Query No. 13

Subject: Accounting treatment of dead stock. 1

A. Facts of the Case

1. A company is a joint venture of N Ltd. and G Ltd., engaged in the business of electricity generation and LNG (Liquefied Natural Gas) regasification having facility at Anjanwel, Maharashtra.

2. The company has commissioned its LNG regasification unit (LNG Terminal) on 22nd May, 2013. The querist has stated that for commissioning of the LNG Terminal, the company has procured one time LNG which is required to be maintained at minimum level in the system comprising of ring main and storage tanks to keep the LNG Terminal operational. LNG is stored in the LNG storage tanks at (-) 162oC. The minimum level of LNG is required to be maintained for operation of the pump and to keep the tank in cold condition to avoid expansion/contraction for life time. The boil off gases from the top layer of LNG is removed to avoid pressure increase of the tanks and maintaining the cold condition.

3. The querist has further stated that the company has entered into long term agreement with G Limited to provide services of regasification of LNG brought by them through its LNG Terminal against the predefined charges (per MMBTU) as per the agreement. Separate inventory records of the company and G Ltd. are maintained and reconciled quarterly, although physical separation of inventory of the company and G Ltd. is not possible. The querist has also stated that the company has no obligation for procurement of LNG cargos and related expenditure. G Ltd. has allowed system use gas of 0.66% of received energy and any gas consumption for system use other than fuel gas is charged to consumption. The company has to maintain the minimum LNG level including by replenishment although may be rarely required during the lifetime of the plant operations. The company has contractual arrangement with G Ltd. to bring cargos so as to maintain cold conditions of the plant.

4. According to the querist, it is pertinent to mention that LNG in the ring main and storage tank, procured at the time of commissioning by the company, is essential minimum quantity of LNG which is pre-requisite for keeping the LNG Terminal ready for operation at any time and it cannot be taken out from the system except in the case of decommissioning of the plant when it has to be released in the atmosphere. In view of the above, the company has capitalised the cost of LNG required to keep the system operational along with the LNG Terminal.

Basis of treatment given by the company

5. The querist has also stated that the company has capitalised the LNG based on paragraph 6.1 of Accounting Standard (AS) 10, 'Accounting for Fixed Assets'2 which provides that "Fixed asset is an asset held with the intention of being used for the purpose of producing or providing goods or services and is not held for sale in the normal course of business.” Further, while capitalising the cost of LNG, the company has considered the following:

6. With regard to the process being followed at LNG regasification unit (LNG Terminal) and the company’s relationship with G Ltd., the querist has separately clarified as follows:

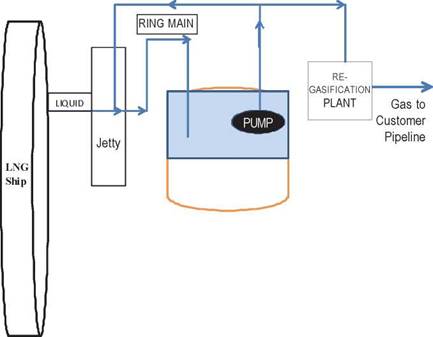

The querist has also supplied a flow chart to explain the process at Annexure 1.

B. Query

7. On the basis of the above, the querist has sought the opinion of the Expert Advisory Committee as to whether the company has given correct treatment by capitalising the cost of LNG required essentially for keeping the system operational and available for uninterrupted regasification services to G Ltd. under the agreement.

C. Points considered by the Committee

8. The Committee notes that the basic issue raised in the query relates to the accounting treatment of the cost of the minimum level/quantity of LNG required to be maintained in the system, viz., LNG Terminal comprising ring main (pipelines) and storage tanks. The Committee has, therefore, considered only this issue and has not examined any other issue that may arise from the Facts of the Case, such as, accounting for regasification services provided by the company to G Ltd., valuation of inventory of gas in the system, determination of cost of gas, etc.

9. With regard to the issue raised, the Committee notes the definition of the term ‘inventories' as given in Accounting Standard (AS) 2, ‘Valuation of Inventories', and the definition of the term ‘fixed asset' as given in Accounting Standard (AS) 10, ‘Accounting for Fixed Assets', notified under the Companies (Accounting Standards) Rules, 2006, which are reproduced below:

10. From the above, the Committee notes that the classification of an asset as a fixed asset or inventory depends on its intended primary use for an entity. If an asset is essentially held for using it for the purpose of producing or providing goods or services rather than for sale in the normal course of business, it is classified as fixed asset. However, if it is held for sale in the ordinary course of business, or if it is used in the process of production for such sale; or in the form of materials or supplies to be consumed in the production process or in the rendering of services, the asset should be classified as inventory. The Committee notes from the Facts of the Case that complete ring main system and LNG tanks are required to be maintained in cold chain at (-) 160oC. The maintenance of cold chain is essential in ring main pipelines throughout the plant life, otherwise with the heat ingress leading to temperature differentials, the pipelines would bend due to thermal expansion and crack leading to release of hazardous hydrocarbons in cryogenic conditions. Similarly, the LNG tanks also need to be maintained at (-) 160oC for avoiding major damages to tanks because of thermal expansions-contractions effects. Further, in case of breakage of cold chain, the plant would require decommissioning and this cold chain is to be maintained even if ships are not coming to LNG terminal. For this purpose, during project design of LNG terminal, the distance between jetty and tanks is minimised so that cold chain can be maintained easily.

11. From the above, the Committee notes that minimum quantity of LNG in the ring main and storage tanks is essential to maintain the temperature so as to avoid expansion/contraction of the ring main and storage tanks and to keep the LNG Terminal operational. Thus, minimum level of LNG in the ring main and storage tank is pre-requisite for keeping the LNG Terminal (plant) ready for operation at any time. Accordingly, the Committee is of the view that in the extant case, technological design of pipelines and tanks is such that, minimum level of gas is always required to be maintained in the system to keep the system operational and that such pipelines and tanks are not merely a mode of transportation and storage. The Committee also notes that the company is only providing services for regasification of LNG bought by G Ltd. under the agreement and not in the business of sale or purchase of LNG in normal course. Thus, it is not held for sale in the normal course of business. Further, it is noted from the Facts of the Case that this quantity of LNG can never be used in the life cycle of the plant as this cannot be pumped out and required to be always present in the system to keep the Terminal operational. Even in the case of decommissioning this quantity cannot be used or sold except to be flared up in the atmosphere. Thus, it cannot also be considered to be held for sale or consumption in the process of production or in the rendering of services. Accordingly, the Committee is of the view that the minimum level of gas cannot be considered and recognised as ‘inventory'. The Committee is of the view that the cost of initial gas procured for commissioning of the LNG Terminal should be recognised as a fixed asset.

D. Opinion

12. On the basis of the above, the Committee is of the opinion that the treatment given by the company of capitalising the cost of LNG required for keeping the system operational is appropriate

Annexure I

Flow Chart of LNG Terminal ___________ 1 Opinion finalised by the Committee on 11.1.2016. 2 T he opinion should be read in the context of Accounting Standard (AS) 10, ‘Accounting for Fixed Assets', which has been revised as AS 10, ‘Property, Plant and Equipment’ by the Companies (Accounting Standards) Amendment Rules, 2016 vide Ministry of Corporate Affairs (MCA) Notification No. G.S.R. 364(E) dated 30.03.2016. |