset or it results into an expense to be recognised in the statement of profit and loss. In this regard, the Committee notes the following paragraphs of AS 26, notified under the Companies (Accounting Standards) Rules, 2006 and the Framework for the Preparation and Presentation of Financial Statements, issued by the Institute of Chartered Accountants of India:

41. The Committee notes that in the extant case, there are specific clauses in the PD contract with respect to Intellectual Property Rights (IPRs). One of the clauses states that “the company shall not copy or reproduce the documentation delivered in compliance with the present Contract and shall not use Russian inventions, “know-how” and other scientific and technical results contained in it for purposes other than the fulfilment of the Indian work share under this Contract without the prior written consent of M/s XYZ after receipt of the appropriate written request of the company. This Clause will apply reciprocally to M/s XYZ also”. Further, the Committee notes from the Facts of the Case that the commercial exploitation by M/s XYZ or the company through sales to third countries is not permitted and is subject to Inter-Governmental decisions. Even the production and sales of this aircraft by the company in the future for Indian Air Force will be based on quantities and funding to be decided by the Indian Government. Moreover, due to overriding nature of the Inter-Government Agreement over any other contract, as stated by the querist in paragraph 30 above, any IPR generated out of the PD contract would belong to the Indian and Russian Governments and not to the company. Also, the company does not have the right to copy or reproduce any part of the documentation received for purposes other than the contract. Thus, although the PD contract may give rise to creation of IPR, know-how, etc., the company has no discretion with regard to their usage. In view of this, the Committee is of the view that since in the extant case, the company is holding any such rights only as a nominee of the Government for implementation of the PMF Project, no resource controlled by the company is arising out of the PD contract and therefore, the expenditure incurred on PD contract cannot be recognised as an asset and the same should be recognised as an expense in the statement of profit and loss as and when incurred. 42. The Committee further notes that since it is presumed in paragraph 38 above that there is a principal to principal relationship between the company and the Government or the IAF, for the company, IAF is its customer and the company is only an executor of the PMF project, who has been nominated by the Indian Government from Indian side for such project. Further, considering the activities involved in the PMF project (refer to paragraph 2 above), the Committee notes that the company is rendering design and development services to the IAF for development of PMF aircraft, which, as per the querist, meet the definition of development as per AS 26 ( refer to paragraph 35 above). Accordingly, the Committee is of the view that although the PMF project would also involve creation of prototype of PMF aircraft and after its successful development would be consumed by the company itself for further manufacturing (viz., series production) by the company for IAF, the PMF project is basically a contact for rendering design engineering services to the IAF and the creation of aircraft, which could be considered as a construction activity as per the principles of AS 7 is only an insignificant portion of such project. Accordingly, considering the economic substance of the contract from future series production by the company, the Committee is of the view that the principles of AS 9 would be applicable in the extant case. The Committee also notes the definition of revenue as per AS 9, Revenue Recognition, notified under the Companies (Accounting Standards) Rules, 2006, as below:

The Committee notes that the amount received by the company during the PD stage is towards preparation of preliminary designs, software, training materials and other documentation (refer to paragraph 24 above), which has been sub-contracted by the company under PD contract to the Russian agency. This indicates that the company is rendering the specified services to IAF, for which it is receiving consideration. Therefore, based on the definition of revenue as reproduced above, this amount should be recognised as revenue. Further, considering that the amount received is towards preliminary designs and training materials etc. which spans over a period of two years and the contract has specified milestones to be achieved at various points of time, the company should apply the principles of proportionate completion method for recognition of revenue over the contract period as envisaged in the following paragraphs of AS 9:

The Committee is of the view that the revenue should be recognised in accordance with the above paragraphs of AS 9 as per the proportionate completion method considering the degree of completion of services and achievement of various milestones as per the contract. Accordingly, the policy of the company to recognise ‘development sales’ would be correct provided it is in accordance with the principles of AS 9, as discussed above. D. Opinion 43. On the basis of the above, the Committee is of the opinion that the accounting treatment of the payments to the Russian side towards goods and services received by the company in accordance with the PD Contract for the PMF project as development expenditure and recognising as development sales during F.Y. 2012-13 as per accounting policy 9.2 of the company would be in order provided these are recognised as per the requirements of AS 9, as discussed in paragraph 42 above. __________________________________ [1]Opinion finalised by the Committee on 11.12.2014.

|